Beiersdorf (XTRA:BEI) Valuation: Assessing the Impact of New North American Leadership and Strategic Growth Initiatives

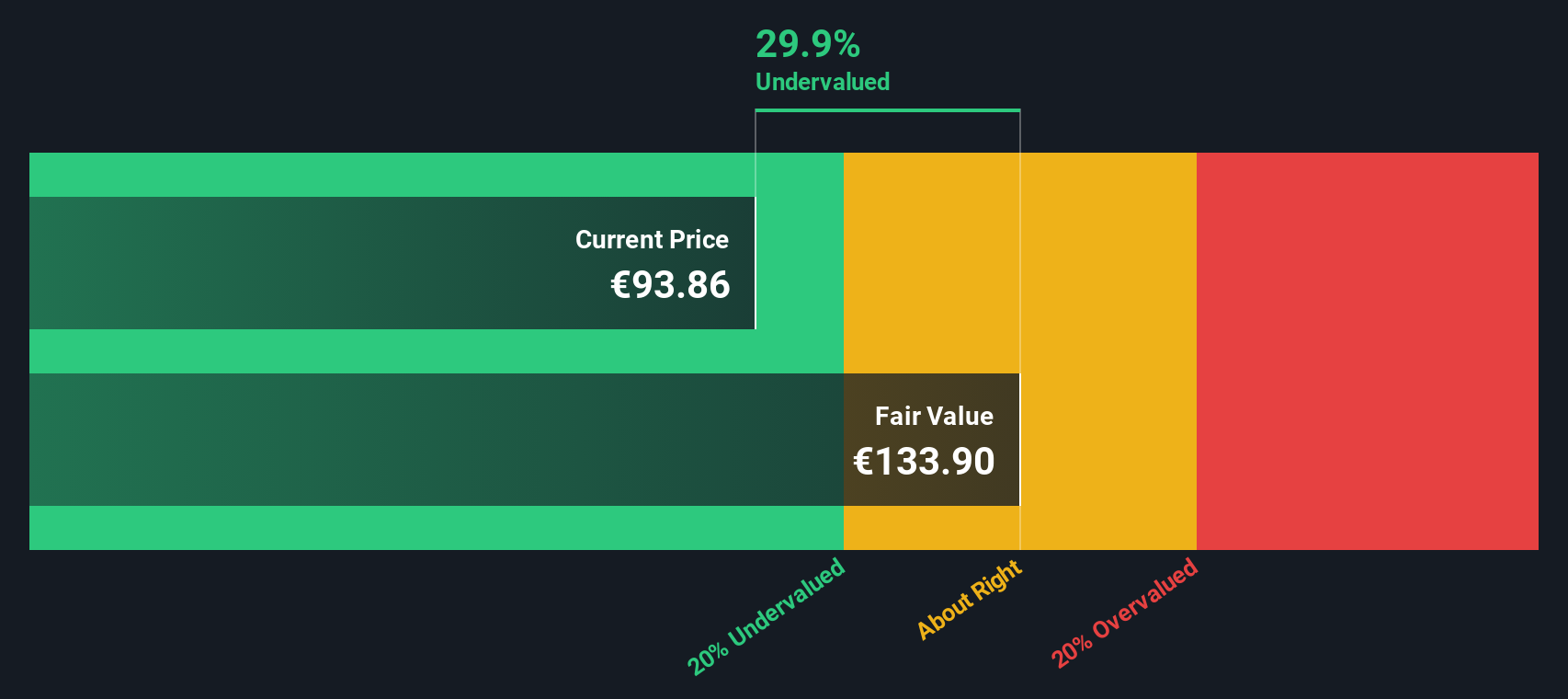

Most Popular Narrative: 27.8% Undervalued

The most widely followed valuation narrative suggests that Beiersdorf is trading considerably below its estimated fair value, implying strong upside potential from current levels.

Breakthrough innovation in science-based skincare, particularly the global rollout of the Epicelline anti-aging ingredient under both Eucerin and NIVEA, positions Beiersdorf to capture increased demand from an aging, health-conscious population. This is expected to drive higher-margin revenue growth from both premium and mass-market channels.

Curious why the market is overlooking this skin care powerhouse? Analysts are betting on a transformation fueled by ambitious growth targets, margin expansion, and a premium product pipeline unlike anything in Beiersdorf's history. What is the secret number at the center of this discounted valuation? The full narrative supports the call with bold projections and a few surprises.

Result: Fair Value of €123.21 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, risks remain, including intensifying competition in core markets and disappointing sales growth from NIVEA. These factors could challenge the upbeat valuation case.

Find out about the key risks to this Beiersdorf narrative.Another View: SWS DCF Model Perspective

Looking at Beiersdorf through the lens of our DCF model, the story appears consistent with earlier findings and again points to undervaluation. However, are both approaches missing risks, or is the case for value growing stronger?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Beiersdorf Narrative

If the consensus view does not align with your perspective, consider taking matters into your own hands. Explore the numbers yourself and build your view in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Beiersdorf.

Looking for More Investment Opportunities?

Smart investors keep their edge by going beyond the obvious. Don’t miss out on a fresh stream of potential winners. Use our tools to spot tomorrow’s leaders now.

- Uncover stocks delivering robust yields and sustainable income in today’s market with our dividend stocks with yields > 3%.

- Target innovative businesses making waves in artificial intelligence by scanning the market with our AI penny stocks.

- Pinpoint shares trading below their intrinsic value and position yourself for potential upside using our undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com