D-Wave Quantum (QBTS): Evaluating Valuation After Breakthroughs and Leadership Moves Fuel Investor Interest

If you’ve been keeping tabs on D-Wave Quantum (NYSE:QBTS), you probably noticed the buzz ramping up following their showcase at SEMICON Taiwan. It wasn’t just another tech presentation. D-Wave highlighted breakthrough progress in annealing quantum computing and hybrid technologies, painting a vivid picture of what could be next for the quantum space. Alongside this, the company’s decision to bring in a veteran chief information security officer sends a clear signal that they’re building toward sustainable, secure growth.

All of this is happening against a backdrop of solid momentum for the stock. Over the past year, shares have climbed over 17%, aided by recent multi-day rallies and heightened investor interest. Recent events, like major partnerships, a growing customer list, and D-Wave landing a spot in prominent quantum computing ETFs, are fueling optimism. With these forces converging, speculation around future growth and risk is starting to shift, creating more conversations about what’s driving the stock.

After a year of high activity and fresh milestones, the question for investors now is simple: is D-Wave Quantum trading at a bargain, or has the market already priced in its next wave of breakthrough growth?

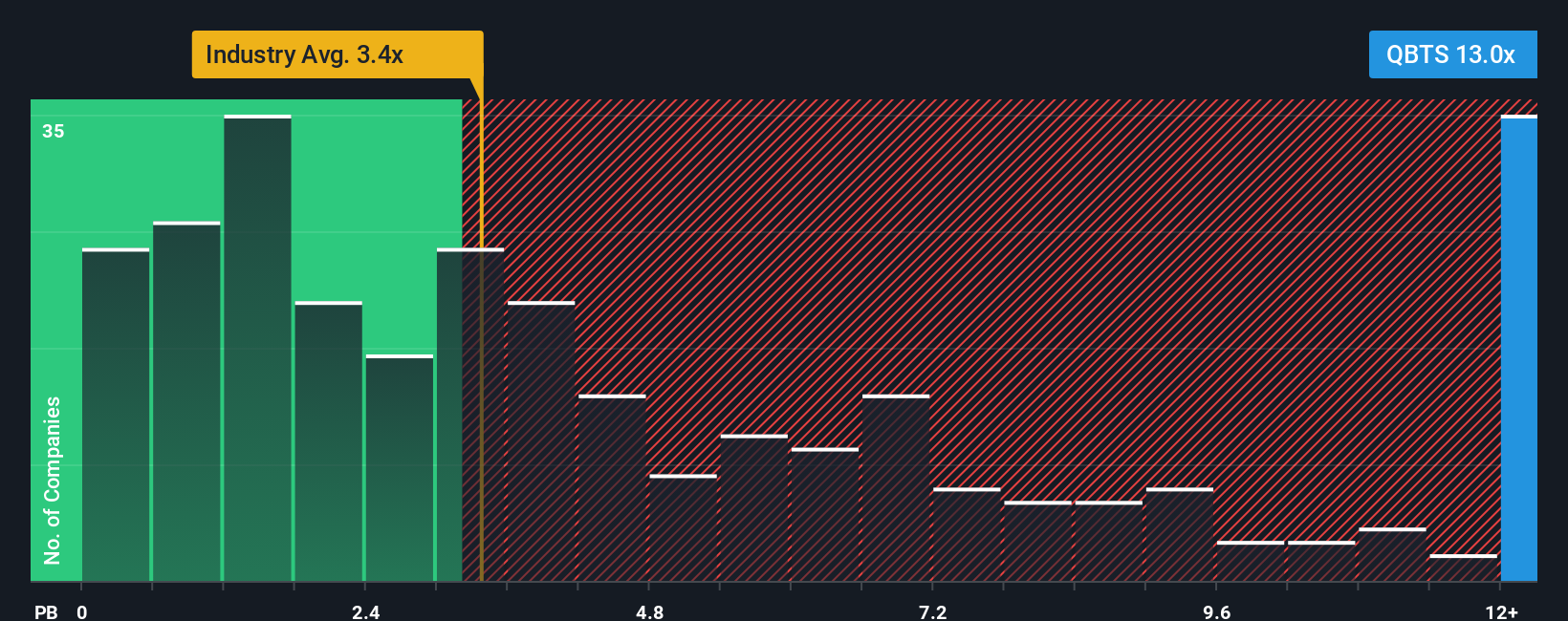

Price-to-Book of 8.7x: Is it justified?

Based on the price-to-book (P/B) ratio, D-Wave Quantum trades at 8.7 times its book value. This is lower than the peer average of 13.7x, but significantly higher than the broader US Software industry average of 3.8x. This indicates the stock might be attractively priced when compared to close peers, yet expensive relative to the wider sector.

The price-to-book ratio measures how much investors are willing to pay for each dollar of net assets. In rapidly evolving sectors like quantum computing, high P/B multiples can signal investor belief in the company’s future growth prospects or a premium for cutting-edge technology, even when current profitability is negative.

The key question becomes whether this premium is warranted given D-Wave’s trajectory. The company’s revenue is forecast to grow rapidly, but ongoing unprofitability and recent shareholder dilution raise debates about where fair value lies.

Result: Fair Value of $22.20 (UNDERVALUED)

See our latest analysis for D-Wave Quantum.However, ongoing losses and recent shareholder dilution could undermine future gains, particularly if revenue growth slows or if market optimism fades.

Find out about the key risks to this D-Wave Quantum narrative.Another View: Comparing to the Broader Industry

Taking a different angle, the industry’s average price-to-book is much lower than D-Wave Quantum’s. This suggests the stock might be more expensive than most in its sector. Could market optimism be overshooting the fundamentals?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own D-Wave Quantum Narrative

If you see things differently or want to dive deeper into the numbers yourself, building your own view of D-Wave Quantum takes just moments. Do it your way.

A great starting point for your D-Wave Quantum research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Stay ahead of the crowd by searching for new opportunities beyond D-Wave Quantum. The right screener could help unlock your next big winner, so do not let these trends pass you by.

- Uncover overlooked growth with penny stocks with strong financials. Here, under-the-radar companies with robust financials might offer outsized potential before the market catches on.

- Accelerate your portfolio by tapping into tomorrow’s breakthroughs with AI penny stocks. This screener features pioneers pushing the boundaries in artificial intelligence innovation.

- Power up your income strategy and find reliable opportunities for steadier returns with dividend stocks with yields > 3%, focusing on stocks yielding over 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com