A Fresh Look at Air Canada (TSX:AC) Valuation Following Bold Route Expansion and Network Changes

Air Canada (TSX:AC) just rolled out a slate of new network changes that could catch investors’ attention. The airline is adding year-round flights from Ottawa to both Fredericton and Moncton, alongside a new Vancouver to Fort McMurray connection coming this December, while also increasing service from Toronto to Sudbury. At the same time, Air Canada is trimming less profitable routes, suspending service to Bathurst and North Bay at the end of January. These moves are part of a bigger push that also includes more international routes, such as Montreal to Sicily and Palma de Mallorca, and new long-haul offerings with its upgraded Airbus A321XLR fleet coming online in 2026.

These network updates come on the heels of a year where Air Canada’s share price swung higher, gaining 19% over the past twelve months after some tougher stretches earlier in 2025. Over the longer term, the momentum has been more muted. The last three and five years delivered milder returns, so this recent lift stands out. The stock’s trajectory reflects both optimism around travel demand and ongoing caution as the company navigates reinvention and shifting industry dynamics. Expanded domestic and international routes, coupled with a refreshed fleet, point to a strategy focused on growth and market share, even if trade-offs like route suspensions can add near-term uncertainty.

After this year’s sharper gains for Air Canada, is the stock primed for another run as profits catch up, or has the market already factored in these bold moves?

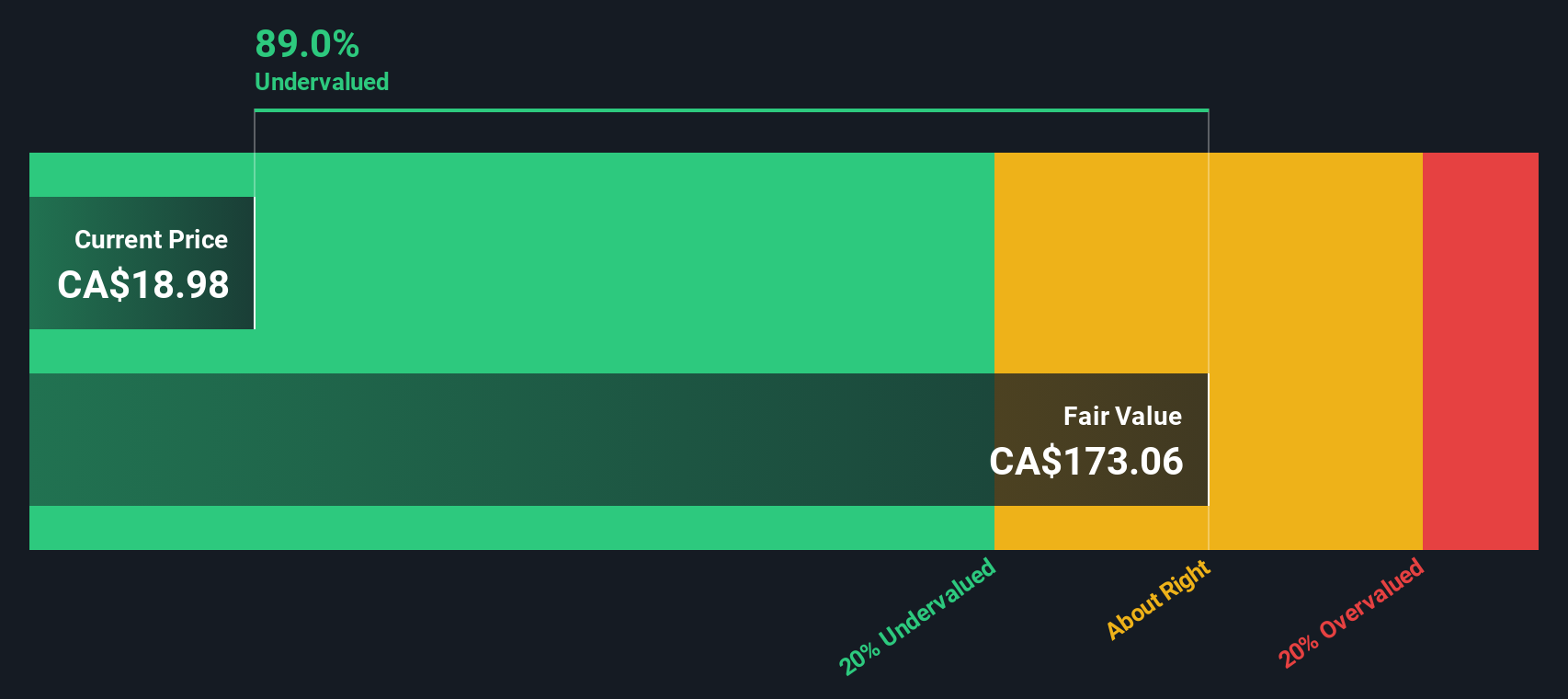

Most Popular Narrative: 24.7% Undervalued

The most widely followed narrative suggests Air Canada is trading well below its estimated fair value, with future growth and earnings potential underpinning the case for significant upside.

Robust and sustained demand for international travel, driven by rising global middle-class incomes and increased appetite for experiences, continues to benefit Air Canada's transatlantic and Asia-Pacific routes. This supports long-term revenue growth and market share expansion.

How is Air Canada set to defy expectations? The most popular narrative banks on outsized international demand, ambitious network growth, and a future profit multiple that challenges industry norms. Want to know which headline numbers, profit swings, and bold projections are powering this eye-catching valuation? Follow the narrative to uncover the math and insight behind Air Canada's bullish fair value.

Result: Fair Value of $25.29 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, rising labor costs and increasing competition on key international routes could challenge Air Canada's earnings momentum and put pressure on future valuations.

Find out about the key risks to this Air Canada narrative.Another View: SWS DCF Model

Taking a step back from market-based comparisons, our DCF model values Air Canada based on its projected future cash flows. This method also suggests the shares are undervalued. However, can any model truly account for all the complexities of this industry?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Air Canada Narrative

If these conclusions don't quite align with your take, you can always dive into the numbers and build out your personal story in just a few minutes using Do it your way.

A great starting point for your Air Canada research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let opportunity pass you by. This is an ideal moment to expand your watchlist with smart choices that match your goals and interests.

- Capitalize on the AI boom by targeting the innovators making real waves in machine learning, all highlighted in our AI penny stocks.

- Boost your passive income strategy by selecting companies with consistently high yields found through our dividend stocks with yields > 3%.

- Spot tomorrow’s growth stories at a bargain by screening for undervalued businesses using our undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com