Valuing Carl Zeiss Meditec (XTRA:AFX) After Recent Share Price Drop and Analyst Outlook

If you have been keeping an eye on Carl Zeiss Meditec (XTRA:AFX), you may have noticed the sharp drop in its share price over the past three months. Despite a 19% slide, the company’s core fundamentals still look steady, and management has continued to pay dividends. This is a reassuring sign for investors uneasy about volatility. With some experts projecting a turnaround in earnings and profitability on the horizon, the market’s negative reaction raises a big question for anyone considering what to do next with the stock.

This recent dip comes after a period where Carl Zeiss Meditec’s long-term returns have generally trailed the broader healthcare sector. Shares are down about 23% over the past year and more than 54% for the past three years, reflecting fading long-term momentum. Yet, the fundamentals tell a steadier story: return on equity is roughly in line with peers, and annual net income growth is holding up better than many industry counterparts. Consistent dividend payouts for over a decade also hint at a management team committed to shareholder value through various cycles.

So, as the stock trades at a sizeable discount to its recent highs, is this just the market getting ahead of fundamental reality, or could there be genuine value here for those willing to bet on a rebound?

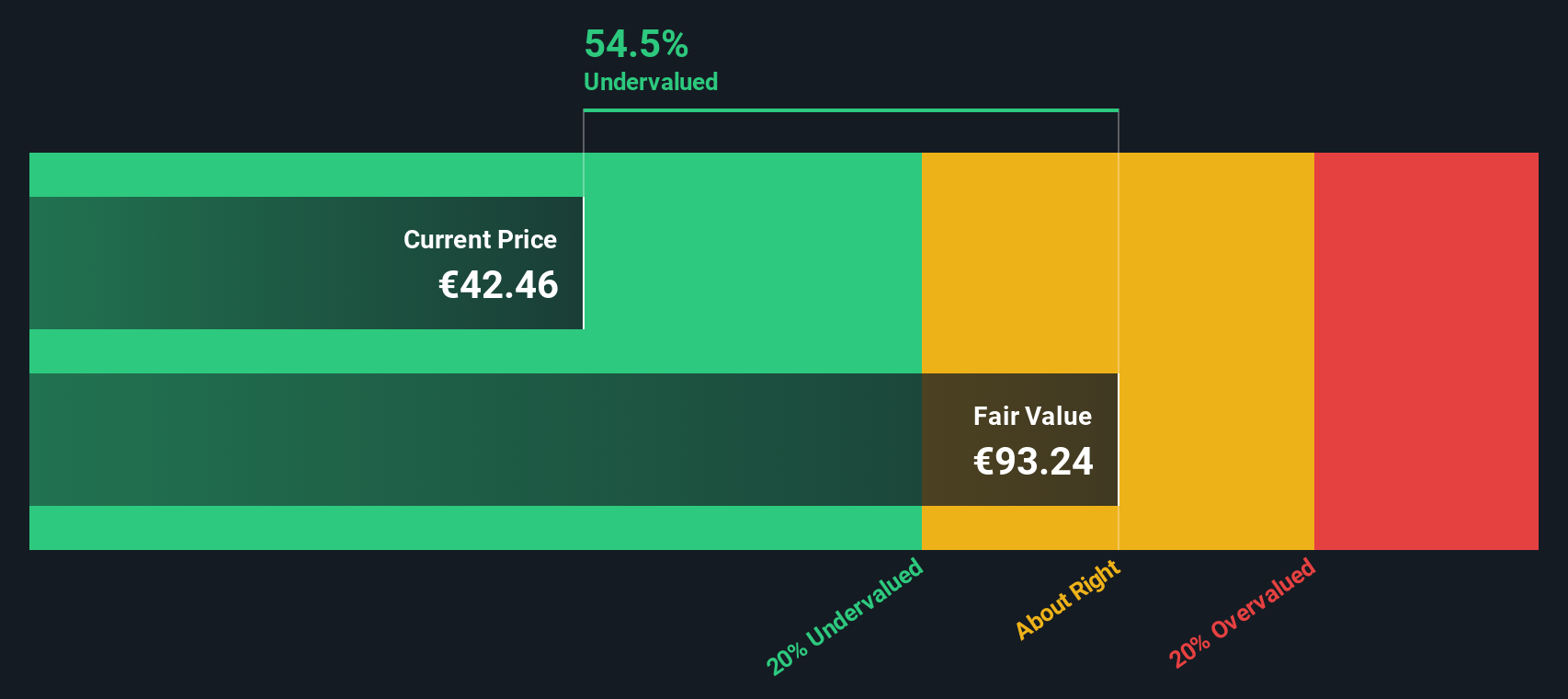

Most Popular Narrative: 14.3% Undervalued

According to the prevailing narrative, Carl Zeiss Meditec is seen as fundamentally undervalued, with a 14.3% discount to fair value based on future earnings projections and analyst consensus.

The recent approval of the VISUMAX 800 in China, earlier than expected, positions Carl Zeiss Meditec AG for potential revenue growth. The launch is expected to boost higher ASP (Average Selling Price) for both devices and treatment packs, enhancing future revenue streams.

Curious what’s fueling this valuation call? There are ambitious growth assumptions supporting these figures, spanning revenue, profit margins, and a profit multiple that differs from the sector norm. Is the fair value really justified by these bold forecasts, or is there more to the story? Discover the financial calculations shaping this market perspective.

Result: Fair Value of €53.61 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, sustained margin pressure and weak demand in China could quickly undermine these upbeat projections. Investors should watch industry trends closely.

Find out about the key risks to this Carl Zeiss Meditec narrative.Another View: Discounted Cash Flow Analysis Weighs In

Adding to the picture, our SWS DCF model paints a much more optimistic outlook. It suggests that Carl Zeiss Meditec may be trading well below its true value. Could this model be seeing something the market is missing?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Carl Zeiss Meditec Narrative

If you think there's another angle or have different insights, you can quickly pull together your own perspective using the available data and tools. Do it your way Do it your way.

A great starting point for your Carl Zeiss Meditec research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Unlock fresh opportunities by tapping into smarter stock screens designed to help you stay ahead. Don’t let your next big win slip through the cracks.

- Spot tech trailblazers making breakthroughs in artificial intelligence when you check out the latest picks among AI penny stocks.

- Target high-yield returns by scanning companies known for strong cash payouts using our handpicked dividend stocks with yields > 3%.

- Catch hidden bargains trading below their true value with the top selection of undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com