Sprott (TSX:SII) Valuation in Focus After New ETF Launch and Index Expansion in Metals and Mining

Price-to-Earnings of 38.8x: Is it justified?

Sprott is currently valued at a price-to-earnings (P/E) ratio of 38.8x, which is significantly higher than both its industry peers and the broader Canadian capital markets sector. This high multiple suggests that investors are paying a premium for Sprott's current and anticipated future earnings compared to similar companies.

The P/E ratio measures how much investors are willing to pay for each dollar of company earnings. In sectors such as capital markets, where revenue and profit can be cyclical, this ratio often indicates whether the stock is perceived as a growth opportunity or is being overvalued due to strong recent performance.

Given that Sprott's P/E is well above the industry average of 9.6x and the peer average of 17x, the market appears to be pricing in strong future growth or other positive factors that go beyond current sector norms. However, with earnings growth of 20.5% last year, investors should consider whether such a premium is justified based on the company's longer-term growth prospects and profit sustainability.

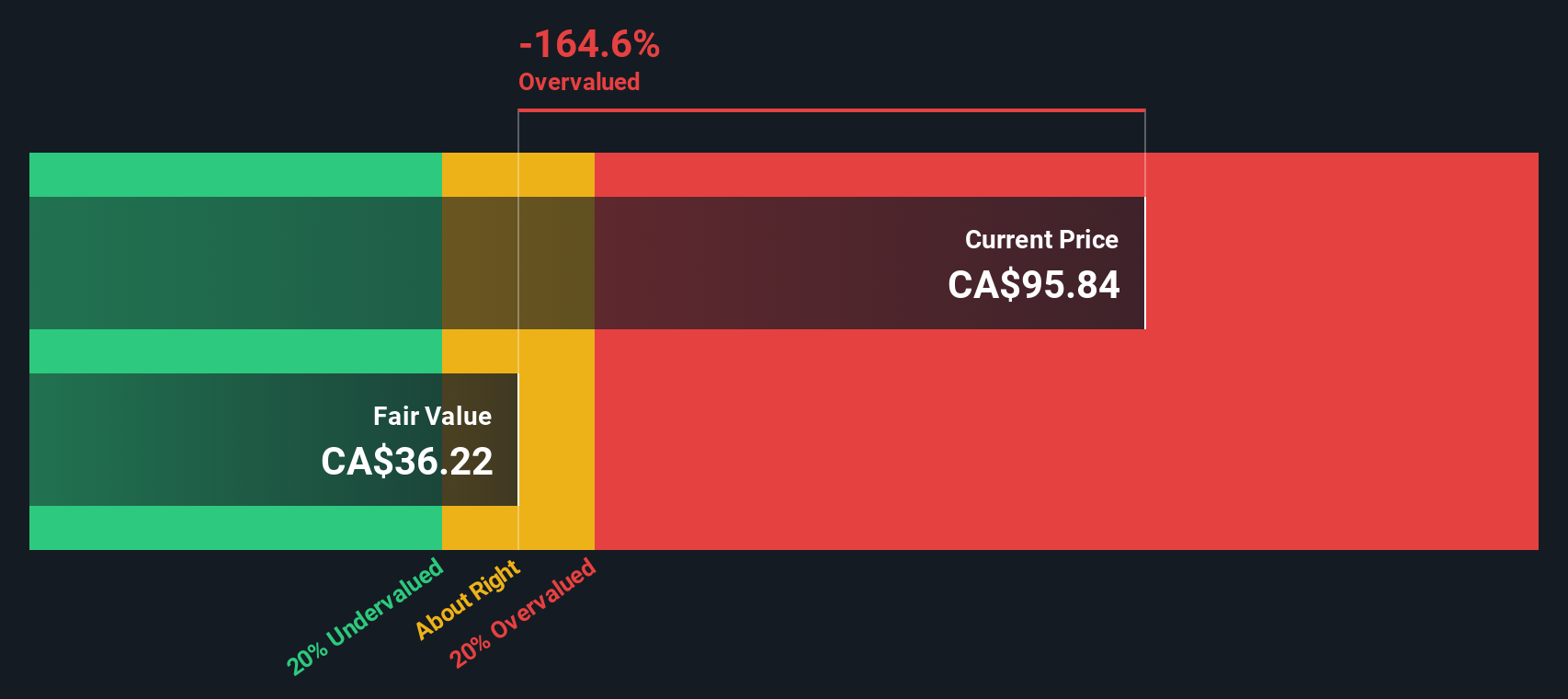

Result: Fair Value of $37.58 (OVERVALUED)

See our latest analysis for Sprott.However, slower revenue growth or a drop in sector momentum could quickly challenge the current valuation premium and reduce investor enthusiasm.

Find out about the key risks to this Sprott narrative.Another View: Our DCF Model Tells a Similar Story

The SWS DCF model, which estimates fair value using future cash flows, also finds Sprott trading above its intrinsic value. Both methods highlight the premium investors are paying. What could change this outlook?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Sprott Narrative

If you see things differently, or want to dig into the numbers yourself, you can craft your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Sprott.

Looking for More Investment Ideas?

Your next great opportunity could be just a click away. Step up your strategy and seize the moment with these handpicked themes worth your attention:

- Capture the potential of undervalued companies and get ahead of the market by using our undervalued stocks based on cash flows.

- Tap into the rise of next-generation medicine with our selection of healthcare AI stocks, leading innovation in health and artificial intelligence.

- Maximize your passive income by finding top picks among dividend stocks with yields > 3%, offering strong yields and solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com