The Bull Case for Flywire (FLYW) Could Change Following U.K. Student Payment Software Enhancements

- Earlier in September 2025, Flywire Corporation announced significant enhancements to its Student Financial Software solution for the U.K. higher education sector, including real-time integration with major ERP systems and streamlined U.S. loan disbursement capabilities.

- These upgrades have already resulted in improved student satisfaction and administrative efficiency at several institutions, highlighting Flywire's continuing investment in technology-driven solutions for complex education payment needs.

- We'll review how Flywire's new U.K. education offerings and real-time integrations may impact the company's long-term growth story.

Find companies with promising cash flow potential yet trading below their fair value.

Flywire Investment Narrative Recap

To own Flywire stock, investors need to believe in the company’s steady progress in digital payments and education software, especially its ability to expand internationally while countering headwinds from sector regulation and slowdowns in high-revenue regions. The recent enhancements to Flywire’s U.K. Student Financial Software, while positive for client satisfaction and efficiency, are not likely to materially shift the immediate risk tied to permit and visa policy changes, which remain the leading challenge impacting revenue predictability and short-term market sentiment.

Among Flywire’s recent announcements, the integration of real-time account presentment and payment capabilities with major U.K. higher education ERPs stands out. This move directly addresses administrative pain points and can help bolster Flywire’s reputation and stickiness in a critical global market, supporting the longer-term catalyst of digital payments adoption and international client growth.

But even as product innovation shines, the ongoing impact of global visa restrictions and regulatory changes is something every investor should keep in mind as...

Read the full narrative on Flywire (it's free!)

Flywire's outlook anticipates $817.0 million in revenue and $102.1 million in earnings by 2028. This is based on analysts forecasting 14.8% annual revenue growth and an earnings increase of $95.3 million from current earnings of $6.8 million.

Uncover how Flywire's forecasts yield a $14.55 fair value, a 11% upside to its current price.

Exploring Other Perspectives

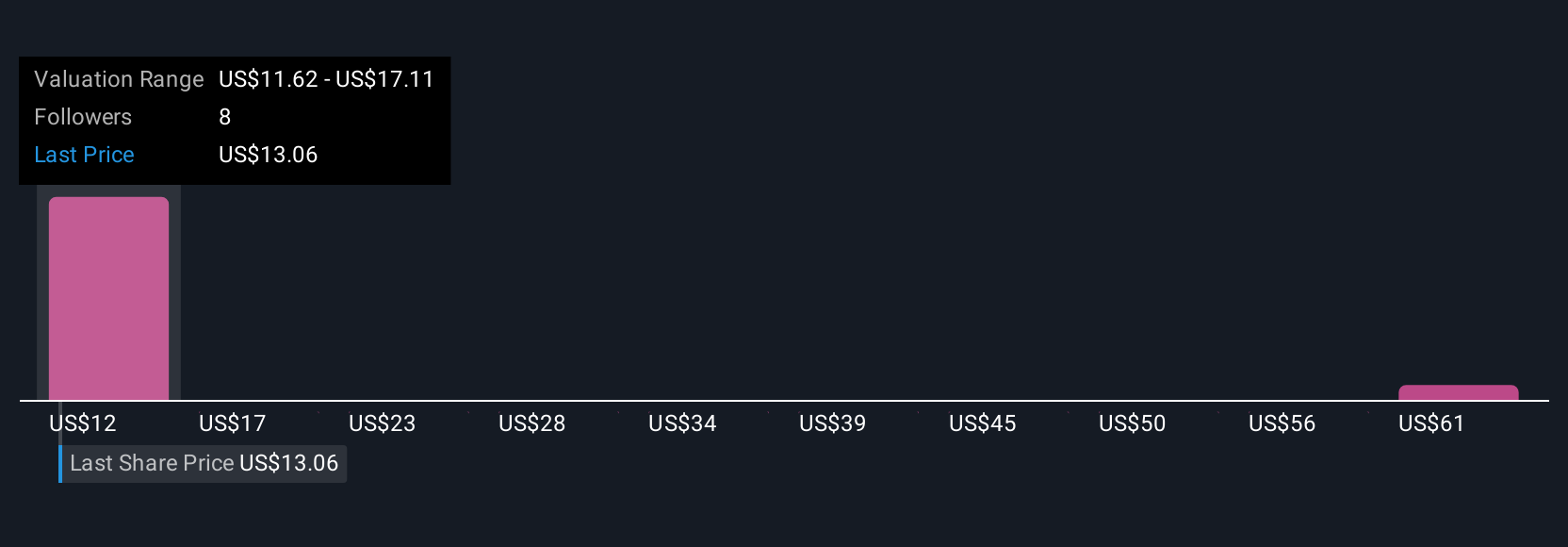

Simply Wall St Community members submitted three fair value estimates for Flywire, ranging from US$11.62 to US$66.49 per share. While projections vary greatly, many still point to regulatory or policy-related headwinds as a significant consideration for future growth and earnings stability.

Explore 3 other fair value estimates on Flywire - why the stock might be worth 11% less than the current price!

Build Your Own Flywire Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Flywire research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Flywire research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flywire's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com