A Look at Incyte's Valuation After Pivotal Phase 3 Data for Povorcitinib in Hidradenitis Suppurativa

If you have been watching Incyte (INCY) lately, the company’s just-released interim data from its Phase 3 STOP-HS study may be grabbing your attention. The update, focused on povorcitinib in moderate-to-severe hidradenitis suppurativa, delivered statistically significant and clinically meaningful results along with a safety profile consistent with earlier data. With regulatory filings planned in Europe and the US, this milestone brings povorcitinib closer to a possible market launch and has prompted new conversations among investors about Incyte’s pipeline potential and near-term prospects.

This announcement adds to a period of momentum for Incyte, both in the clinic and the market. Over the past three months, the company’s shares have climbed nearly 24%, outpacing the broader S&P 500. This uptick is accompanied by other recent catalysts such as FDA approval for Opzelura in pediatric atopic dermatitis and notable executive changes, all indicating that the company is undergoing transformation and expansion. The combination of pipeline progress and market response has pushed Incyte toward the higher end of its recent trading range, warranting a closer look at what is currently driving valuation.

With clinical wins and strong share performance this year, is Incyte offering investors a genuine buying opportunity, or has the market already priced in this period of growth?

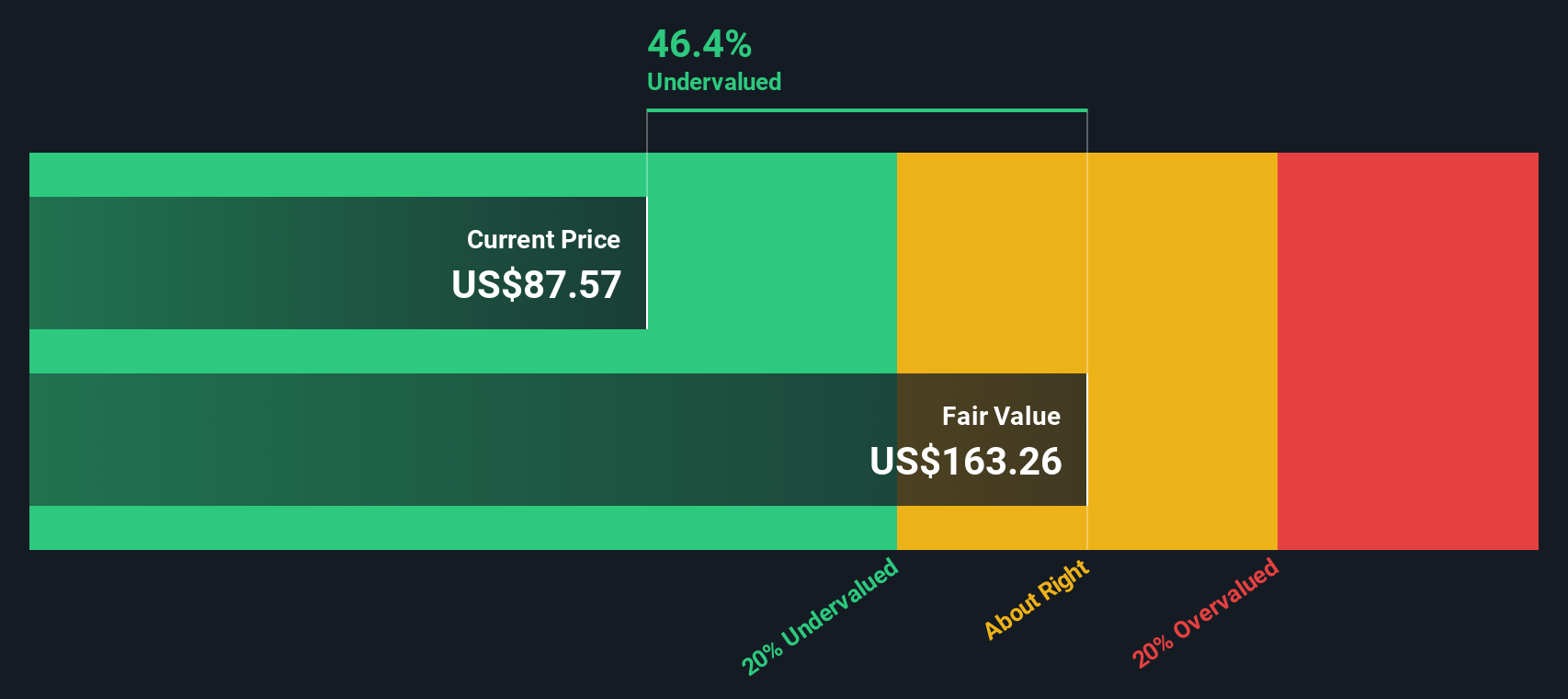

Most Popular Narrative: 1.1% Undervalued

The prevailing narrative suggests that Incyte is trading just below its fair value, with only a slight undervaluation relative to analyst expectations.

Recent advances in precision medicine, exemplified by the successful early clinical data for mutant-CALR antibody 989 and Incyte's collaboration with QIAGEN for mutation-specific diagnostics, directly align with accelerating industry adoption of targeted therapies, expanding total addressable markets and improving the probability of commercial success. These factors could enhance future revenue and margin expansion.

What is fueling this tight valuation gap? Analysts are betting on aggressive growth assumptions and sharper margins. Find out which vital future milestones and bold projections are setting this narrative apart. The underlying math here is not what you might expect. Curious to see what makes this price target tick?

Result: Fair Value of $83.62 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, continued heavy reliance on Jakafi, along with the threat of pipeline setbacks or regulatory pressures, could sharply alter Incyte's growth outlook.

Find out about the key risks to this Incyte narrative.Another View: DCF Model Offers a Different Perspective

While the analyst view suggests Incyte is close to fair value, our DCF model presents a more optimistic picture and indicates the shares may actually be undervalued. Could this alternative approach reveal upside that the market is missing?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Incyte Narrative

If you have a different angle or want to dig deeper into the data, you can easily craft your own narrative in just a few minutes. Do it your way.

A great starting point for your Incyte research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Winning Investment Ideas?

Don’t let market momentum pass you by. Uncover fresh opportunities and actionable themes with these powerful Simply Wall St tools and give your portfolio the edge leaders use.

- Pinpoint stocks with real potential for significant gains by tapping into undervalued stocks based on cash flows for companies trading below their true worth.

- Capture growth in the fast-evolving world of artificial intelligence and see which businesses are making waves through AI penny stocks.

- Seize stable income streams from companies consistently outperforming on yield with dividend stocks with yields > 3% above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com