Firefly Aerospace’s Valuation in Focus Following New $10M NASA Lunar Data Contract Expansion

Firefly Aerospace (FLY) made headlines this week, thanks to a $10 million NASA contract addendum that extends its participation in the Commercial Lunar Payload Services (CLPS) initiative. After the company’s Blue Ghost Mission 1 became the first commercial mission to land successfully on the Moon, NASA moved to acquire extra scientific and operational data. Firefly is providing a substantial volume of high-definition images and unique lunar performance insights. For investors, this contract highlights not only a technical achievement, but also signals Firefly’s growing reputation as a preferred partner for lunar exploration and data services. This development could open doors for future NASA business.

This announcement follows several eventful months for Firefly. While the recent revenue guidance for 2025 points to growth, the past year brought a share price decline, with the stock down 18% year-to-date. However, momentum appears to be building again, as shares rose nearly 10% in a single day and are up 13% over the past week. The contract win, combined with steady progress on rocket launches and data sales, is attracting renewed attention from investors who have been waiting to see if Firefly can turn its innovations into real revenue streams.

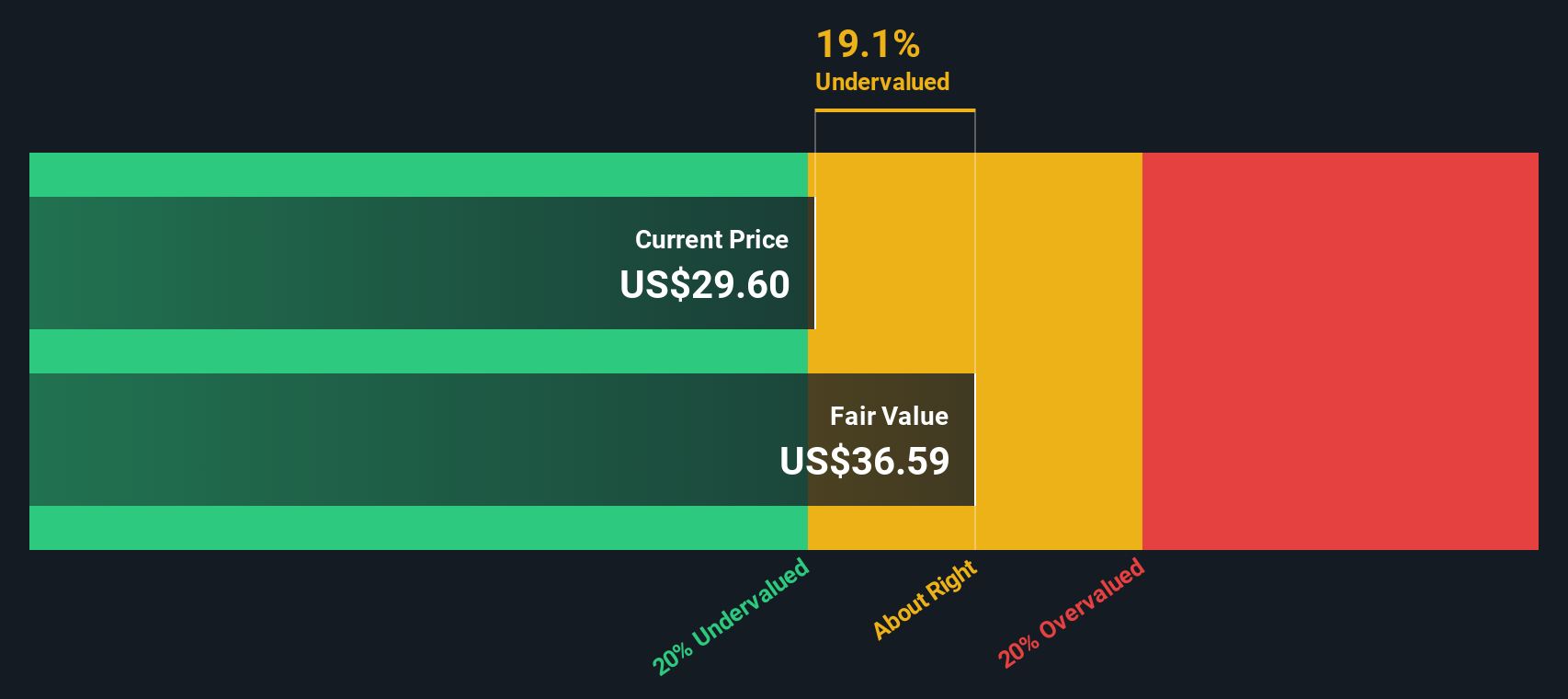

With shares rebounding sharply after this series of contract news, the big question is whether Firefly Aerospace offers an undervalued entry point, or if the market is already pricing in the company’s future lunar success.

Price-to-Book of -8.5x: Is it justified?

Assessing Firefly Aerospace’s valuation against its industry, the company reports a negative Price-to-Book (P/B) ratio of -8.5x. This stands in sharp contrast to the average P/B ratio of 3.3x for the US Aerospace & Defense sector. This suggests the company’s shares are valued significantly below its book value.

The Price-to-Book ratio measures market price relative to the company’s net assets. For asset-heavy sectors like aerospace, this metric is commonly used to gauge whether a stock is trading at a discount or premium to its underlying value.

However, Firefly’s negative equity, driven by ongoing losses and liabilities, complicates this interpretation. The sharp negative ratio signals that investors may be pricing in future growth potential over current fundamentals, or remaining cautious due to the company’s unprofitability and balance sheet risk.

Result: Fair Value of $37.89 (OVERVALUED)

See our latest analysis for Firefly Aerospace.However, mounting net losses and volatile returns remain key risks that could challenge Firefly Aerospace’s growth narrative in the near term.

Find out about the key risks to this Firefly Aerospace narrative.Another View: What Does Our DCF Model Suggest?

Looking at Firefly Aerospace through our DCF model offers a different angle. This approach is different from the earlier market-based multiple and points to a result that also suggests overvaluation. Could the market be missing something, or are expectations for future growth too high?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Firefly Aerospace Narrative

If you have your own perspective or want to dive deeper, you can quickly build your own personalized view of Firefly Aerospace’s outlook. Do it your way

A great starting point for your Firefly Aerospace research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t just wait for the next headline. Make your portfolio stand out by seeking unique opportunities where big trends and value align using the Simply Wall Street Screener:

- Boost your income potential with companies consistently offering strong yields by checking out dividend stocks with yields > 3% before these payers gain wider attention.

- Tap into tomorrow’s innovators by scouting AI penny stocks. These companies are shaping the future in artificial intelligence, automation, and advanced data solutions.

- Position yourself for value with lesser-known gems through undervalued stocks based on cash flows and spot opportunities the market may have overlooked.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com