Is UBE (TSE:4208) Undervalued? Examining the Latest Valuation After Recent Share Price Movement

When a stock like UBE (TSE:4208) makes a move without an obvious catalyst, it naturally grabs attention from investors wondering what might be brewing under the surface. Sometimes these price changes are less about a single headline and more about shifting sentiment, especially when there is no clear event driving the change. In cases like this, the real question becomes whether the market is hinting at something bigger ahead or simply adjusting to broader trends.

Stepping back, UBE’s stock has not delivered a strong year. For the past twelve months, its return lags behind the wider market, with a drop of about 11%. Over the past month, however, there has been moderate upward movement, and the past three years tell a different story with gains of 37%. This combination suggests that while longer-term momentum is evident, recent performance has been softer and may indicate changing risk perceptions or shifting market focus after previous growth.

With that in mind, the question on investors’ minds is clear: does the current price reflect UBE’s true value, or is the market overlooking potential for a rebound?

Price-to-Sales of 0.5x: Is it justified?

Based on its price-to-sales (P/S) ratio, UBE appears undervalued compared to both its industry and peer group averages. The company’s current P/S ratio is just 0.5x, which is lower than the JP Chemicals industry average of 0.6x and the peer average of 0.9x.

The price-to-sales ratio measures how much investors are willing to pay for each unit of sales. It is especially relevant for companies like UBE in the chemicals sector, where earnings can be volatile and sales figures may offer steadier insight into the business's value.

This low multiple suggests the market is not fully crediting UBE’s sales base, possibly due to concerns about unprofitability or recent challenges. However, for investors looking for value, the current P/S could make UBE attractive if the company manages to return to profitability as forecast.

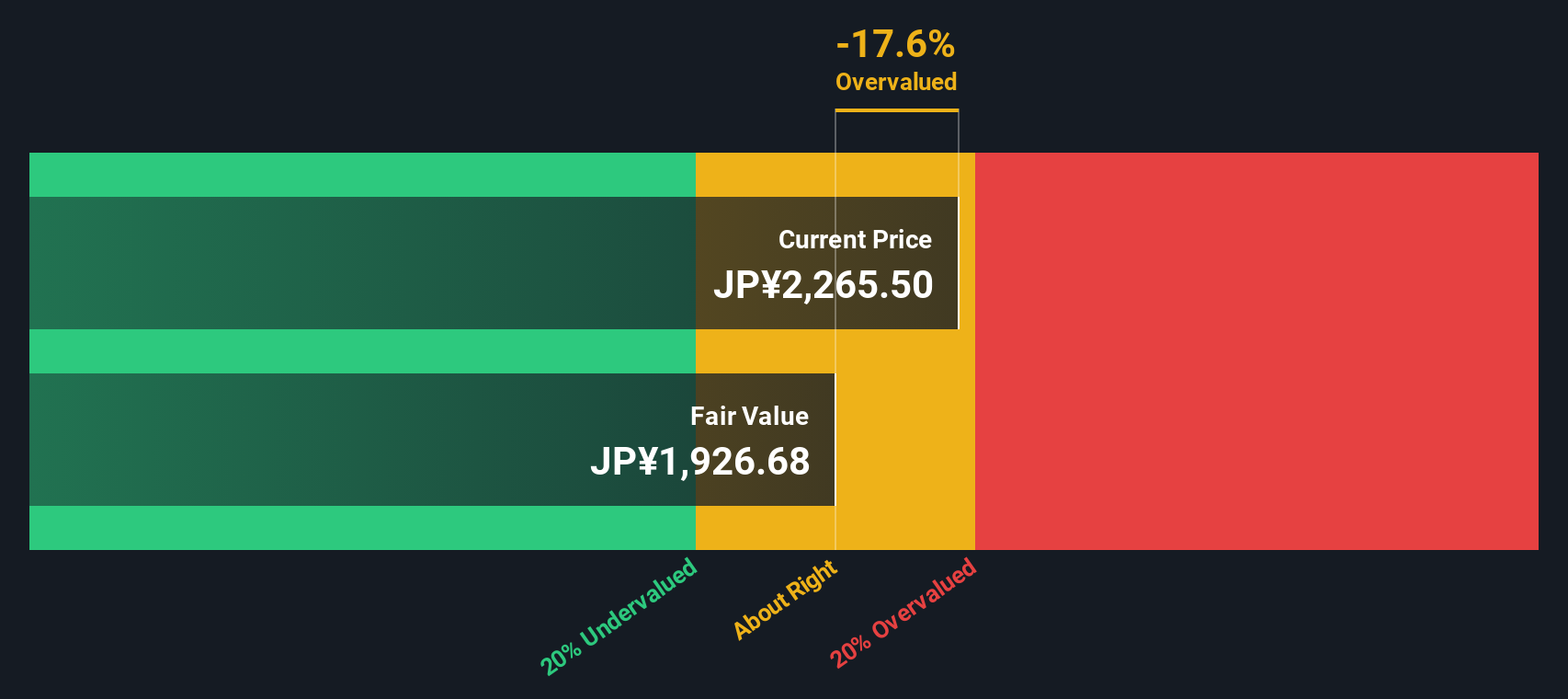

Result: Fair Value of ¥2,001.12 (OVERVALUED)

See our latest analysis for UBE.However, declining annual revenue and recent unprofitability pose risks that could weigh on UBE’s valuation, even with potential for a recovery.

Find out about the key risks to this UBE narrative.Another View: What Does the DCF Model Say?

Looking at UBE through the lens of our SWS DCF model, a different picture emerges. This method currently signals that the shares may actually be overvalued. This raises questions about whether value-seeking investors should pause for thought.

Look into how the SWS DCF model arrives at its fair value.

Build Your Own UBE Narrative

If you see things differently or want to dig deeper into UBE’s story, you can explore the numbers yourself and craft your own perspective in just a few minutes. Do it your way.

A great starting point for your UBE research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors are always lining up their next big opportunity. Don’t miss out. Broaden your radar now and give yourself an edge in finding tomorrow’s winners.

- Uncover affordable stocks poised for upside when you scan our picks for undervalued stocks based on cash flows based on their future cash flows.

- Tap into innovation by searching fast movers in artificial intelligence through our handpicked selection of AI penny stocks.

- Catch steady income streams by reviewing our curated list of dividend stocks with yields > 3% that offer attractive yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com