Viva Energy (ASX:VEA): Assessing Valuation Following Leadership Changes in the Convenience and Mobility Division

Viva Energy Group (ASX:VEA) is in the spotlight following some big moves in the leadership team of its Convenience and Mobility division. With CEO Jevan Bouzo stepping down and Jennifer Gray, the Group COO, stepping up as Interim CEO, investors are watching closely to see how the company manages this pivotal transition. Leadership shifts like this often draw attention, since new decision-makers can shape company strategy and influence its execution. Both of these factors matter to anyone holding or considering buying VEA shares.

These executive changes arrive at a challenging moment for Viva Energy Group. Over the past year, the stock has trended lower, reflecting lingering uncertainty and shifting momentum. While the five-year return is still solidly positive, both short- and long-term performance have come under pressure, with a negative return so far this year and the stock down sharply in the past month. Investors seem to be weighing the potential impact of recent management moves alongside the company's financial trajectory.

After a year marked by setbacks and now a shake-up at the top, it’s worth asking: is the market pricing in all the risks, or could this transition open the door to undervalued growth for patient investors?

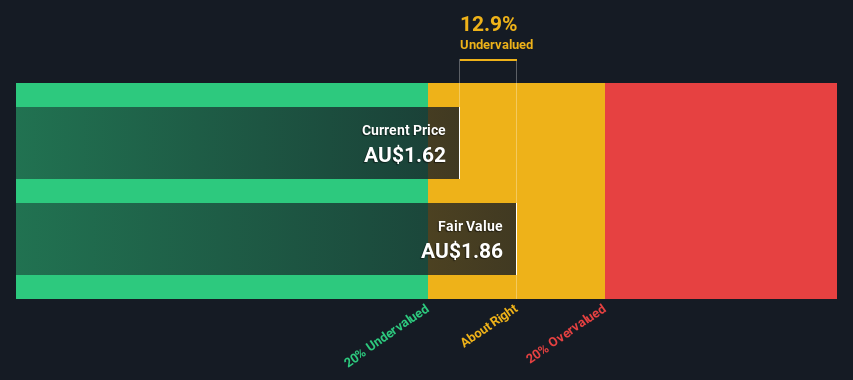

Most Popular Narrative: 28% Undervalued

According to the most widely followed narrative, Viva Energy Group's shares are considered significantly undervalued, with a fair value estimate meaningfully above the current price.

The ramp-up in retail network conversions to OTR branded stores, with demonstrated increases in sales and higher-margin non-fuel offerings, is expected to materially lift revenue and improve overall net margins as consumer demand for convenience retail and fast food continues to rise. This trend aligns with ongoing Australian urbanization and busy lifestyles.

Want to know what’s fueling this bullish outlook? The secret is in their bold transition strategy and ambitious growth forecasts, supported by impressive profit and margin targets. Curious about the assumptions behind these elevated expectations? Unlock the narrative to discover the financial leaps and strategic shifts analysts believe could power the next phase of Viva Energy’s valuation.

Result: Fair Value of $2.57 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent regulatory pressures or weak results from convenience store conversions could quickly erode margins and force a reassessment of Viva Energy’s outlook.

Find out about the key risks to this Viva Energy Group narrative.Another View: Discounted Cash Flow Analysis

Taking a different angle, our SWS DCF model also points to Viva Energy shares being undervalued. This method looks ahead at future cash flows and supports the earlier fair value assessment. Could the market be missing something?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Viva Energy Group Narrative

If you see the story differently or prefer hands-on analysis, it only takes a few minutes to chart your own path using our tools. Do it your way.

A great starting point for your Viva Energy Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let great opportunities pass you by. Use the Simply Wall St screener now to find companies that could fuel your next winning investment move.

- Unlock serious yield potential in today’s market when you browse dividend stocks with yields over 3% by checking out dividend stocks with yields > 3%.

- Focus on market bargains and make undervaluation work in your favor using our powerful tool for undervalued stocks based on cash flows.

- Explore the future of innovation and growth by reviewing cutting-edge AI penny stocks that are set to transform entire industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com