How Does Lloyds Recent Rally Stack Up After Robust UK Consumer Spending News?

Thinking about what to do with Lloyds Banking Group stock right now? Many investors are weighing whether to hold on, buy more, or look elsewhere, especially with the bank’s share price putting on such a strong show over the past year. With a last close at £0.83, Lloyds has delivered impressive gains in nearly every recent time frame: up 1.0% in the last week, 0.5% for the month, and a whopping 50.8% year-to-date. Looking back further, those who have held for three or even five years have enjoyed cumulative returns of 134.4% and 284.5%, respectively. The share price strength has been supported in part by wider macro trends, such as resilient UK consumer spending and stabilizing interest rate expectations, which have boosted confidence in major banking groups like Lloyds.

Of course, with the stock riding high, the next important question is value. Is Lloyds still a bargain, or have recent returns pushed it into expensive territory? Looking at a standard valuation score across six common “undervalued” checks, Lloyds lands a 2 out of 6. In other words, the company passes two of the six measures often used to spot value opportunities. That number sets the stage for a deeper dive into the details. If traditional metrics are not giving you the full picture, stick around for an alternative angle that might reveal even more.

Lloyds Banking Group scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.Approach 1: Lloyds Banking Group Excess Returns Analysis

The Excess Returns valuation model is designed to assess how effectively a company generates profits above its cost of equity. Rather than focusing solely on cash flows, this method looks at the returns Lloyds earns on capital compared to what it costs to raise that capital from shareholders. Higher excess returns signal a business that can create real value, which is a positive marker for long-term investors.

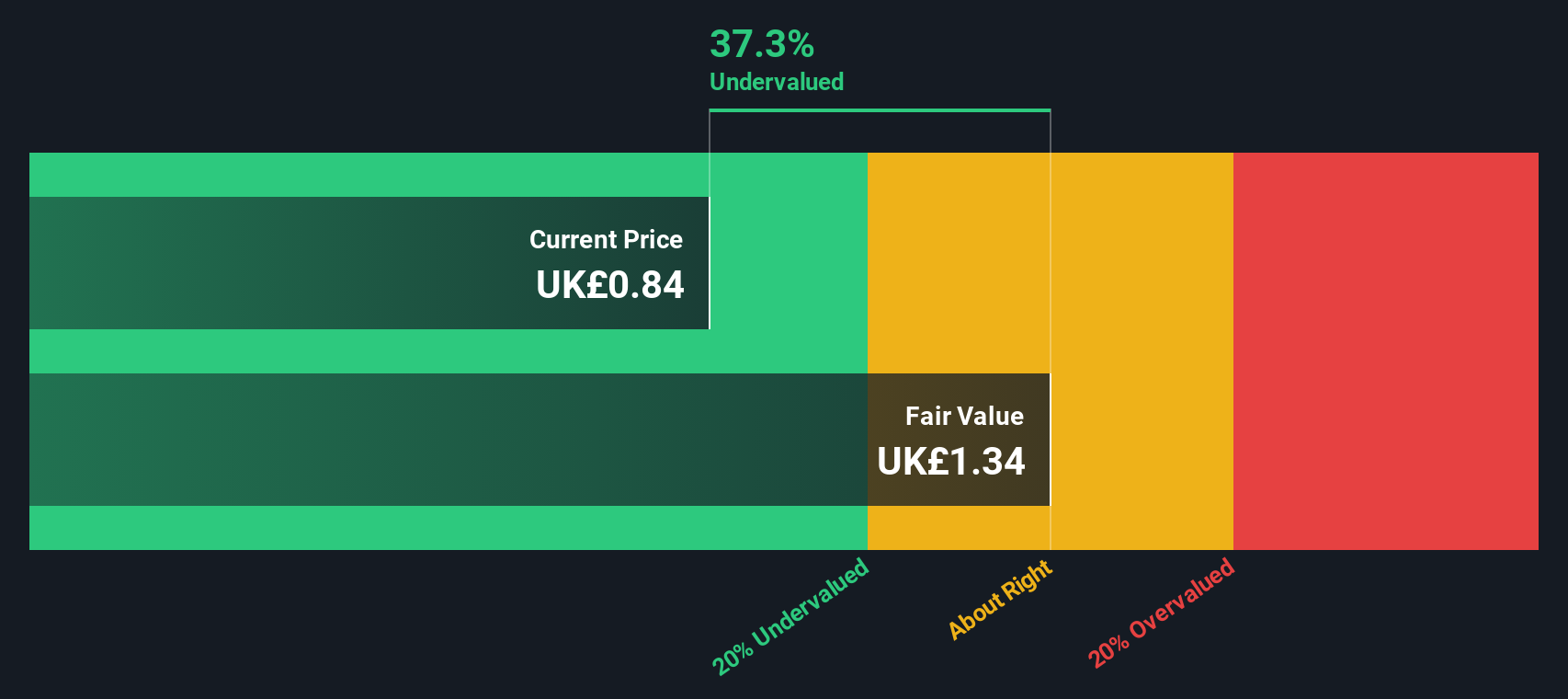

For Lloyds Banking Group, the latest estimates show a book value of £0.67 per share and a stable earnings per share (EPS) of £0.10, based on forecasts from 13 analysts. The company’s cost of equity stands at £0.07 per share, with an average return on equity of 12.58%. This produces an excess return of £0.03 per share, meaning the value generated above the company’s cost of funding is positive. Additionally, projections see Lloyds reaching a stable book value of £0.77 per share in the future, using weighted estimates from nine analysts.

Using this methodology, the intrinsic value per share is estimated at £1.32. With Lloyds’ actual share price currently at £0.83, this suggests the stock is trading at a 37.3% discount to its intrinsic worth, which indicates undervaluation.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Lloyds Banking Group.

Approach 2: Lloyds Banking Group Price vs Earnings

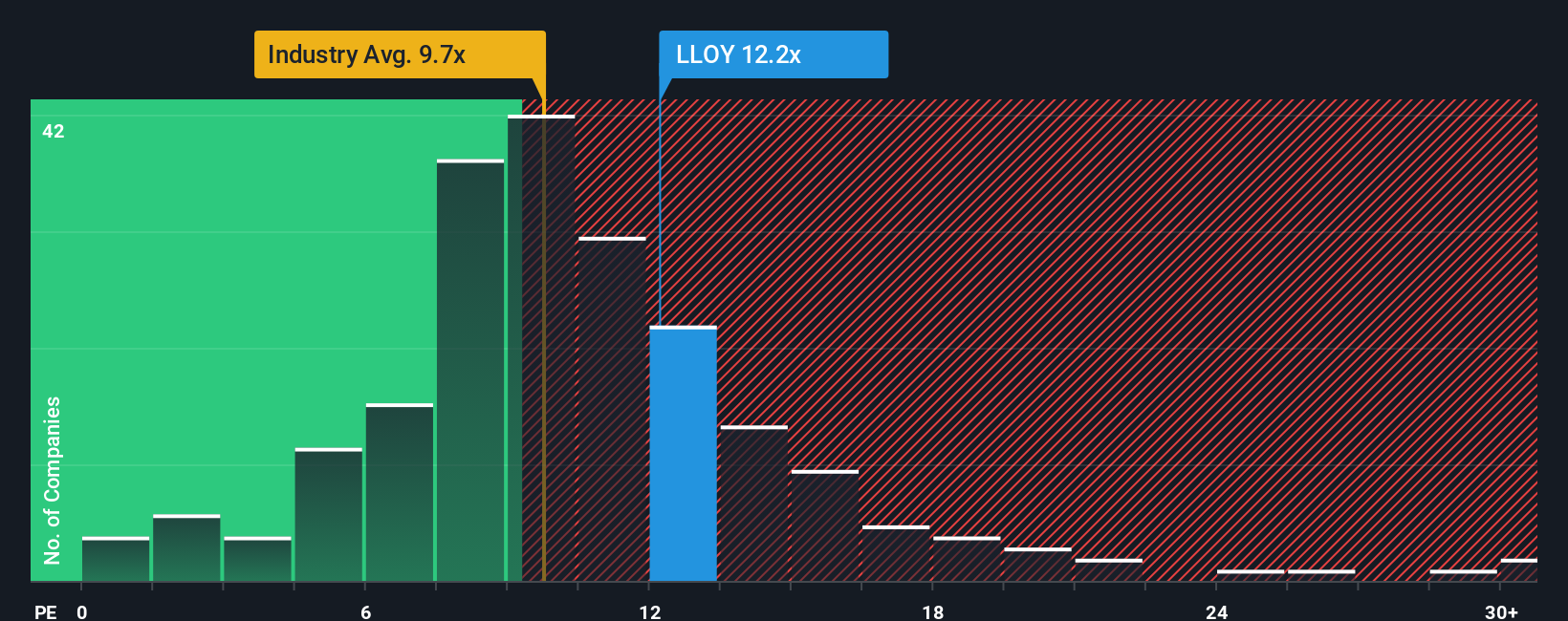

The Price-to-Earnings (PE) ratio is one of the most widely used valuation tools for profitable companies like Lloyds Banking Group. Because it relates market price to actual earnings, it helps investors gauge how much they are paying for each pound of profit generated by the company. Typically, a higher PE ratio may reflect higher growth expectations or lower perceived risk. In contrast, a lower PE could point to slower growth, greater risk, or an undervalued opportunity.

Lloyds currently trades at a PE ratio of 12.0x. For context, this is above both the industry average PE of 10.5x and the average among peers at 10.2x. At first glance, that might suggest the stock is a bit pricey. However, looking beyond simple averages can be more insightful. This is where Simply Wall St’s Fair Ratio comes in. Calculated in this case at 8.9x, the Fair Ratio is designed to give a more tailored view of what is reasonable to pay for Lloyds, because it takes into account not only industry benchmarks but also factors unique to the company, such as its earnings growth outlook, risk profile, profit margins, and size.

Comparing the current PE of 12.0x to the Fair Ratio of 8.9x shows that Lloyds is trading at a premium on this basis. This suggests that, at least on earnings, the stock may be somewhat overvalued according to the comprehensive criteria considered in the Fair Ratio.

Result: OVERVALUED

Upgrade Your Decision Making: Choose your Lloyds Banking Group Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is a simple, yet powerful way to articulate your personal view or story about Lloyds Banking Group. It connects your beliefs about its business future to a detailed financial forecast and a calculated fair value. Think of Narratives as the bridge between what you know about the company, your expectations for its future, and what that means for its intrinsic value.

Available on Simply Wall St’s Community page and trusted by millions of investors, Narratives make sophisticated investment thinking accessible. They allow you to craft your perspective, whether you see Lloyds as set to dominate through digital transformation, or worry that UK economic headwinds could hold back growth, and quantify it in real numbers. You can compare the fair value implied by your Narrative with the current share price to decide whether to buy, hold, or sell.

Narratives are always evolving as new news or earnings are released, helping you stay up to date and adjust your view automatically. For instance, one investor’s Narrative might predict Lloyds’ digital transformation will drive earnings above £6.9 billion and a fair value near £1.03, while another could be concerned about margin pressures and set a much lower outlook closer to £0.53.

Do you think there's more to the story for Lloyds Banking Group? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com