How Do Recent Contract Wins Impact HII’s Current Valuation in 2025?

If you have Huntington Ingalls Industries on your investing radar, you are not alone in wondering whether now is the moment to make a move. The stock recently closed at $278.77 and has notched some attention-grabbing returns: up 1.3% in the past week, 0.9% over the last month, and an impressive 48.6% year-to-date. Looking even further back, Huntington Ingalls has delivered a strong 117.0% gain over the last five years. These results are notable, especially when market sentiment around defense contractors is shifting, with investors weighing both increased geopolitical demand and changing risk appetites.

Of course, strong past performance is only part of the equation, and sustained gains require you to keep an eye on valuation. On that front, Huntington Ingalls scores a 4 out of 6 in our valuation assessment. This means the company is undervalued based on four different checks, pointing to some potential for upside. We'll break down what those valuation checks are, and more importantly, dig into how each one might influence whether HII really stands out from the crowd. Stick around, because after we review the classic valuation metrics, I will share a more nuanced approach that many investors overlook, one that could really change how you think about the stock’s value proposition.

Why Huntington Ingalls Industries is lagging behind its peersApproach 1: Huntington Ingalls Industries Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model projects a company’s expected future cash flows and then discounts those values back to today to estimate what the business is intrinsically worth. For Huntington Ingalls Industries, the model uses a two-stage Free Cash Flow to Equity approach to estimate value based on future performance.

At present, Huntington Ingalls generates $692.8 million in free cash flow. Analyst forecasts suggest modest growth in the coming years, with free cash flow expected to reach around $658 million by 2029. For subsequent years, these figures are extrapolated with long-term projections reaching $735.7 million in 2035. These projections, all calculated in US dollars, are grounded in a mix of analyst consensus for the next five years, followed by reasonable, incremental adjustments for years further out.

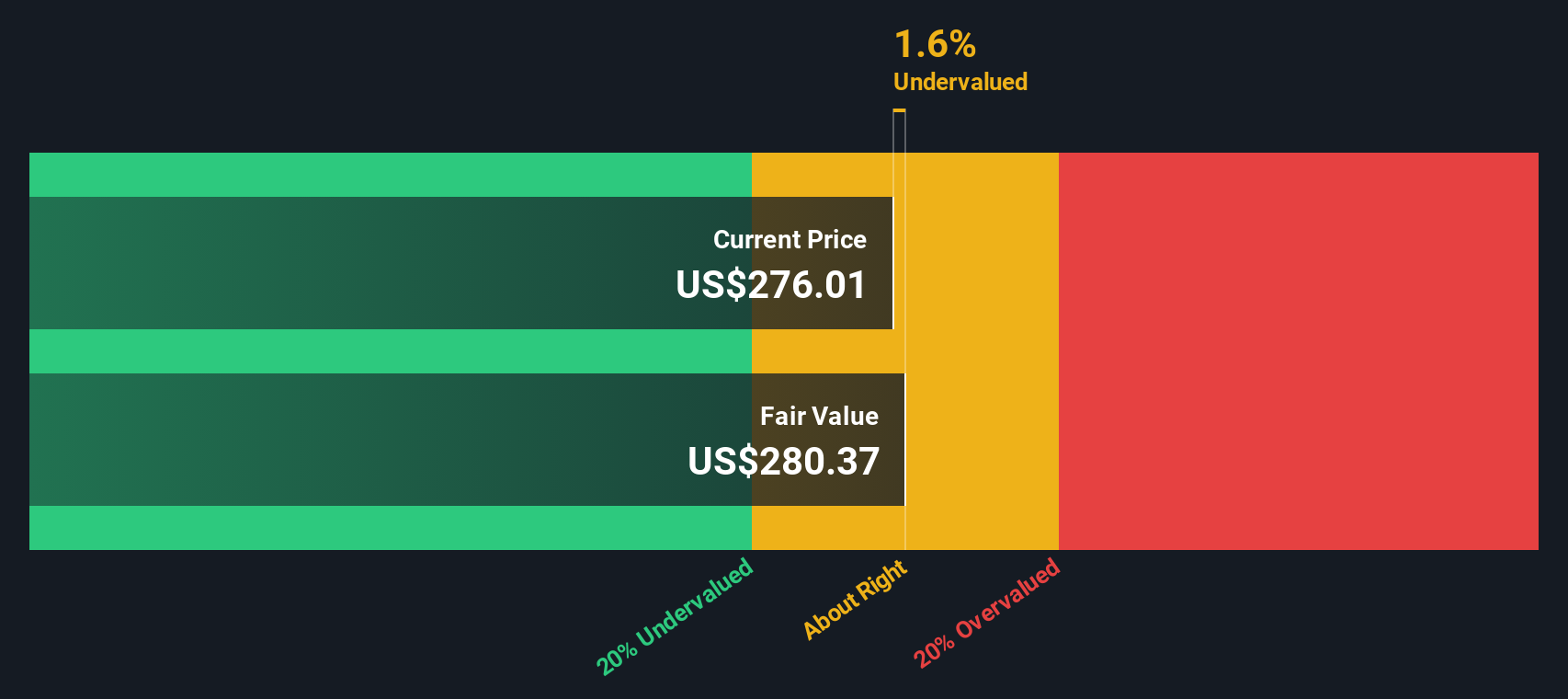

After discounting these future cash flows back to the present, the model estimates an intrinsic value per share of $281.08. With shares currently trading at $278.77, this translates to the stock being roughly 0.8% undervalued compared to its intrinsic value. This is a very slight difference, suggesting HII is almost exactly in line with what the market believes it’s worth right now.

Result: ABOUT RIGHT

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Huntington Ingalls Industries.

Approach 2: Huntington Ingalls Industries Price vs Earnings

The Price-to-Earnings (PE) ratio is a classic and effective way to value profitable companies like Huntington Ingalls Industries because it directly relates a company’s share price to its earnings. For investors, this metric gives a clear sense of how much they are paying for each dollar of current profits, which is key information when the company is consistently profitable.

It is important to remember that what qualifies as a “normal” or “fair” PE ratio depends not just on industry standards, but also on the business’s growth prospects and risk profile. Typically, faster-growing or less risky companies deserve higher PE ratios, while slower-growing or riskier ones trade at lower multiples.

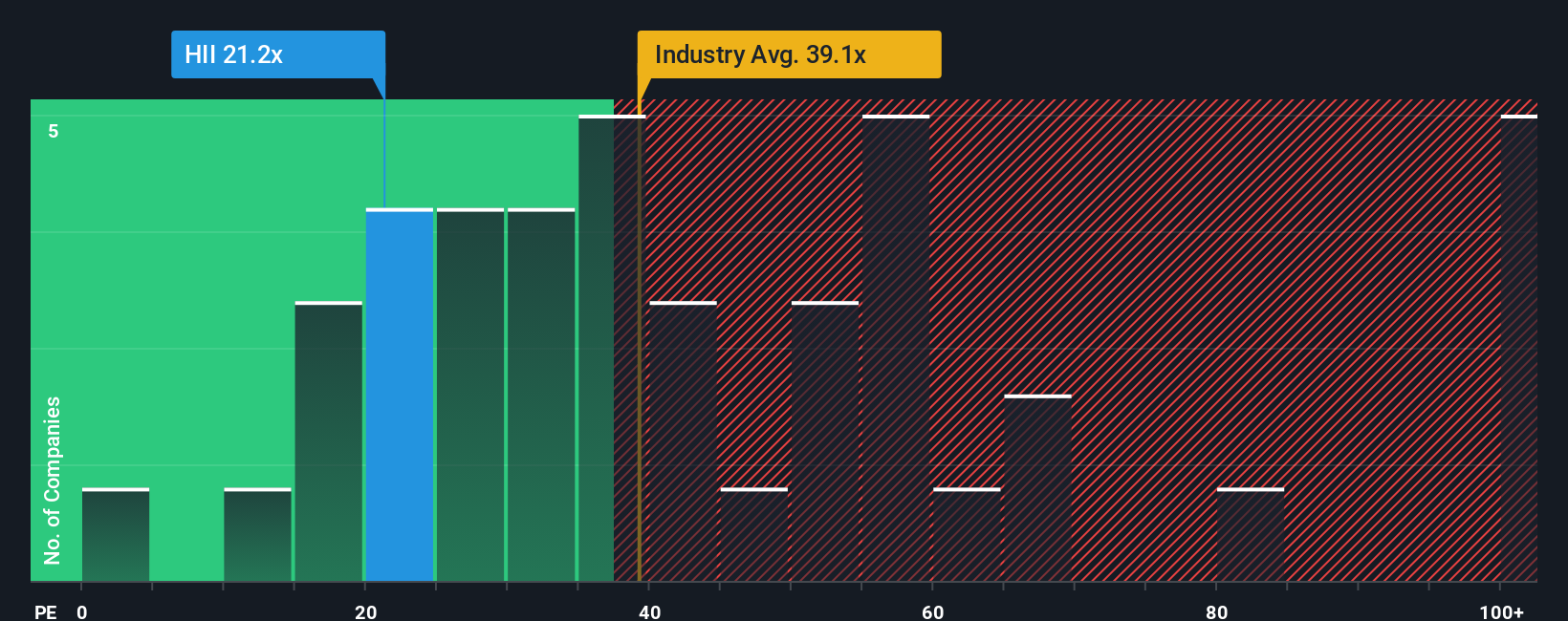

Currently, Huntington Ingalls trades at a PE ratio of 20.8x. For context, the broader Aerospace & Defense industry has an average PE of 38.1x, while HII’s peer group averages an even higher 39.9x. On the surface, this makes Huntington Ingalls look attractively valued compared to other companies in the sector.

However, Simply Wall St’s proprietary “Fair Ratio” offers a more nuanced assessment by factoring in the company’s unique mixture of earnings growth, profit margins, risk, market cap, and industry context to determine what would be a reasonable multiple for HII. While broad benchmarks are useful, the Fair Ratio provides an improved comparison by focusing on aspects specific to Huntington Ingalls itself.

According to this model, HII’s fair PE ratio is estimated at 28.9x. With the current PE at 20.8x, the stock appears undervalued when adjusting for its specific fundamentals rather than just relying on external comparisons or broad industry norms.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your Huntington Ingalls Industries Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is the story behind the numbers. It captures your unique perspective on a company and ties it to specific, transparent assumptions about future revenue, earnings, and profit margins, resulting in a tailored Fair Value estimate.

Rather than relying purely on static metrics, Narratives let you connect what you know about Huntington Ingalls Industries, such as major defense contracts, new technologies, or operational challenges, directly to a personalized financial forecast and valuation. On Simply Wall St’s platform, you can easily create or explore Narratives from millions of investors right from the Community page, making this tool accessible whether you're a beginner or an experienced investor.

Narratives also help you make smarter buy or sell decisions. You can instantly see how your Fair Value compares against the current market price and update your view as soon as new information, such as news or earnings updates, becomes available. For example, one investor might build a Narrative forecasting robust earnings growth and assign a Fair Value of $324.0, while a more cautious investor could focus on contract risks and arrive at a Fair Value of $221.0. Narratives make it easy to see and act on these different perspectives, helping you invest with more confidence and clarity.

Do you think there's more to the story for Huntington Ingalls Industries? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com