Assessing Rubrik Shares After 24% Year-To-Date Surge and Microsoft Alliance News

If you own Rubrik stock or are eyeing it after a massive 157.0% rally over the past year, you are in good company. There is a real buzz around Rubrik, thanks to its YTD climb of 23.8% and a subtle 2.4% pop in the past week after some market reassessments. Of course, the ride has not been perfectly smooth; the stock dipped 6.1% over the past month as investors recalibrated their risk appetite in the face of broader market jitters and shifts in tech sentiment. For growth-oriented investors, these swings are like a siren’s song, promising both opportunity and volatility.

But is Rubrik really undervalued right now? According to our valuation score, Rubrik earns a 1 out of 6 on key undervaluation checks, which is a sign that, on paper, the shares are only ticking one major box for bargain hunters. Still, numbers only tell part of the story, and valuation is more art than science. Next, we will explore the main ways investors try to gauge whether Rubrik is a steal, or if much of its rapid growth is already priced in. Stay tuned, because at the end of this article, we will share a smarter lens for judging what the market might be missing about Rubrik’s true value.

Rubrik scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.Approach 1: Rubrik Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model is a common method investors use to estimate what a stock should be worth today by projecting the company’s future cash flows, and then discounting those cash flows back to their present value. For Rubrik, this approach relies on forecasting how much free cash the company will generate each year, then adjusting those future values to reflect what they would be worth right now, in today’s dollars.

Currently, Rubrik’s Free Cash Flow is $174.88 million. Analyst estimates are available for the next five years and suggest healthy growth, with free cash flow projected to reach approximately $765.9 million by 2030. These early projections come directly from analysts, but estimates after five years are extrapolated using Simply Wall St’s methods, providing a sense of continued growth beyond analyst coverage.

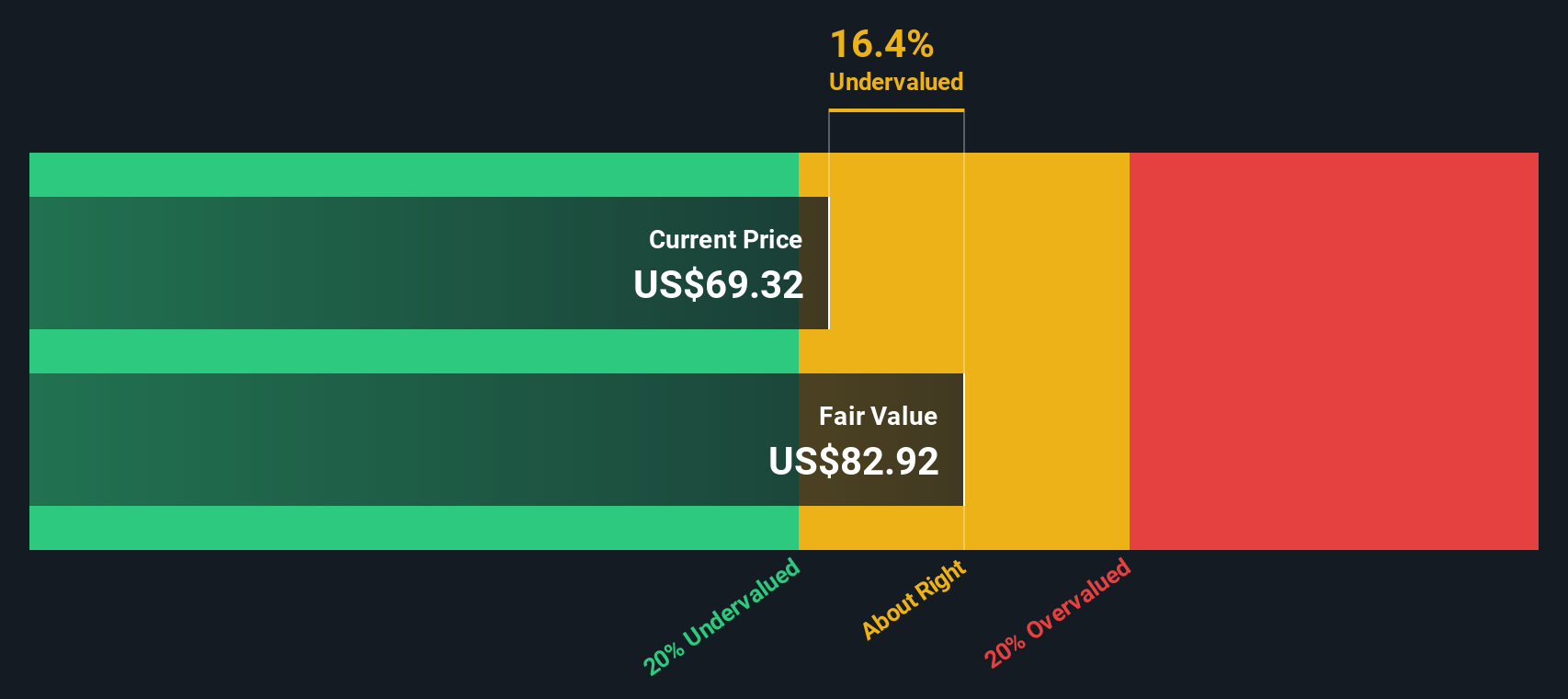

Using these forecasts, the DCF model sets an intrinsic fair value for the company of $80.39 per share. Compared to Rubrik’s current share price, this implies the stock is about 2.2% overvalued, a small premium that suggests the current price is just a bit higher than what the discounted cash flow analysis would support.

Result: ABOUT RIGHT

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Rubrik.

Approach 2: Rubrik Price vs Sales (P/S)

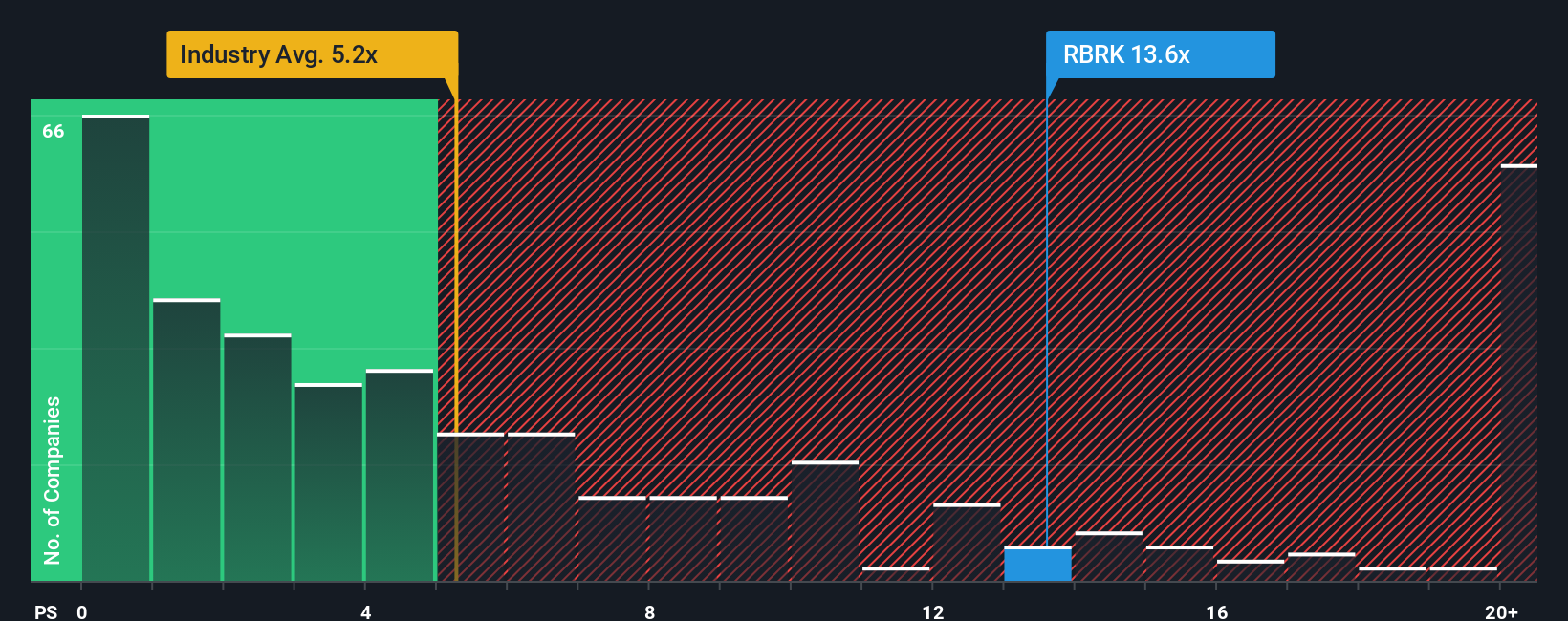

For growth-oriented tech companies like Rubrik, the Price-to-Sales (P/S) ratio is a favorite tool to estimate value because it is less affected by accounting quirks or the lack of current profitability, and it directly reflects how the market values every dollar of sales generated. The P/S ratio is particularly effective here since Rubrik's fast-expanding revenue base makes it easier to gauge the business’s scale and future potential than profit metrics alone.

Determining what a “normal” or “fair” P/S ratio should be depends on several big picture factors. High-growth businesses with strong market positions and lower risks usually command higher multiples, while more mature, slower-growing, or riskier companies trade at lower levels. In Rubrik’s case, its current P/S ratio is 15.0x, which stands well above the Software industry average of 5.3x and also higher than the peer group’s 10.6x. On its face, this signals that the market is pricing in robust expectations for Rubrik’s continued expansion and market share gains.

This is where Simply Wall St’s “Fair Ratio” comes in. Unlike a simple comparison to peers or industry averages, the Fair Ratio (12.2x for Rubrik) is a proprietary metric that weighs much more than just recent sales. It factors in future growth potential, profit margins, market cap, and risk. Because it adapts to the company’s unique profile, the Fair Ratio is a smarter benchmark for retail investors who want a clearer sense of fair value in a fast-changing sector like software.

Comparing Rubrik’s actual P/S ratio (15.0x) to its Fair Ratio (12.2x), we see the current valuation is somewhat ahead of the fundamentals and growth outlook implied by the Fair Ratio. This suggests investors are willing to pay a slight premium, but the difference is not massive.

Result: OVERVALUED

Upgrade Your Decision Making: Choose your Rubrik Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple concept. It is your perspective or “story” about what Rubrik’s future could look like, with your own expectations for revenue growth, profit margins, and a fair value. Instead of just relying on a formula or a consensus, you can connect your thesis about the business, such as strong product adoption, competitive risks, or sector tailwinds, to a set of numbers and see how that stacks up against the current share price.

Narratives seamlessly link a company’s story to a financial forecast and ultimately to a fair value, offering a holistic view of the opportunity or risk beyond traditional ratios. On Simply Wall St’s Community page, millions of investors use Narratives as an accessible tool to build, compare, and challenge their investment ideas. They help you decide when to buy or sell by showing where your estimates put Rubrik’s fair value versus the latest market price.

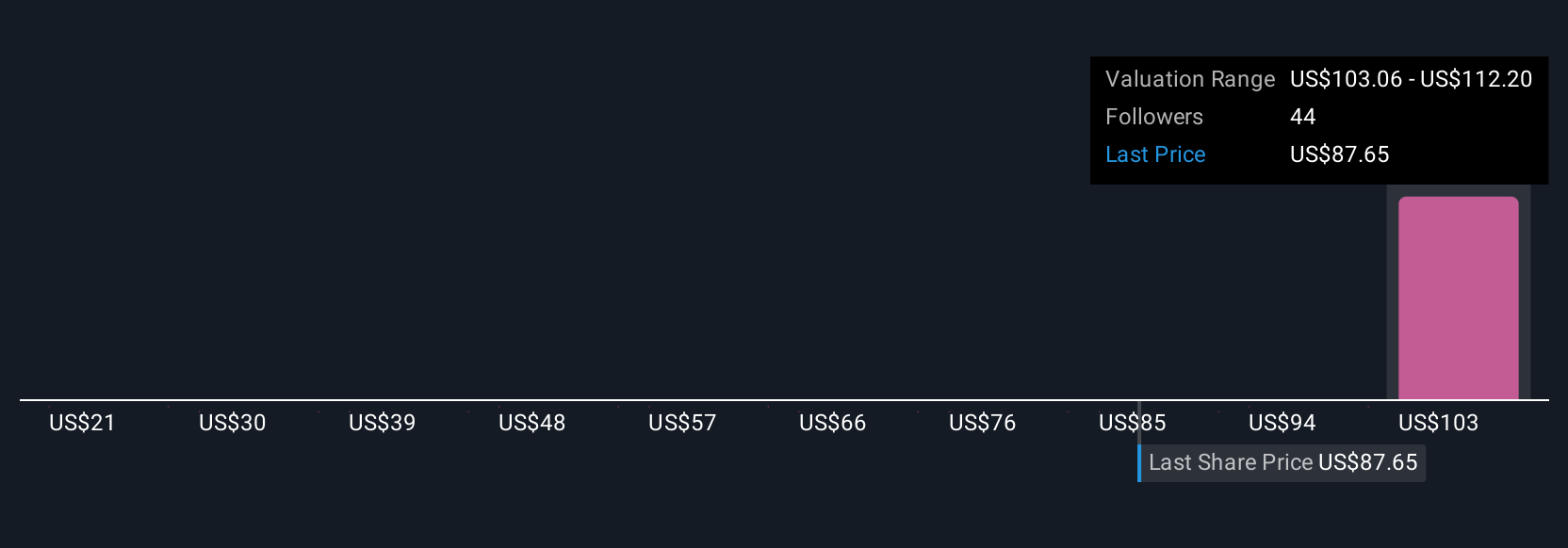

Best of all, Narratives update automatically as fresh news or earnings come in, so your view is always current. For example, among Rubrik investors on Simply Wall St, some believe the company should be worth as much as $125 per share, thanks to its leadership in cyber and AI-powered expansion, while others see more modest potential, capping fair value closer to $97, as they focus on competitive risks in a rapidly changing environment.

Do you think there's more to the story for Rubrik? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com