What Does Weak Consumer Demand Mean for Budweiser Brewing Company APAC Shares in 2025?

Thinking about what to do with Budweiser Brewing Company APAC stock? You are not alone. Investors have watched this iconic brewer’s shares swing wildly over the past few years, and the latest market action has left plenty of folks scratching their heads. In the last week, the stock slipped 3.6 percent, and over the last 30 days, it is down 4.6 percent. But step back to the start of the year and you will find a 12.0 percent gain, while the move over the past year is a solid 8.7 percent up. Of course, the three- and five-year stories tell a different tale, with the stock down a staggering 60.0 percent and 61.5 percent respectively, signaling that there have been serious shifts in market perception and expectations.

Recent fluctuations have had more to do with sentiment around consumer staples in Asia and evolving competition in the beverage space, rather than specific company news. Some investors seem to be betting on recovery potential, hoping that previous overreactions have driven the share price down too far, too fast. This kind of volatility often signals opportunity for those paying close attention to value.

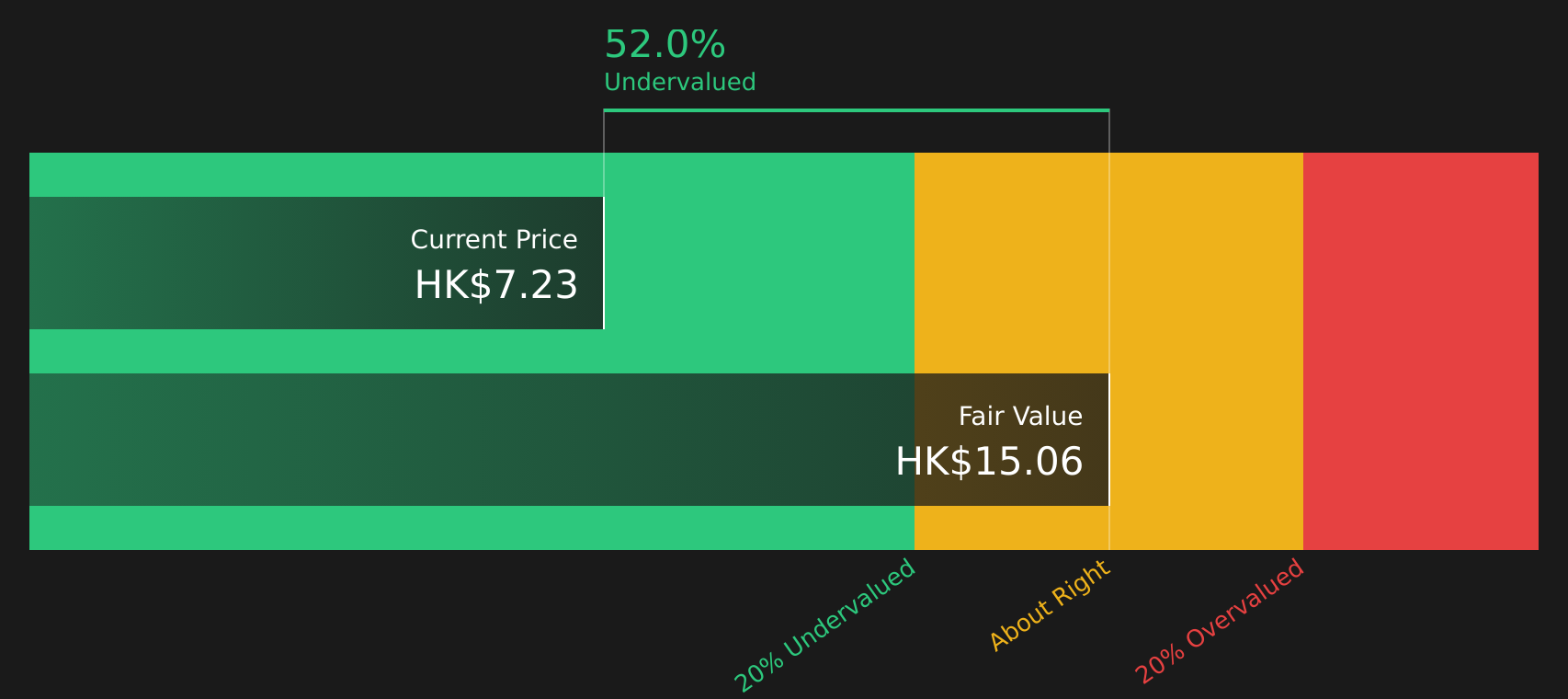

Speaking of value, Budweiser Brewing Company APAC currently receives a valuation score of 3. That means it is considered undervalued on 3 out of the 6 standard checks analysts use, a point worth exploring if you are looking for bargain buys with growth potential. In the next sections, we will break down how different valuation approaches paint the picture for Budweiser, then reveal a lesser-known but even more insightful way to judge if this iconic brewer is truly a buy right now.

Why Budweiser Brewing Company APAC is lagging behind its peersApproach 1: Budweiser Brewing Company APAC Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's true value by projecting its future cash flows and then discounting them back to the present using a rate that reflects risk and time. This approach provides investors with an intrinsic value, helping determine if the stock price is justified by anticipated performance.

For Budweiser Brewing Company APAC, the latest twelve months’ Free Cash Flow (FCF) stands at $784.8 Million. Analysts expect that this figure will continue to rise, projecting FCF to reach $1.098 Billion by 2027. Looking further forward using mixed analyst estimates and algorithmic extrapolations, Simply Wall St forecasts FCF to grow to approximately $1.42 Billion by 2035. These figures form the backbone of the valuation and offer a long-term view of Budweiser’s earnings potential.

Taking these forecasts into account, the DCF suggests an intrinsic value of $15.99 per share. Compared to the most recent share price, this implies the stock is trading at a discount of 49.3%. In other words, the market appears to be skeptical about the company’s future. If these cash flow projections hold, the stock could offer significant upside.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Budweiser Brewing Company APAC.

Approach 2: Budweiser Brewing Company APAC Price vs Earnings

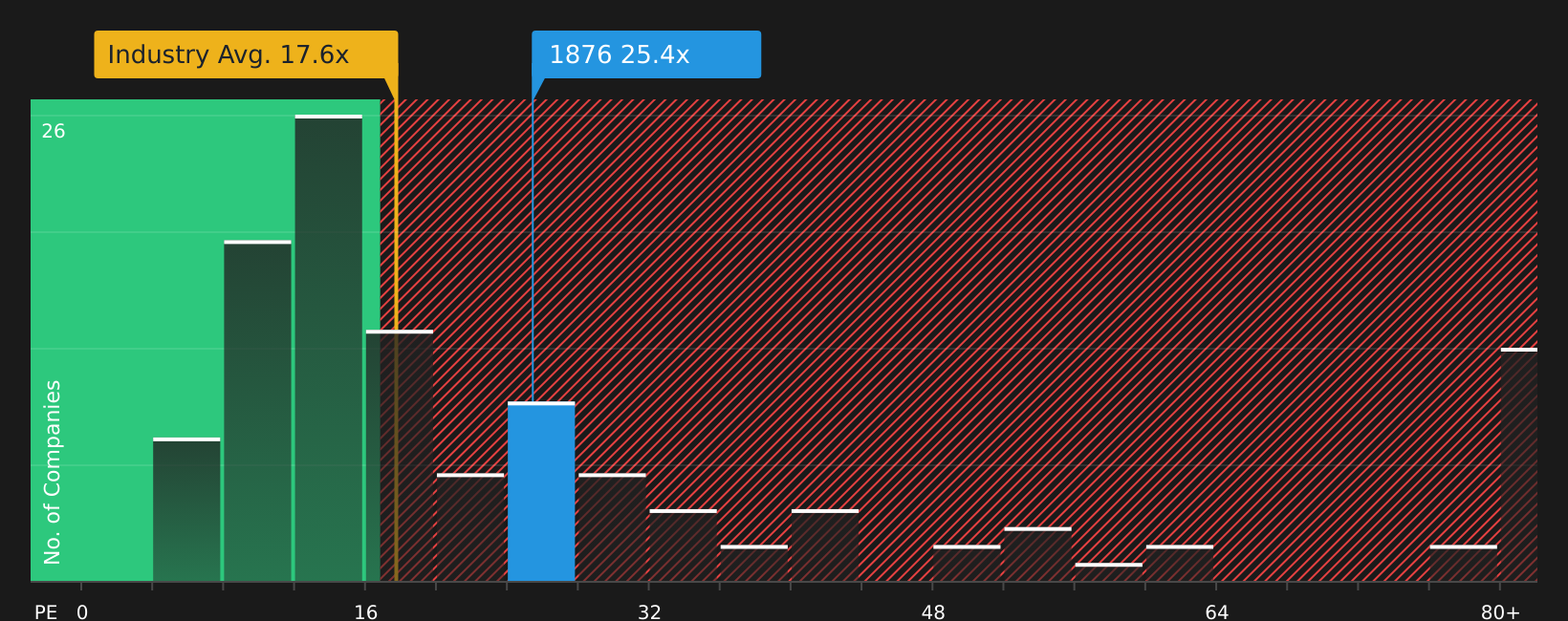

For profitable companies like Budweiser Brewing Company APAC, the Price-to-Earnings (PE) ratio is often a go-to valuation tool. This multiple gives investors a snapshot of how much they are paying for each dollar of current profits, making it especially useful for comparing companies with steady earnings.

The "right" PE ratio is influenced by a company’s expected growth and its risk level. Growing companies typically command a higher PE, while those facing headwinds or higher risks usually trade at lower multiples. It is also helpful to consider what investors are paying for comparable businesses in the same industry or market.

Brewery peers on average trade at 32.59x, while the industry as a whole averages about 18.23x. Budweiser Brewing Company APAC itself sits at 23.18x, higher than the industry but notably below direct peers. Simply Wall St’s “Fair Ratio,” a proprietary number that incorporates future growth forecasts, profit margins, risk profile, industry trends, and market cap, sits at 21.61x for Budweiser. This custom benchmark moves beyond raw averages, providing a tailored, data-backed expectation for what the market should be willing to pay.

Comparing the Fair Ratio of 21.61x to Budweiser’s actual PE of 23.18x suggests the shares are slightly overvalued on this metric, but the difference is not dramatic.

Result: OVERVALUED

Upgrade Your Decision Making: Choose your Budweiser Brewing Company APAC Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is essentially your story or your perspective about a company, connecting what you believe about its future to a set of forecasts for its revenue, earnings, and margins. This approach moves beyond just looking at numbers or ratios by allowing you to build, adjust, or choose a Narrative that reflects your unique outlook. Narratives link the company’s big-picture story directly to financial forecasts and, ultimately, to a fair value you can use as a reference point when deciding whether the current price is attractive or not.

On Simply Wall St’s Community page, millions of investors share and revise their Narratives, making it easy to browse, create, or update your own view in real time. Because Narratives update dynamically in response to new information, such as company news, earnings releases, or industry shifts, they help you stay confident and avoid outdated thinking when weighing buy or sell decisions. For example, some users see rapid premiumization and digital expansion lifting Budweiser Brewing Company APAC’s value as high as HK$14.92, while others remain cautious due to competitive and regulatory challenges, estimating fair value closer to HK$7.85. This range shows how Narratives empower you to anchor your decisions in both data and your personal read of the company’s story.

Do you think there's more to the story for Budweiser Brewing Company APAC? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com