Upwork (UPWK) Valuation in Focus After $100 Million Share Buyback Announcement

Upwork (UPWK) just caught the market’s eye after announcing a fresh share repurchase program, approving the buyback of up to $100 million worth of company shares. A buyback of this scale tends to send a clear message that the management believes there is underlying value in its own stock and is willing to back it up in a significant way. For investors trying to figure out their next move, the timing and size of this authorization could be worth a closer look.

Buybacks like this often fuel price momentum, and Upwork’s share performance lately shows there is plenty of movement. The stock is up 64% over the past year, including a 24% gain in the past month, suggesting that optimism is building. This uptick comes as the company posts steady revenue growth, even as net income growth has pulled back, and follows other strategic updates over the last few quarters.

After a year of strong gains and this new buyback in play, is there still value left on the table for new investors, or is the recent climb already factoring in all of Upwork’s future growth?

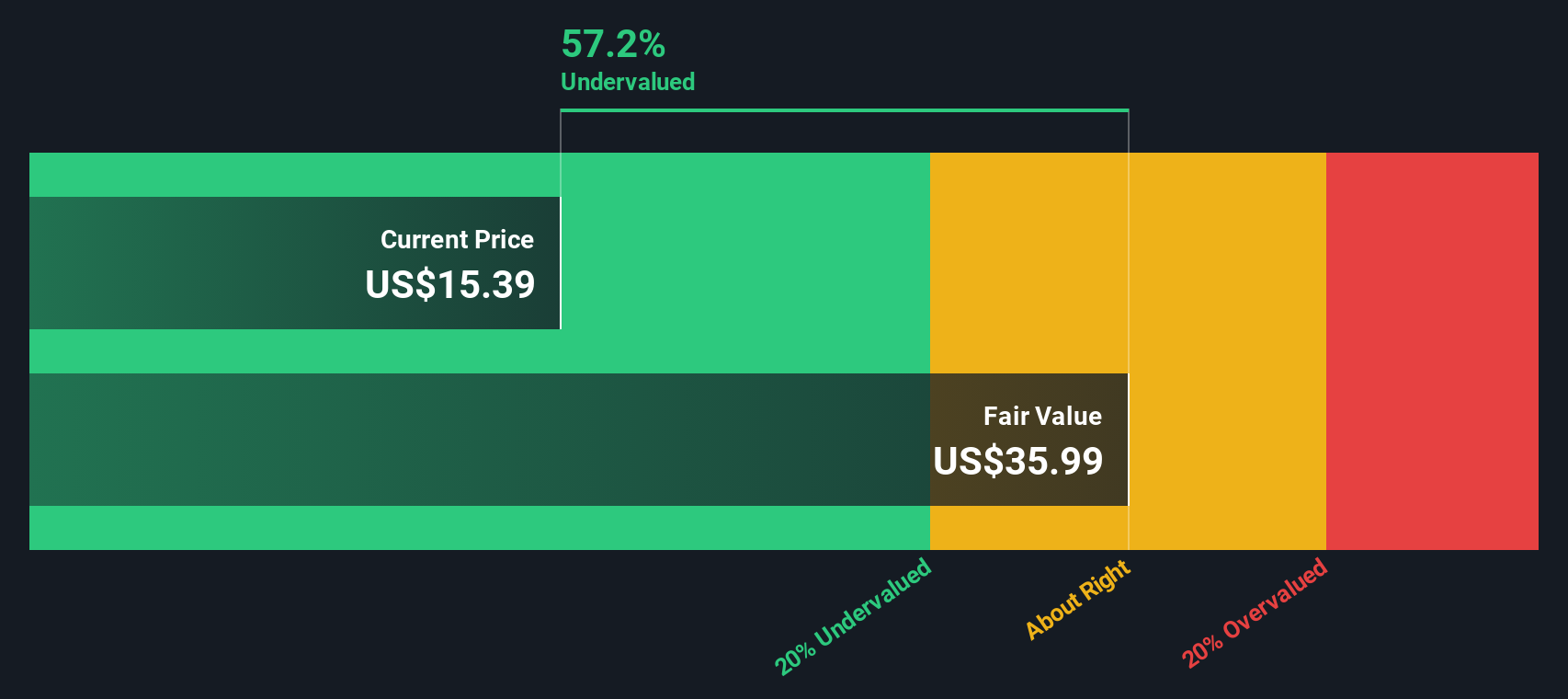

Most Popular Narrative: 8.6% Undervalued

According to the most widely followed narrative, Upwork is believed to be undervalued by 8.6% compared to its estimated fair value. The narrative builds this outlook on a set of forward-looking assumptions around revenue and earnings, with a discount rate applied to reflect market risk and opportunity.

Upwork's launch of integrated enterprise solutions through recent acquisitions (Bubty and Ascen) positions the company to capture a larger share of the $650 billion contingent workforce market, with expectations for meaningful GSV, revenue, and adjusted EBITDA contributions beginning in late 2026 and accelerating into 2027. This supports long-term earnings expansion.

What’s fueling the bullish analyst target? It’s not just about recent performance. There is a not-so-obvious growth lever powering this valuation. This lever only becomes clear when you look under the hood of their future projections. The answer? You will want to see how this valuation stacks up against the bold, market-shifting assumptions behind the headline number.

Result: Fair Value of $18.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, challenges such as sluggish client acquisition and unpredictable enterprise spending patterns could create headwinds, which may potentially weaken the current bullish narrative around Upwork's future growth.

Find out about the key risks to this Upwork narrative.Another View: What Does Our DCF Model Say?

While the analyst consensus points to undervaluation, our DCF model also finds the current share price sits well below its fair value. Could the market be missing something deeper? Alternatively, are key risks being overlooked?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Upwork Narrative

If you see things differently or prefer to dig into the details yourself, you can craft your own narrative in just a few minutes. Do it your way.

A great starting point for your Upwork research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Opportunities?

Expand your investing toolkit by tapping into game-changing trends. Don’t limit yourself to just one story when so many standout ideas are ready for you to act on today.

- Spot potential in rising digital currencies by tapping into companies building the future of blockchain through cryptocurrency and blockchain stocks.

- Uncover value-packed, under-the-radar stocks priced below their potential. Start finding better opportunities with undervalued stocks based on cash flows.

- Get ahead of the curve by tracking innovators in quantum computing advancing breakthroughs in speed, security, and real-world impact via quantum computing stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com