Does Powell Industries' (POWL) Strong Returns Justify High Short-Term Liabilities in Its Growth Strategy?

- Powell Industries recently reported a 34% return on capital employed, substantially above the electrical industry average, with capital employed nearly doubling over the past five years.

- An interesting aspect of this news is the company's high current liabilities, accounting for 41% of total assets, which could pose short-term financial risks despite strong reinvestment trends.

- To assess how these robust returns and liability levels might impact investor expectations, we will examine how the latest news shapes Powell Industries' investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Powell Industries Investment Narrative Recap

To be a Powell Industries shareholder, you need to believe in the company’s ability to harness robust internal reinvestment and sustained high returns on capital, while managing the business’s increased exposure to short-term liabilities. The recent report of a 34% ROCE and surging capital employed highlight reinvestment momentum, but the elevated level of current liabilities could magnify sensitivity to order and supply chain cycles. As a result, while short-term operating strength remains, the liability profile does temper some of the enthusiasm previously tied to backlog-driven visibility and secular electrification themes.

Of the recent announcements, the planned US$12.4 million expansion at the Jacintoport manufacturing facility stands out, directly tying to Powell’s reinvestment thesis. By boosting production capacity by 62%, this development supports the company’s pursuit of additional market share in key sectors and potentially underpins the strong ROCE shown in the latest report. As investors assess catalysts like these, it becomes even more important to weigh Powell’s ability to balance ambitious growth projects with the risk profile inherent in its current balance sheet structure.

Yet, while the operational results remain compelling, investors should keep in mind that high current liabilities mean the company could be more vulnerable if...

Read the full narrative on Powell Industries (it's free!)

Powell Industries is projected to reach $1.3 billion in revenue and $169.4 million in earnings by 2028. This outlook assumes annual revenue growth of 5.7% and a decrease in earnings of $6 million from the current $175.4 million.

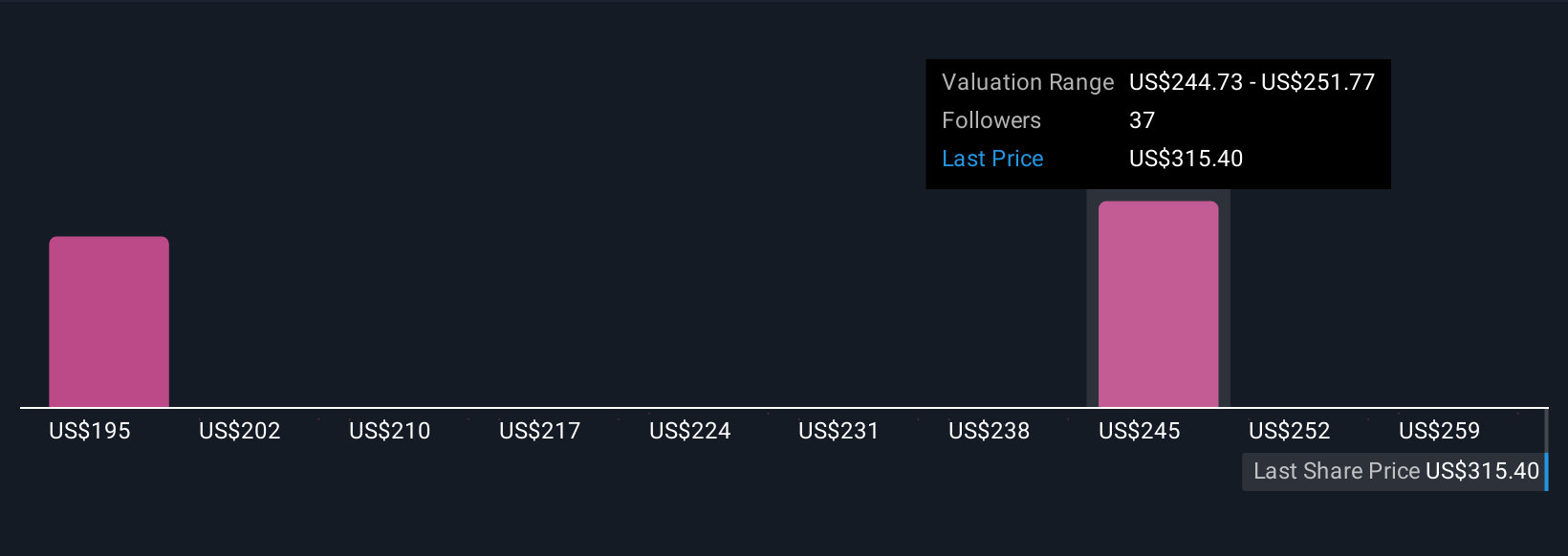

Uncover how Powell Industries' forecasts yield a $245.93 fair value, a 17% downside to its current price.

Exploring Other Perspectives

Five perspectives from the Simply Wall St Community put Powell Industries’ fair value estimates between US$143 and US$266 per share. Contrast this with the company’s recent ability to meaningfully outpace industry returns, which drives both opportunity and higher scrutiny around margin and backlog sustainability.

Explore 5 other fair value estimates on Powell Industries - why the stock might be worth less than half the current price!

Build Your Own Powell Industries Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Powell Industries research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Powell Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Powell Industries' overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com