Does the Recent Weakness in Cognizant Shares Signal Opportunity for 2025?

If you are following Cognizant Technology Solutions or considering adding it to your portfolio, you are not alone. The stock is hovering at $66.98 per share, which has certainly caught the eye of investors watching for opportunities in this sector. Over the past week, the stock barely budged, up just 0.1%, but that flatness comes after a rockier ride recently. In the last month, shares slid -7.4%. Year-to-date, Cognizant is down -12.3%, and it is lagging over the last year as well with a -11.5% drop. Looking further back, however, a different picture emerges. Cognizant is up 22.5% over three years and 4.9% over five years, showing a knack for long-term resilience even as short-term sentiment wavers.

These price moves have unfolded against a backdrop of shifting market dynamics and changing risk appetites in the broader tech services industry. Investor perceptions of the sector’s threats and opportunities have clearly played a role in both the pullbacks and recoveries. So, is this an overlooked value play or a stock best left alone?

Diving into the numbers, Cognizant receives a value score of 6, which means it checks all six boxes used to spot undervalued companies. In the sections ahead, we will break down what this score actually means by examining different valuation methods. Most importantly, we will point you toward a smarter way to judge whether Cognizant is a buy today.

Why Cognizant Technology Solutions is lagging behind its peersApproach 1: Cognizant Technology Solutions Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting those amounts back to today's value. This approach helps investors compare what a company is really worth versus where its shares trade currently.

For Cognizant Technology Solutions, the most recent twelve months produced approximately $2.24 billion in Free Cash Flow. Analysts forecast these cash flows will steadily grow, reaching about $3.31 billion in 2028. Further gains are expected over the next decade as projections are extrapolated based on historical growth rates and industry context.

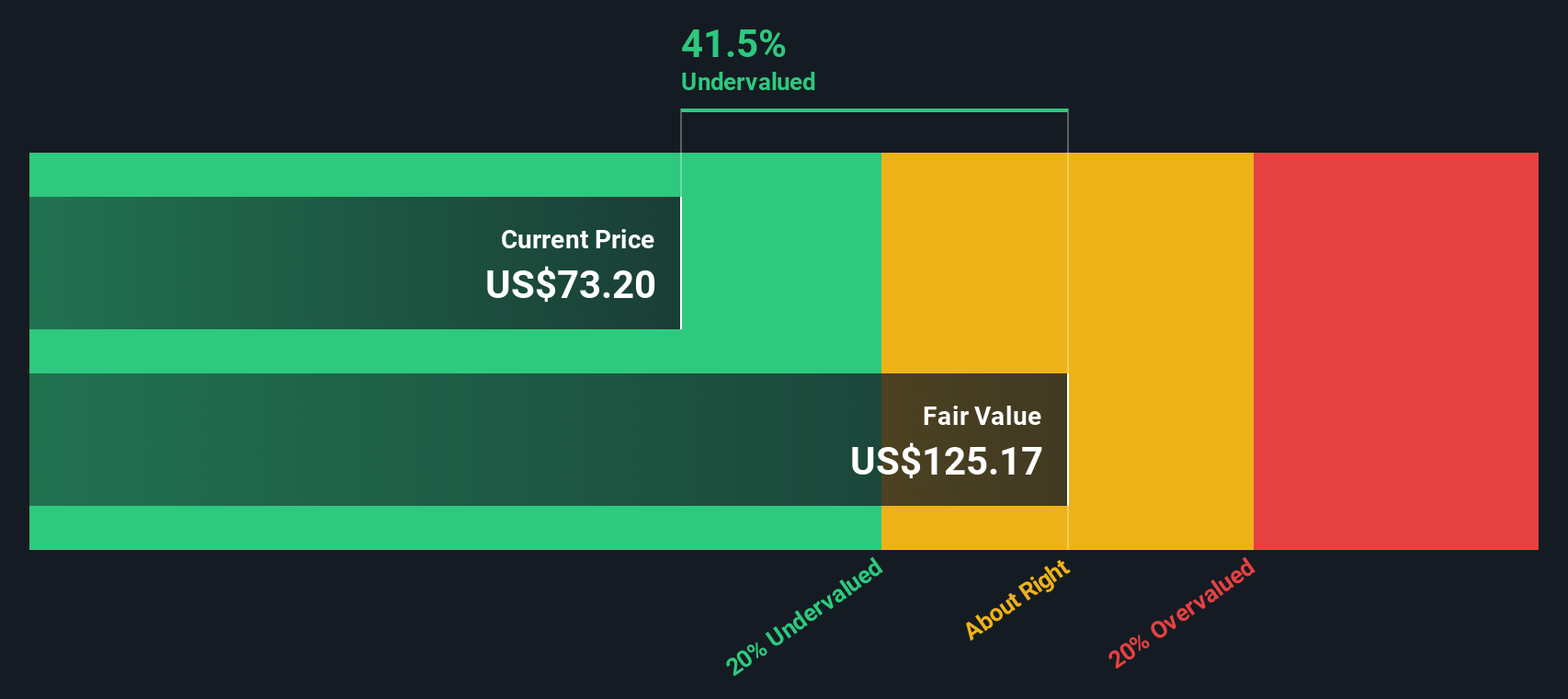

According to the DCF calculation, Cognizant's fair value per share is $118.27, which is significantly higher than its current trading price of $66.98. This spread represents a substantial intrinsic discount of 43.4 percent, indicating the stock trades well below its calculated worth.

In summary, the DCF approach portrays Cognizant as deeply undervalued by the market on a cash flow basis. For value-seeking investors, this could signal a promising buying opportunity based on the fundamentals.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Cognizant Technology Solutions.

Approach 2: Cognizant Technology Solutions Price vs Earnings

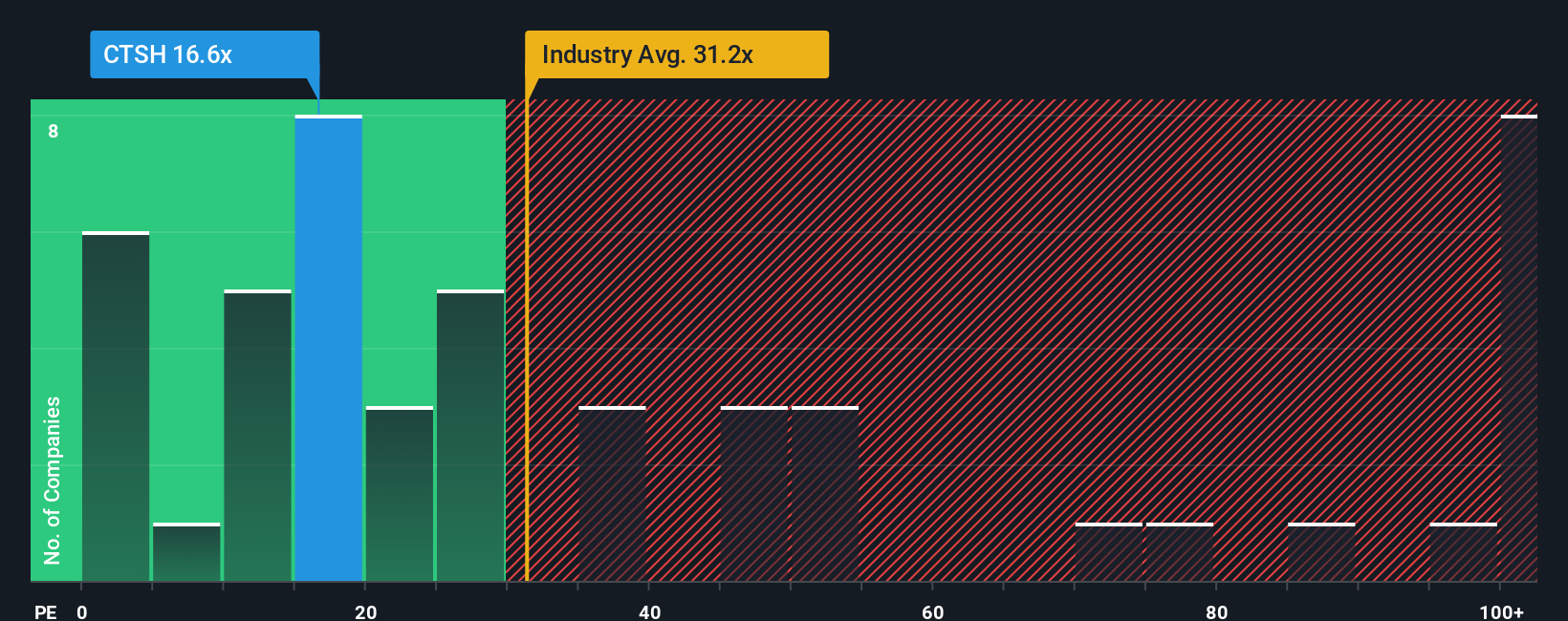

The Price-to-Earnings (PE) ratio is a widely used valuation metric for established, profitable companies like Cognizant Technology Solutions, as it directly relates the company’s share price to its underlying earnings power. This makes it especially helpful for comparing profitability and market expectations across similar businesses.

What constitutes a “normal” or “fair” PE ratio is shaped by a mix of factors, most notably a company’s anticipated growth and the amount of risk investors associate with its future. Higher growth expectations typically justify higher PE ratios. Conversely, elevated risk usually leads to lower multiples as investors demand more reassurance in returns.

Cognizant currently trades at a PE ratio of 13.4x, which is notably below both the IT industry average of 31.3x and the peer group average of 18.1x. At first glance, this could make the stock appear quite inexpensive relative to its competitors. However, Simply Wall St’s Fair Ratio for Cognizant stands at 33.5x. This Fair Ratio offers a more accurate benchmark as it blends together growth outlook, profit margins, sector trends, company size, and risk factors for a single, tailored valuation. Relying solely on industry or peer multiples can be misleading because it might not adjust for the specific attributes that shape Cognizant’s value proposition.

A comparison of Cognizant’s current PE of 13.4x to its Fair Ratio of 33.5x suggests a meaningful undervaluation, indicating the market may not be fully recognizing the firm’s earnings potential or risk profile.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your Cognizant Technology Solutions Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal story and forecast for a company like Cognizant Technology Solutions, combining your viewpoint on its future prospects with your estimates for revenue, earnings, margins, and a fair value that reflects your beliefs about where the business is headed.

Unlike static valuation methods, Narratives link what’s going on in the business such as new AI-driven services or shifting industry risks to a dynamic financial forecast and today’s fair value. This lets you see exactly how the story behind the numbers justifies a buy, hold, or sell decision. Narratives are a powerful yet easy-to-use tool available on Simply Wall St's Community page, where millions of investors can share and compare their perspectives.

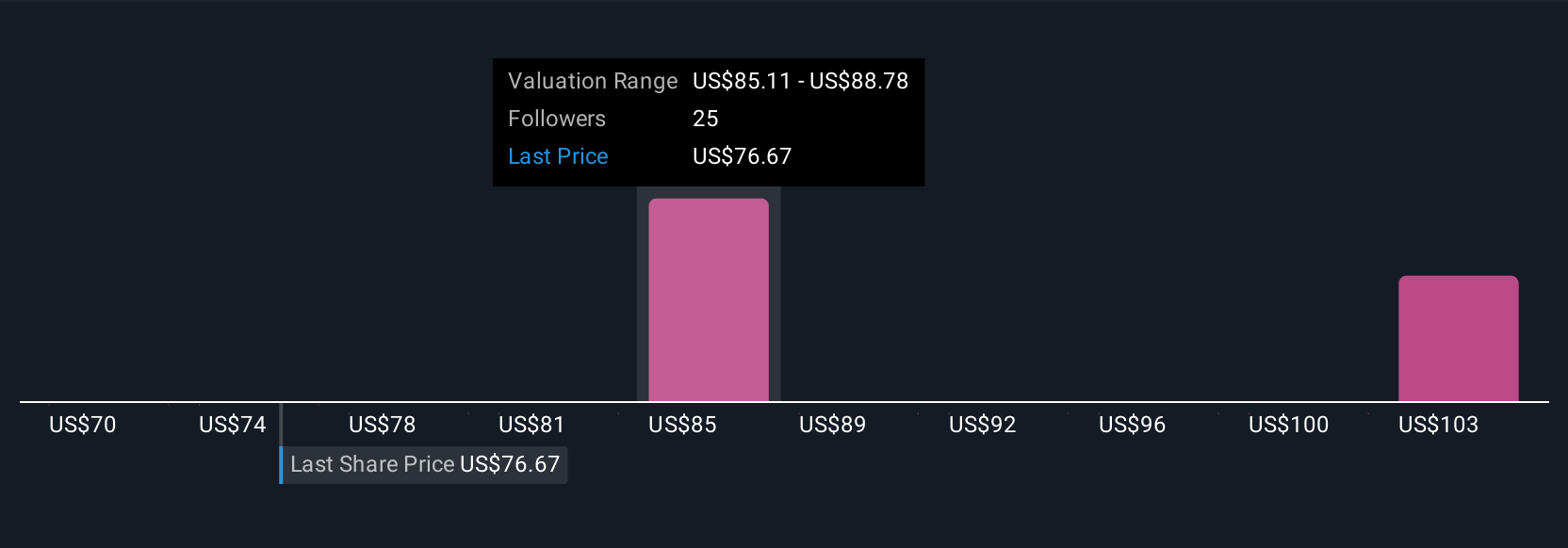

By building or following a Narrative, you can instantly see how your fair value estimate stacks up against the current share price, helping you decide when to act. Narratives are updated as soon as fresh news or financial results hit, so your viewpoint stays relevant. For example, one investor may believe Cognizant’s strong AI push justifies a bullish $103 price target, while another may be cautious and see only $75 as fair value. Narratives make it easy to see and test both approaches as the story evolves.

Do you think there's more to the story for Cognizant Technology Solutions? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com