Is MEG Energy Fairly Priced After Its Exceptional Five Year Performance in 2025?

If you have been eyeing MEG Energy and wondering whether now is the right time to make a move, you are not alone. This stock has had quite a journey, turning heads with a staggering 961.4% return over the past five years. Even if you zoom in a little closer, the numbers are impressive: up 94.8% over three years, with a healthy 18.0% gain year to date. Yet, the recent mood has been a touch more cautious, with the stock dipping -2.4% over the past week, despite not much in the way of major news moving the market.

So, what is behind MEG Energy's long-term climb and its current, more measured pace? A lot of it comes down to market sentiment about energy stocks in general, especially with ongoing shifts in oil prices and renewed global attention on Canadian oil sands producers. Investors are weighing the growth potential against new risks and volatility, resulting in some short-term ebb and flow in the share price.

If you are evaluating your next move, you are probably eager to know whether MEG Energy’s current price justifies optimism, caution, or somewhere in between. That is where a solid valuation deep-dive comes in. By most traditional measures, MEG Energy scores a 3 out of 6 on value checks for being undervalued, meaning it clears half of the main hurdles analysts use to spot a bargain. However, as you will see, there is more than one way to judge value. The most insightful approach is discussed last.

Why MEG Energy is lagging behind its peersApproach 1: MEG Energy Discounted Cash Flow (DCF) Analysis

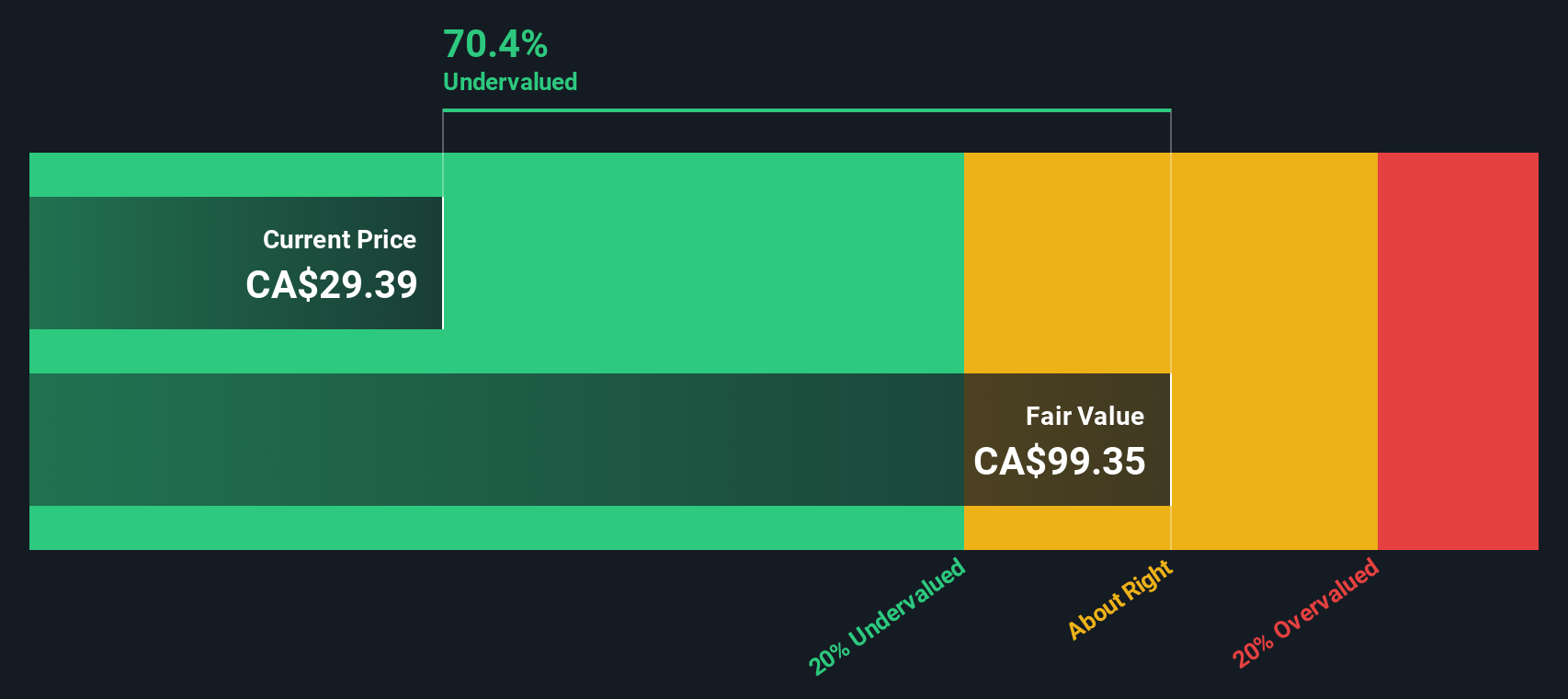

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s value. This helps investors determine what the business is really worth at present.

For MEG Energy, the most recent Free Cash Flow (FCF) was CA$976 million. Analysts forecast upcoming FCFs up to 2028, with projected values steadily rising and reaching CA$725 million. Looking further out, Simply Wall St extrapolates ten-year projections that go as high as CA$1.23 billion by 2035, reflecting expectations of ongoing growth.

When all these cash flows are discounted using the 2 Stage Free Cash Flow to Equity method, the estimated fair value for MEG Energy is CA$99.57 per share. This implies an intrinsic discount of around 71.6 percent, indicating that the market is currently pricing MEG Energy well below what its future cash flows suggest is fair.

This substantial discount suggests that MEG Energy is currently undervalued by the market according to this DCF analysis.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for MEG Energy.

Approach 2: MEG Energy Price vs Earnings

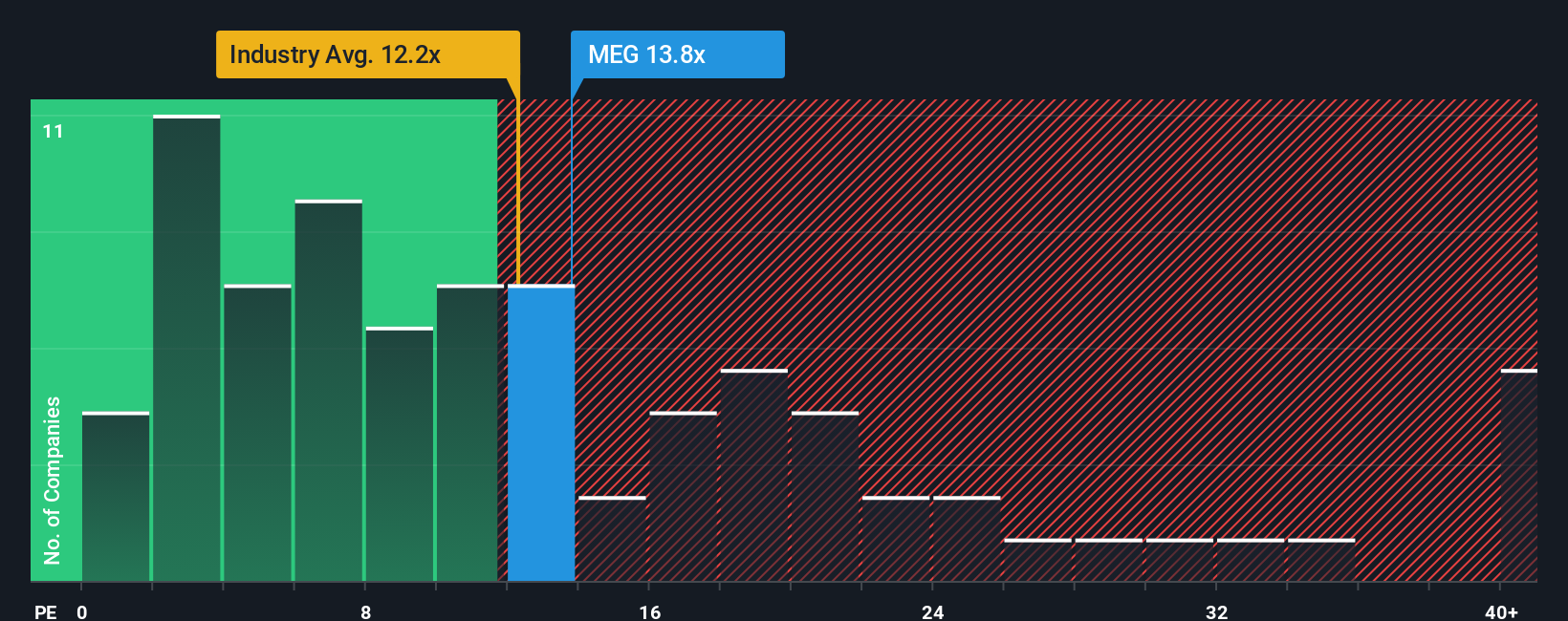

For profitable companies like MEG Energy, the Price-to-Earnings (PE) ratio is one of the most widely used metrics to assess valuation. The PE ratio reflects how much investors are willing to pay for each dollar of a company’s earnings, making it a useful benchmark for comparing similar businesses within the same sector.

Growth expectations and perceived risk strongly influence what a “normal” or “fair” PE ratio should be. Companies with robust earnings growth and lower risk profiles often command higher PE ratios, while those with greater uncertainties or slower growth tend to trade at a discount.

Currently, MEG Energy trades at a PE ratio of 13.1x. For context, this is slightly above the Oil and Gas industry average of 12.3x, but significantly below the average of its listed peers at 29.0x. These comparisons can offer a quick perspective, but have their limitations since they do not account for company-specific growth, profitability, or risk factors.

This is where Simply Wall St’s Fair Ratio comes in. The Fair Ratio for MEG Energy is calculated at 11.8x and incorporates factors like its earnings growth, profit margin, market cap, risks, and its specific position within the industry. Unlike a raw peer or industry comparison, the Fair Ratio provides a more tailored benchmark that adapts to the company’s individual context.

With MEG Energy’s actual PE ratio (13.1x) just slightly above its Fair Ratio (11.8x), the difference is minimal and the stock appears to be priced about right by the market when examined through this lens.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your MEG Energy Narrative

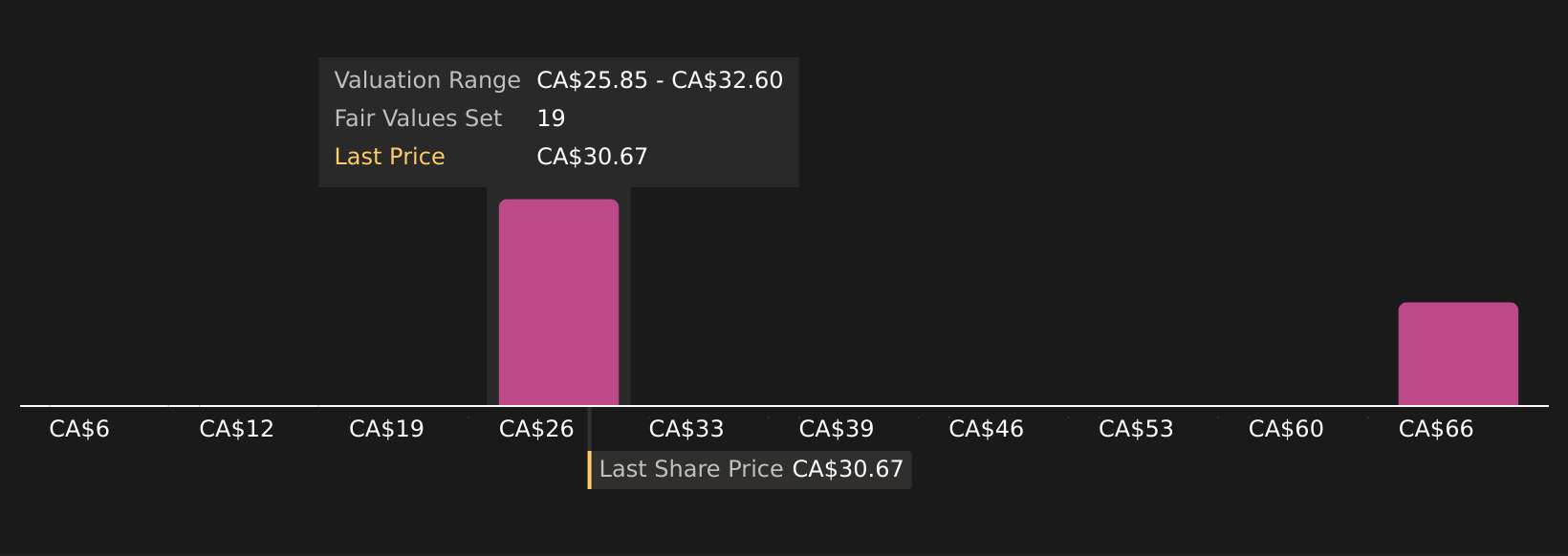

Earlier, we mentioned there is an even better way to understand valuation, so now let’s introduce you to Narratives. A Narrative is a clear story that connects what you believe about a company, such as MEG Energy’s future opportunities and risks, to a financial forecast and, ultimately, your own fair value estimate.

Instead of relying only on static ratios or analyst reports, Narratives help you define your personal outlook by allowing you to input your assumptions about future revenues, profit margins, and market conditions. This approach transforms numbers into a meaningful, customizable story and makes investing more accessible and insightful for everyone.

Narratives are central to Simply Wall St’s Community page, where millions of investors explore, share, and compare perspectives on hundreds of stocks. You can easily see whether your Narrative signals MEG Energy is undervalued or possibly overvalued by comparing its Fair Value, based on your assumptions, to the current share price.

What makes Narratives especially powerful is that they are updated automatically whenever new information, such as earnings results or breaking news, becomes available. This keeps your analysis relevant and timely.

For example, some investors see MEG Energy as having a CA$33.0 fair value based on aggressive growth and expansion, while others set a more cautious target of CA$24.0. This shows how Narratives let every investor infuse their own conviction and research into their decisions.

Do you think there's more to the story for MEG Energy? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com