How the Bretisilocin Acquisition Could Shift AbbVie’s 2025 Valuation Debate

Thinking about whether you should buy, hold, or cash out of AbbVie? You’re not alone. This stock has been anything but quiet lately, with its price closing at $218.34. Over just the last week, AbbVie jumped 4.1%, stacking on top of a solid 5.6% gain over the last month. Stretch that timeline out and AbbVie's numbers become even more impressive, with a 21.7% return year-to-date and nearly 200% over five years. These are the kinds of figures that tend to turn heads.

What’s driving this surge in investor confidence? It’s not just market optimism. Recent buzz centers around AbbVie’s push to expand its Neuro pipeline, particularly the proposed acquisition of Bretisilocin, a move praised as a “very solid addition” by analysts at Raymond James. Just a month prior, Bloomberg reported AbbVie was in talks to buy Gilgamesh Pharmaceuticals for around $1B, signaling the company’s active hunt for innovative assets to fuel future growth. Moves like these can recalibrate investors’ perceptions of risk and upside, driving both price and attention.

Of course, growth stories are one thing, but what about value? If you care about buying at the right price, AbbVie's current valuation score comes in at 2 out of 6, meaning it’s considered undervalued on two key checks. But numbers only tell part of the story. Let's break down what those valuation methods actually show and, more importantly, explore if there’s a smarter way to understand what AbbVie is really worth.

AbbVie scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.Approach 1: AbbVie Discounted Cash Flow (DCF) Analysis

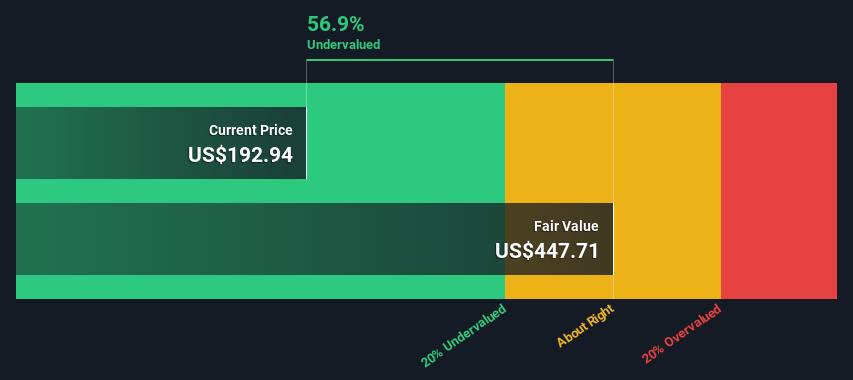

The Discounted Cash Flow (DCF) model estimates a company's true value by projecting its future free cash flows and discounting them back to their value today. Essentially, it provides an intrinsic value based on what the business is expected to generate, not just what the stock market thinks it should be worth right now.

For AbbVie, the DCF analysis starts with its current annual Free Cash Flow of $18.4 billion. This figure serves as a robust foundation by any standard. Analysts provide estimates for the next five years, with projected Free Cash Flow rising to $32.3 billion in 2029. Beyond that, Simply Wall St extrapolates cash flows out to 2035, reflecting a steady annual growth trajectory but with more uncertainty.

Based on these projections, the DCF calculation arrives at an intrinsic value of $443.68 per share. This represents a 50.8% discount relative to the current share price, indicating AbbVie stock is significantly undervalued according to this model.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for AbbVie.

Approach 2: AbbVie Price vs Earnings

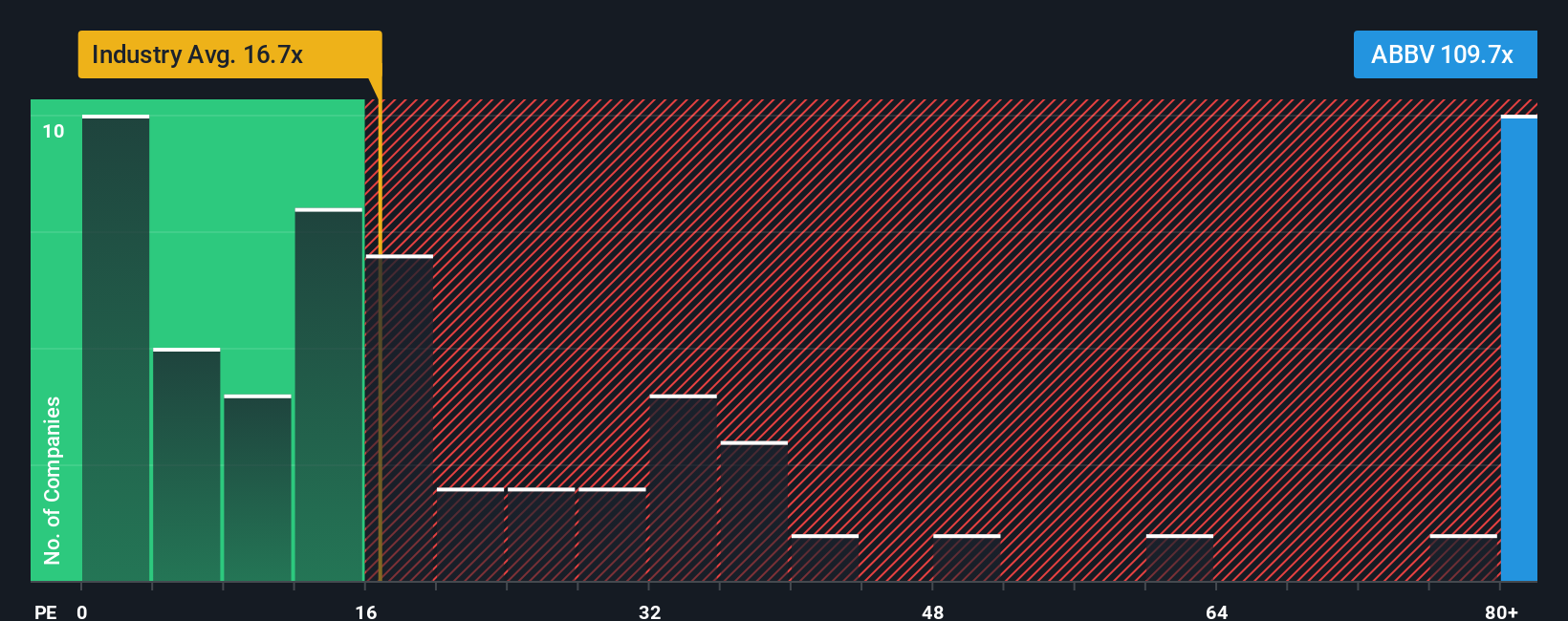

The price-to-earnings (PE) ratio is one of the most trusted metrics for valuing profitable companies like AbbVie. It connects a company’s current stock price to how much profit it actually generates. When a business is solidly in the black, the PE ratio provides a fast, relatable way to gauge if investors are paying a premium or a discount for those earnings.

What counts as a “normal” or “fair” PE ratio doesn't just depend on a company’s profits today. Investors also consider how quickly earnings are expected to grow and how risky that growth looks. Companies with higher expected growth or lower risk typically trade at higher PE multiples, while those with slower growth or greater uncertainty tend to be valued at lower multiples.

Currently, AbbVie is trading at a hefty 103.60x earnings. Stack that up next to the biotech industry average of 15.27x and the peer group’s average of 21.46x, and it is clear AbbVie’s PE sits near the very top of its sector. However, Simply Wall St’s proprietary “Fair Ratio” adjusts for the company’s expected earnings growth, its profit margins, broader biotech risks, and even factors like market cap. For AbbVie, this fair value lands at 40.13x, well below its current level. Unlike a standard industry or peer comparison, the Fair Ratio reveals whether the higher PE is justified by AbbVie’s specific strengths and outlook, or if investors may be overreaching.

Comparing AbbVie’s actual PE of 103.60x with its Fair Ratio of 40.13x suggests the stock is trading at a significant premium, even after accounting for its growth prospects and unique strengths.

Result: OVERVALUED

Upgrade Your Decision Making: Choose your AbbVie Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives, a powerful tool that lets you connect your perspective on a company with the numbers behind its fair value. A Narrative is your story: it’s where you outline what you think AbbVie’s future holds, set your own expectations for revenue growth, earnings, margins, and then see how these assumptions translate into a fair value estimate. Narratives link your insights or concerns directly to a financial forecast, giving you clarity on whether you see AbbVie as undervalued or overvalued at the current price.

On Simply Wall St’s Community page, which is used by millions, you can easily write or explore Narratives, making the process accessible even if you’re new to stock analysis. Narratives help you anchor your buy or sell decisions, since you can instantly compare your fair value calculation with the actual market price. What makes them especially powerful is that they update automatically as news, results, or forecasts change, ensuring your perspective stays current. For example, some users see AbbVie’s expanding neuroscience and immunology pipeline driving a fair value as high as $255 per share, while others worry about patent losses and price pressures, setting their fair value closer to $170. This highlights how Narratives let you weigh your conviction alongside the numbers.

Do you think there's more to the story for AbbVie? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com