A Fresh Look at Trinity Capital (TRIN) Valuation Following $100M Angel Studios Investment Announcement

If you have been following Trinity Capital (TRIN), the recent news probably turned your head. The company has announced a hefty $100 million commitment to Angel Studios, a media and technology business that just went public via a merger with Southport Acquisition Corporation. This deal stands out because Trinity Capital is stepping directly into the fast-evolving entertainment sector. The company appears confident that Angel’s crowd-driven content platform, which relies on its vast network of contributors to guide new projects, has more room to grow. Strategic investments like this are relatively rare and can signal where the company sees real upside, or at least a differentiated way to deploy capital.

Looking at what this means in the bigger picture, TRIN’s stock has already seen strong momentum, with a 34% return over the past year and an 86% gain over three years. Recent weeks brought incremental gains, further supported by consistently paying out dividends for 23 quarters without a cut. This streak of performance and reliable income may be why investors are watching closely to see how the Angel Studios investment will play out, especially as TRIN continues to seek new growth avenues beyond its traditional lending activities.

So, after this period of notable returns and a bold move into a new sector, investors may be considering whether Trinity Capital is offering a genuine buying opportunity or if the recent growth has already been reflected in the current price.

Most Popular Narrative: Fairly Valued

The prevailing narrative sees Trinity Capital as fairly valued, with analysts almost evenly split on where its price should land given future growth.

"Strong growth in venture debt deal flow, surging assets under management (AUM), and expansion into managed account platforms are fueling investor expectations for sustained double-digit revenue and earnings growth. The rapid pace of origination, however, raises the risk that future credit quality or loan demand could falter if the innovation/startup or venture capital ecosystem weakens unexpectedly."

Curious what’s fueling this delicate balance? The heart of the narrative is a bold bet on a unique growth runway backed by expanding assets and new income streams. But it all hinges on several surprising projections, numbers that show how much faith analysts place in future earnings, margins, and deal flow. Want the real story driving this fair value call? The next section reveals the specific benchmarks behind these calculations.

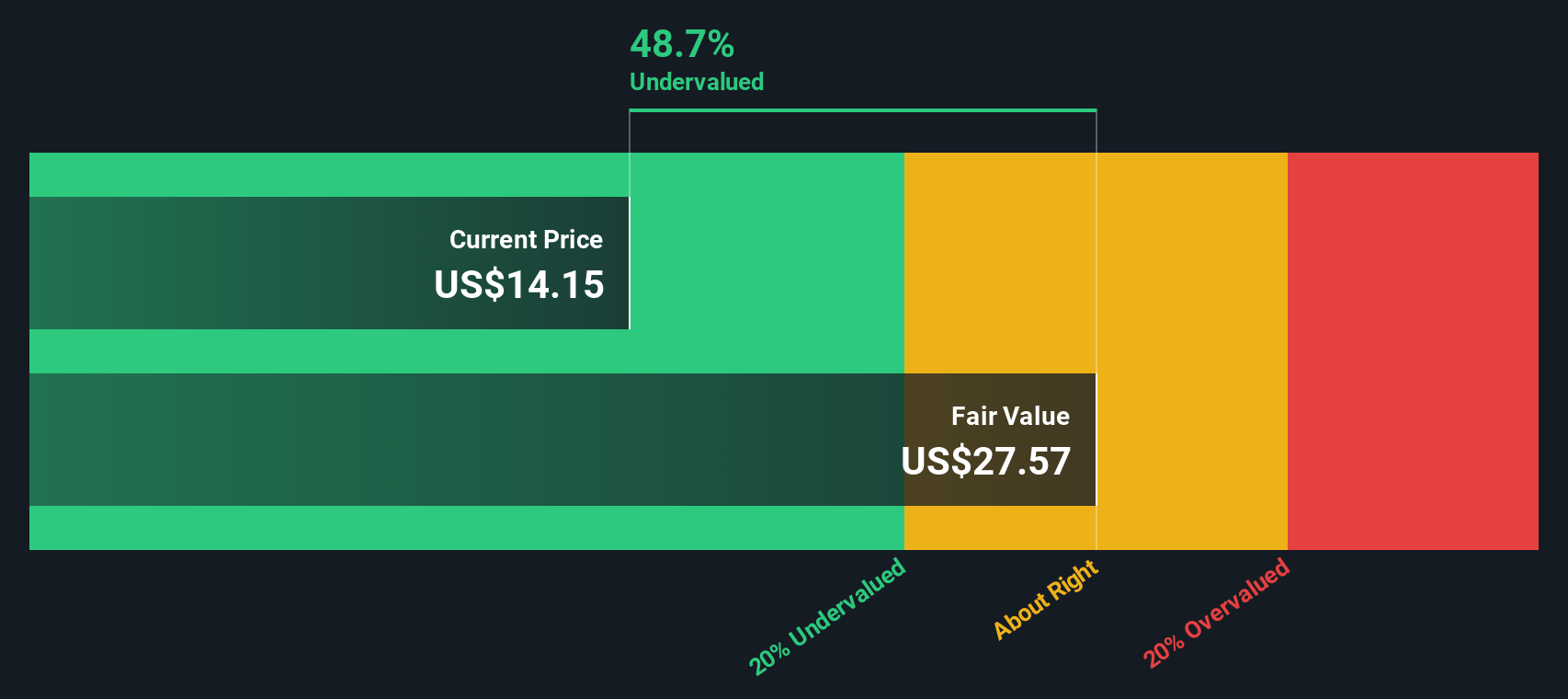

Result: Fair Value of $16.44 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent competition or a sudden downturn in tech and VC funding could quickly challenge these well-laid assumptions for Trinity Capital.

Find out about the key risks to this Trinity Capital narrative.Another View: Discounted Cash Flow Model

Taking a different angle, the SWS DCF model suggests Trinity Capital may actually be trading well below its intrinsic value. This model forecasts future cash flows and discounts them back to the present, offering an alternative perspective. Which lens should investors trust?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Trinity Capital Narrative

If you think there’s another angle or want to dig into the numbers yourself, you can craft your own case for Trinity Capital in just a few minutes. Do it your way.

A great starting point for your Trinity Capital research is our analysis highlighting 4 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Uncover your next winning opportunity and level up your strategy with tailored stock ideas built for multiple goals. Don’t let fresh trends and untapped potential pass you by.

- Tap into high-yield income streams by searching for established companies with consistent payouts through dividend stocks with yields > 3%.

- Spot undervalued gems positioned for a comeback by using our exclusive insights at undervalued stocks based on cash flows.

- Ride the artificial intelligence wave and get ahead of disruptive innovation by browsing today’s standout leaders with AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com