Diginex (DGNX): Valuation in Focus After Strategic ESG Partnership With Allocations Inc.

If you’re wondering what all the buzz is about with Diginex (NasdaqCM:DGNX) this week, you’re definitely not alone. The company just revealed a strategic relationship with Allocations Inc., aiming to bring its advanced ESG data collection and verification services directly into Allocations’ platform. This move empowers thousands of fund managers and advisers with better tools for responsible investing. By simplifying ESG integration, Diginex and Allocations are making it easier for the alternative investment community to respond to growing demands for transparency and measurable impact.

This partnership announcement seems to have caught investors’ attention. Over the month, Diginex’s stock price surged by 93%, with momentum only building. Shares are up 120% in the past three months. These jumps follow a stream of updates on Diginex’s acquisition strategy, suggesting the market is responding not just to the latest collaboration but also to the company’s broader push into ESG and data-driven services. Despite double-digit returns so far this year, the main spotlight remains on how these deals might drive sustainable growth.

So with shares rocketing higher, the real question for investors now is whether Diginex is shaping up to be a smart value play or if the market’s already factoring in its future ESG potential.

Price-to-Book of 626.1x: Is it justified?

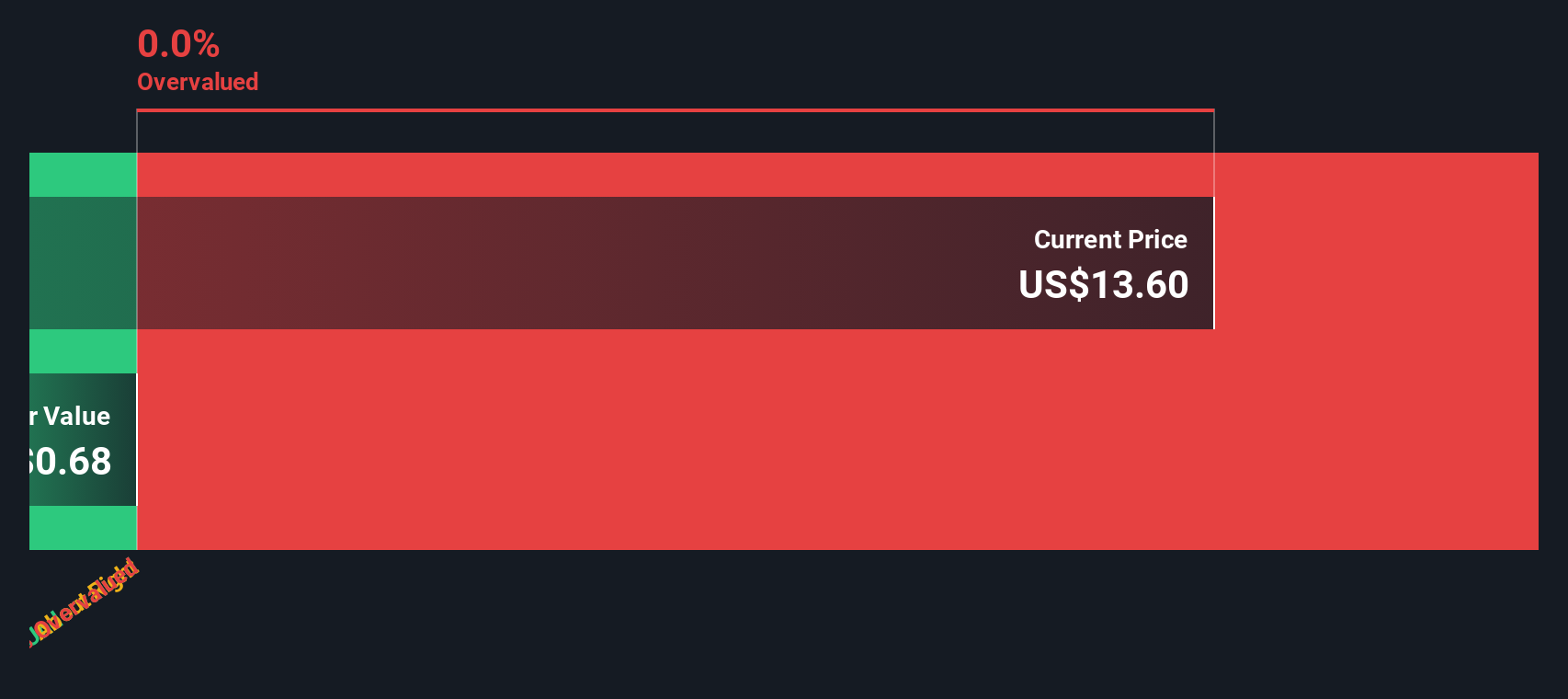

Based on its current price-to-book ratio, Diginex appears significantly overvalued both compared to US software peers and the broader industry average.

The price-to-book ratio compares a company's market capitalization to its book value, offering insight into how much investors are willing to pay relative to the company's net assets. For software firms, a price-to-book can indicate how the market values intangible assets and future growth potential.

With Diginex trading at 626.1 times its book value, while peers average only 2.8 times and the industry comes in at 4 times, the market is assigning a dramatic premium to the company. This high multiple suggests investors are banking on outsized future growth, but it may not be justified given its current financials.

Result: Fair Value of $2M (OVERVALUED)

See our latest analysis for Diginex.However, with negative net income and limited revenue growth, any faltering in execution or shifts in ESG demand could quickly dampen the recent optimism.

Find out about the key risks to this Diginex narrative.Another View: What Does the SWS DCF Model Indicate?

To check if the high price-to-book signals genuine long-term value, we can look to our DCF model for a different perspective. Interestingly, this valuation approach also suggests the stock may be priced at a premium. With multiple methods pointing in a similar direction, it may be worth considering whether investor expectations are ahead of reality.

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Diginex Narrative

If our analysis doesn’t match your perspective, or you’d rather dive into the details yourself, you can craft your own view of Diginex in just a few minutes. Do it your way.

A great starting point for your Diginex research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Why stop with just one opportunity when you could be in front of tomorrow’s winners? Tap into different market trends now and stay ahead of the crowd with these top picks:

- Uncover early growth stories and spot hidden leaders before the masses by checking out penny stocks with strong financials through penny stocks with strong financials.

- Gain an edge in the booming field of artificial intelligence by viewing top contenders making waves in next-generation tech with AI penny stocks.

- Boost your income potential and find companies offering generous yields with dividend stocks with yields > 3% for reliable dividend opportunities over 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com