Does PDD’s Valuation Reflect Growth After Temu Resumes US Shipping in 2025?

Debating whether to hit buy, hold, or sell on PDD Holdings? You are definitely not alone. The stock has been a standout performer, climbing 32.7% year-to-date and delivering over 25% gains in the last twelve months. If you have been watching the company's growth, especially after Temu resumed shipping to the US and headlines about big ad spends and analyst price target hikes, it makes sense to wonder if now is the right time to get in or out of this name.

In just the past month, PDD has edged slightly higher, up 1.1%, but the long-term story is what really catches the eye. Over a three-year stretch, PDD shares have roared up an impressive 112%. Optimism is still building, too. Analyst after analyst has recently raised their price targets, with some aiming well past current levels. This sentiment suggests the market is beginning to view PDD as less risky, or at least as a company with more visible growth levers.

The big question, though, is not just about where the price has been, but whether it still offers value today. Based on our valuation checks, PDD scores a 5 out of 6, an unusually strong result that signals the company is undervalued across nearly every method we examined. Stick with me as I dig into how that score comes together, and why there may be an even more insightful way to assess PDD's true worth later in this article.

PDD Holdings delivered 25.7% returns over the last year. See how this stacks up to the rest of the Multiline Retail industry.Approach 1: PDD Holdings Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a fundamental valuation approach that estimates a company's true worth by projecting its future free cash flows and discounting them back to their present value. In this case, PDD Holdings' DCF uses the "2 Stage Free Cash Flow to Equity" method, leveraging both analyst estimates and longer-term growth assumptions.

PDD Holdings recently reported last twelve months Free Cash Flow (FCF) of CN¥93.25 billion. Analyst consensus expects FCF to climb even higher, with projections reaching CN¥162.04 billion by the end of 2027. Looking out a full decade, Simply Wall St extrapolates FCF could top CN¥287.88 billion by 2035, highlighting the company's strong growth trajectory.

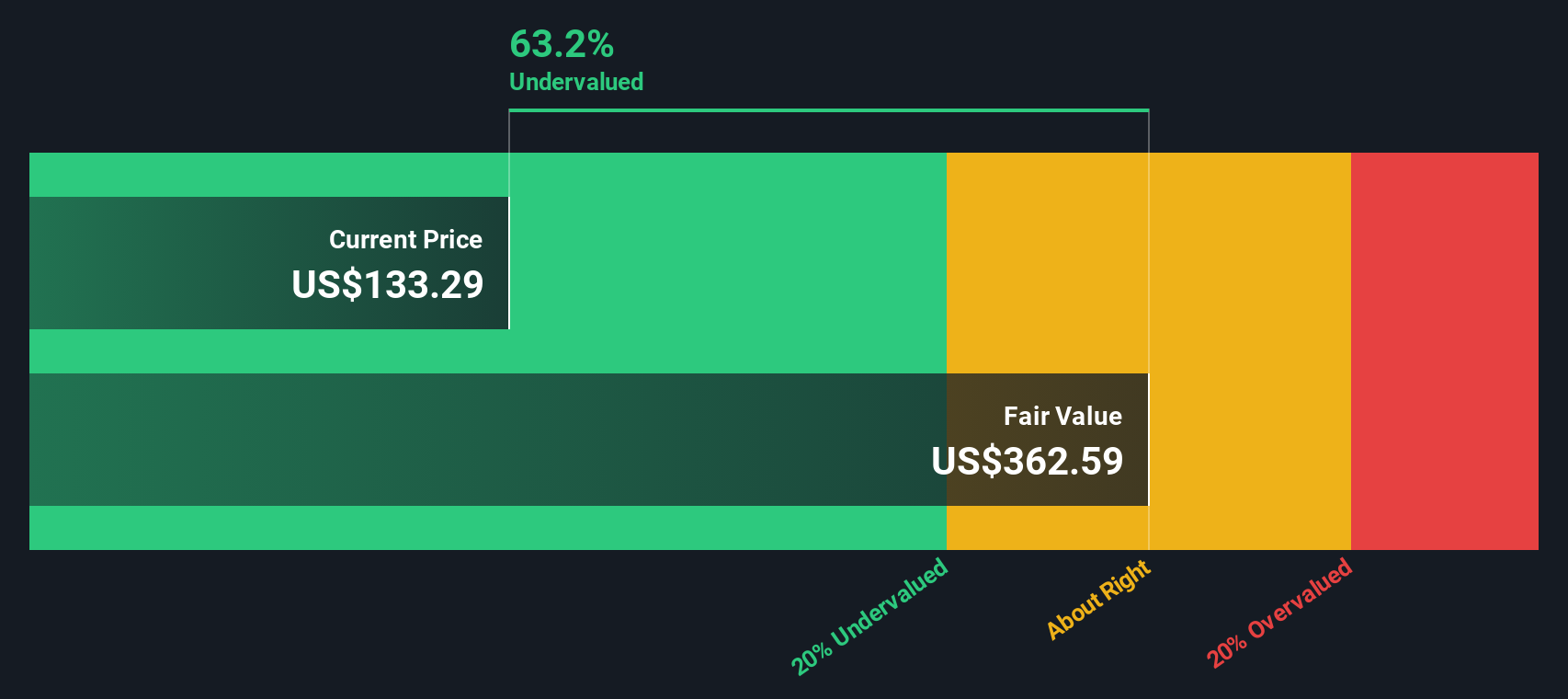

The result of these cash flow projections is an estimated intrinsic value of $355.18 per share. With PDD's shares currently trading at a substantial 63.8% discount to that fair value, this DCF analysis signals the stock is significantly undervalued right now.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for PDD Holdings.

Approach 2: PDD Holdings Price vs Earnings

The Price-to-Earnings (PE) ratio is a tried-and-true metric for evaluating profitable companies like PDD Holdings. It measures how much investors are willing to pay for each dollar of earnings and is especially meaningful when a company is posting solid profits, as is the case with PDD.

Of course, not all PE ratios are created equal. Higher growth prospects or lower risk typically command higher PE multiples, reflecting investor willingness to pay more for future earnings potential. On the other hand, elevated risks, stagnant growth, or other red flags can rightfully drag a PE lower.

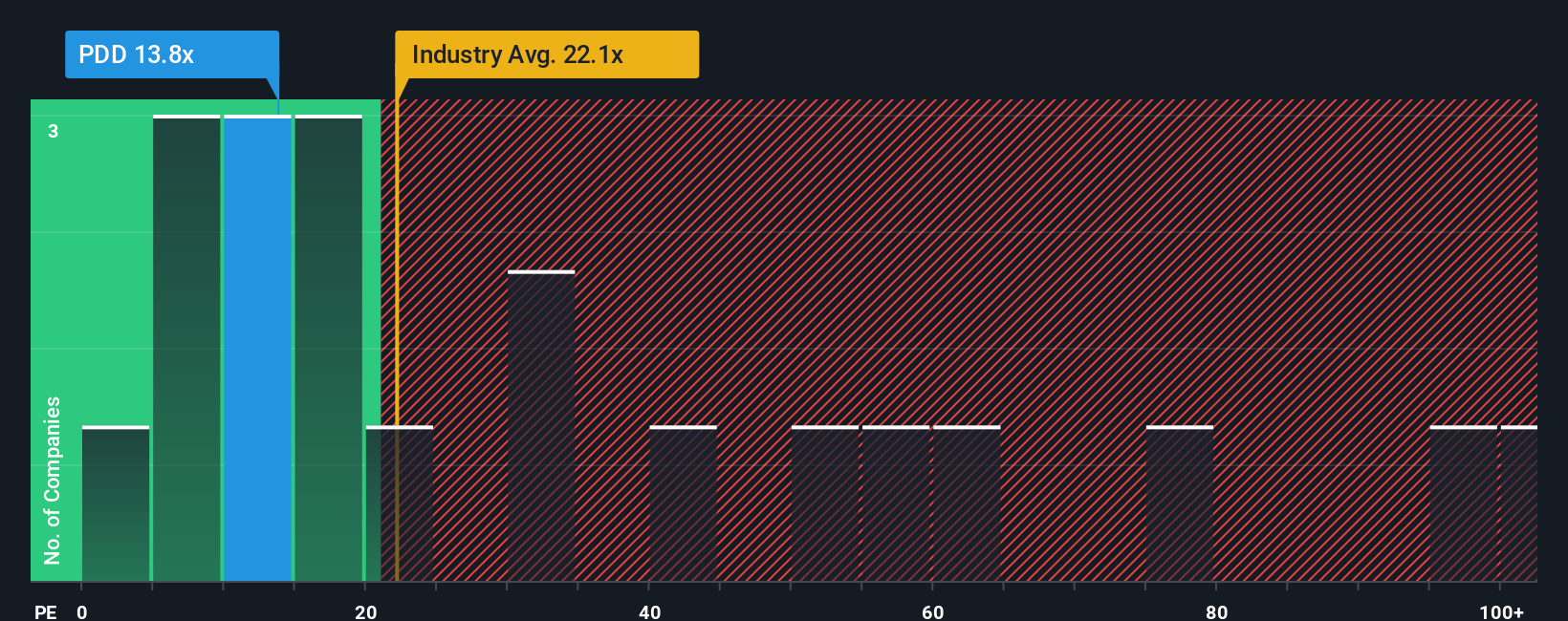

PDD Holdings currently trades at a PE ratio of 13.3x. For context, the average PE for the Multiline Retail industry sits at 22.5x, and the peer group commands an even loftier average of 83.8x. This means PDD is valued much lower than both its industry and direct competitors, which is certainly eye-catching at first glance.

However, raw comparisons have their limitations. Simply Wall St's proprietary Fair Ratio looks deeper and estimates what PE multiple PDD deserves by factoring in its growth, profit margins, risk profile, market cap, and industry characteristics. This makes it a much more tailored benchmark than broad industry or peer averages.

PDD's Fair Ratio is calculated at 29.3x. Compared to the actual PE of 13.3x, this suggests the stock is trading well below what would be reasonable given its fundamentals and outlook.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your PDD Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is your story about what a company will achieve, such as where you think revenue, profits, and margins are headed, and, most importantly, what you believe the business is really worth.

Unlike simple ratios or static models, Narratives connect the dots between your point of view, a financial forecast, and a fair value estimate. They let you base your investment decisions on facts and projections that reflect both the company's journey and your own outlook. This approach offers much more insight than a one-size-fits-all number.

Narratives are available to everyone through the Simply Wall St Community page, where millions of investors can easily share, compare, and update their stories for any stock. By setting your Narrative, you can quickly see if the current price is above or below your fair value. This helps you spot when to buy, hold, or sell based on your conviction, not just the consensus.

What makes Narratives even more powerful is their dynamic nature. They automatically update as new earnings, news, or market events come in, so your investing view stays timely. For instance, with PDD Holdings, some investors see the price surging towards $176 based on rapid international growth, while others take a more cautious stance with targets as low as $117 and warn of possible margin risks.

Do you think there's more to the story for PDD Holdings? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com