Is Snap Stock Set for a Comeback After Recent Digital Ad Market Rally?

If you have been eyeing Snap’s stock and wondering whether it finally deserves a spot in your portfolio, you are not alone. The ride has not been for the faint-hearted. After peaking a few years back, Snap’s price treaded downward, with a staggering 69.3% drop over five years and a 34.7% dip year-to-date. Even its one-year return sits at -23.9%, a reminder that long-term buy-and-hold investors have faced tough sledding.

However, the story gets more interesting when you look at the recent moves. Over the last month, Snap shares clawed back some ground, rising 2.7%, while a steady 1.7% gain took hold in just the last week. This small rebound has come as some investors digest broader market shifts, like renewed interest in digital advertising platforms, and as sentiment wavers between risk aversion and the potential for a turnaround in tech-adjacent names. No wonder you might be asking yourself if the current price really reflects what Snap is worth.

To help make sense of it all, we’ll zero in on Snap’s valuation. Out of six key valuation checks, Snap is currently undervalued on four, giving the company a value score of 4. But, as with any headline figure, context is everything. So before you jump to a verdict, let’s unpack the most common ways Snap’s valuation is measured and see how each stacks up. And stick around, because before we wrap, we’ll reveal a smarter way to cut through the noise and size up Snap’s true value.

Why Snap is lagging behind its peersApproach 1: Snap Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and discounting them back to today’s value. It is a standard tool for evaluating whether a stock is over or undervalued based on fundamentals, rather than market sentiment.

For Snap, the model starts with its latest twelve months Free Cash Flow, which stands at $365 million. Analysts project this number to rise significantly, with estimates for 2029 reaching $1.43 billion. While forecasts are only available through 2029, further growth is extrapolated for later years using conservative assumptions. These projections capture how well Snap could expand its cash generation if market trends and company execution remain steady.

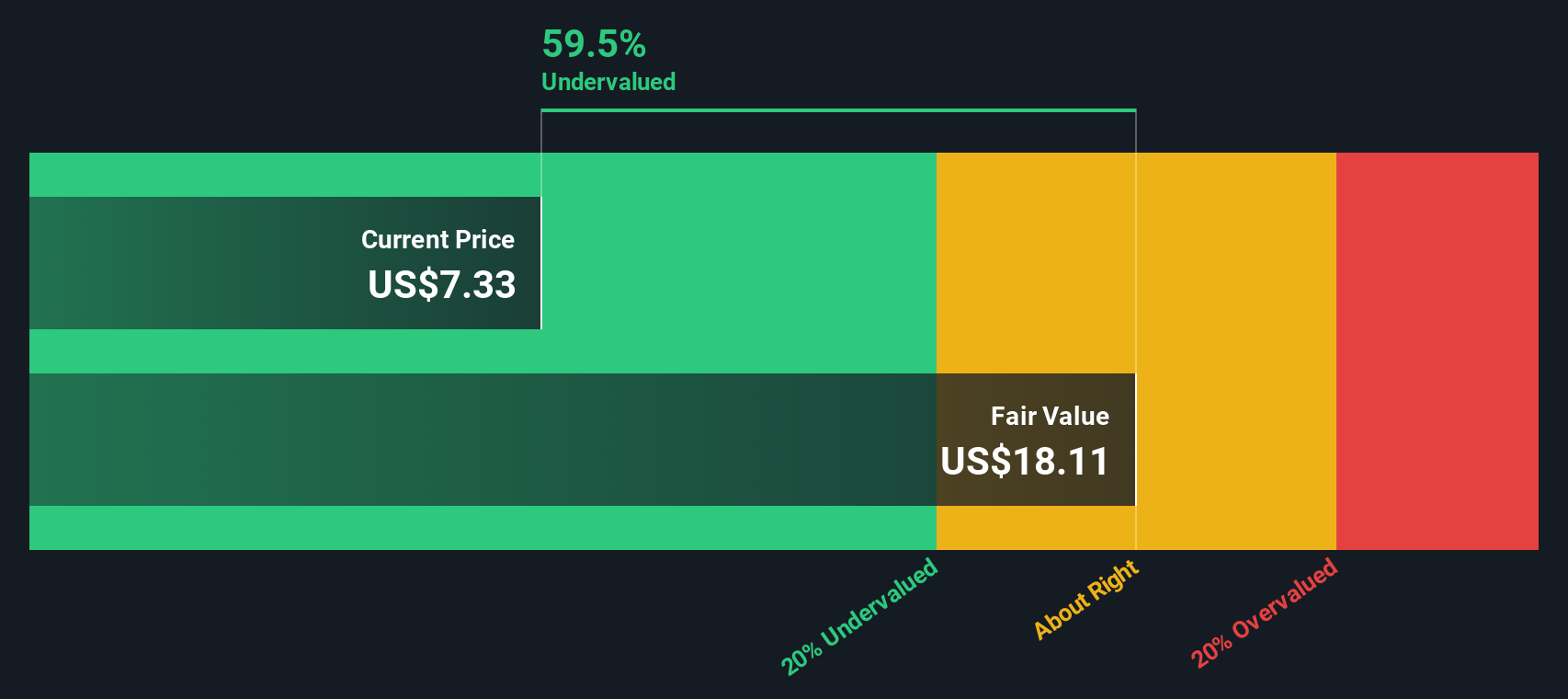

Based on this analysis, the DCF model pegs Snap’s intrinsic value at $18.46 per share. Compared to the current market price, this figure implies the stock is trading at a 60.2% discount. This suggests deep undervaluation.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Snap.

Approach 2: Snap Price vs Sales (P/S)

The Price-to-Sales (P/S) ratio is a favored valuation tool for companies like Snap, especially in periods when earnings are either negative or volatile. For growth-oriented tech firms still scaling up, the P/S ratio provides a useful way to benchmark valuation relative to revenue, which is a more stable metric that is less affected by short-term profitability swings.

Growth expectations and risk profile play a critical role in what counts as a “normal” or “fair” P/S ratio. Fast-growing companies typically command higher multiples, while those facing headwinds or greater uncertainty warrant a discount. It is important not just to compare Snap’s P/S ratio with industry or peer benchmarks, but also to weigh it against the company’s unique growth prospects and risks.

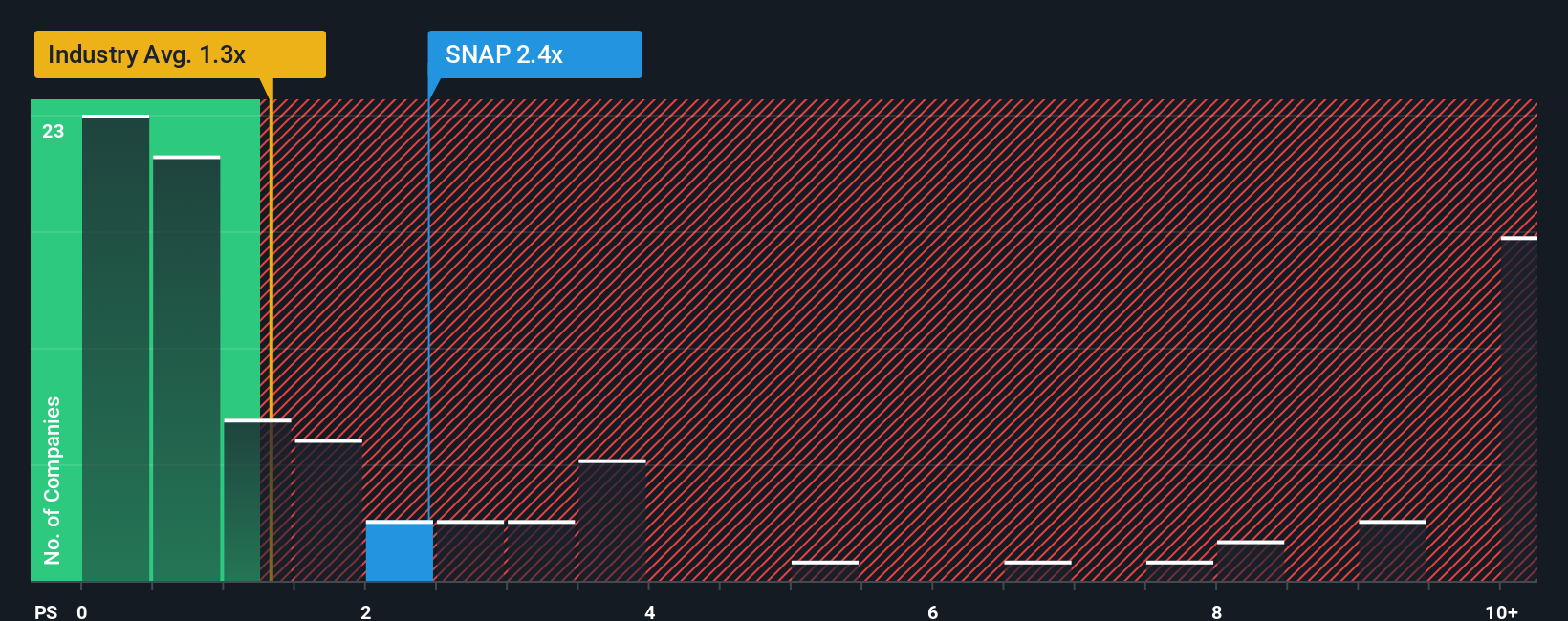

Currently, Snap trades at a P/S ratio of 2.2x. This is comfortably above the Interactive Media and Services industry average of 1.3x, and below the broader peer group average of 3.6x. To take things a step further, Simply Wall St’s proprietary Fair Ratio model weighs factors such as Snap’s earnings potential, profit margin, market size, and risk. For Snap, the Fair Ratio is 2.6x, offering a more holistic benchmark than a basic comparison to industry averages or competitors. With the actual P/S ratio just 0.4x below the Fair Ratio, Snap appears reasonably priced based on this metric, and is neither significantly undervalued nor overstretched.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your Snap Narrative

Earlier, we mentioned there is an even better way to understand valuation. Let us introduce Narratives, a simple and powerful approach that lets you connect your personal view of Snap’s future with clear, data-driven numbers.

With Narratives, you create a story or thesis about Snap, describing your beliefs about its business model, future revenue, earnings, and profit margins. This then produces an estimate of fair value unique to your perspective. This bridges the company’s story to actual financial forecasts and empowers you to make investment decisions that truly reflect your outlook, not just headlines or consensus guesses.

Narratives are accessible to everyone on Simply Wall St’s Community page, trusted by millions of investors, and are constantly updated with the latest news and results so your view always stays relevant.

They help you easily compare Fair Value to the current market price, so you can spot buying or selling opportunities based on your convictions and the latest company developments.

For example, while some Snap investors see opportunities in global digital ad expansion and AR innovation, supporting a bullish $16 valuation, others focus on regulatory risks and stagnant user growth, leading to a bearish $7 target. This shows how Narratives let you reflect your unique view in a tangible forecast.

Do you think there's more to the story for Snap? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com