Is Now the Right Time to Reassess Kintetsu Group After Recent 5% One-Month Rally?

Thinking about what to do with Kintetsu Group HoldingsLtd stock right now? Whatever side of the fence you are on, it is worth pausing to consider what the recent moves actually mean before you make your next decision. Despite a modest climb this week of 1.1% and a stronger 5.2% push over the last month, the stock’s performance year to date tells a tougher story, showing a loss of 6.7%. If you zoom out further, the pain gets a bit more obvious, with the stock down 9.0% over one year, and substantially more, down over 30% across three and five year horizons.

So what is happening beneath the surface? The company has been riding broader waves in Japan’s transport and leisure market, with the sector seeing shifts in both risk appetite and demand forecasts this year. While there have been no single, seismic news events, investors seem to be reassessing long-term prospects in the context of reopening trends, new government infrastructure plans, and ongoing optimization in the travel industry. There is a sense that some of the recent uptick reflects cautious optimism, but the longer-term narrative remains complicated.

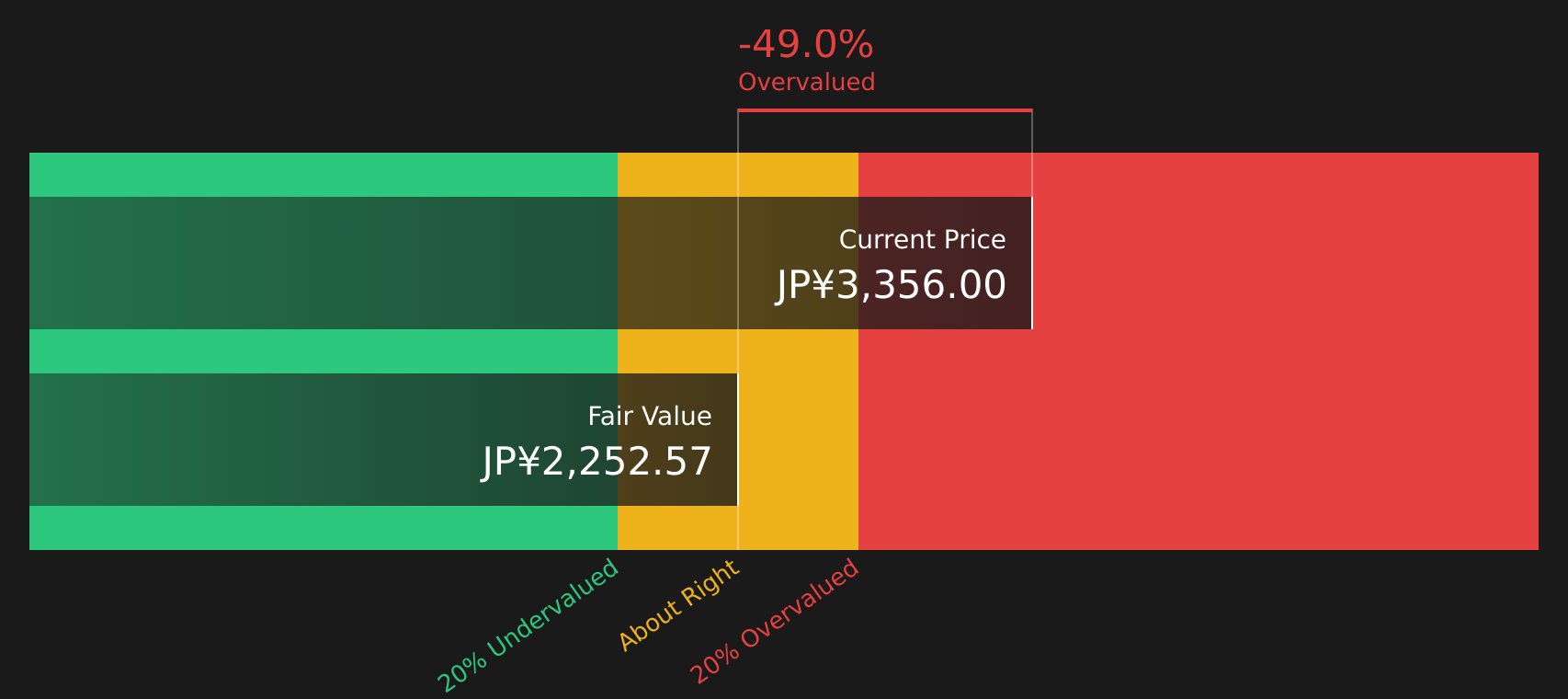

From a numbers-only perspective, Kintetsu Group HoldingsLtd currently carries a valuation score of 1 out of 6, so it ticks just one box for being undervalued according to key criteria. But how much can we trust those simple checklists? Let’s dive into how the main valuation methods stack up for this stock, and later, look at what might be an even more effective way to cut through the noise.

Kintetsu Group HoldingsLtd scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.Approach 1: Kintetsu Group HoldingsLtd Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and discounting them back to today’s value. For Kintetsu Group HoldingsLtd, this involves looking at how much free cash the company is expected to generate, both now and in the years ahead, then adjusting those numbers to reflect the time value of money.

Currently, the company reported last twelve months free cash flow of approximately ¥30.6 billion. Analyst forecasts predict a notable rebound, with free cash flow reaching about ¥44.96 billion by fiscal year 2028. These projections are key steps in the calculation, with longer-term annual estimates after 2028 extrapolated using industry-standard methods. All values are presented in Japanese yen, the reporting currency.

When applying the DCF method, the intrinsic value estimated for Kintetsu Group HoldingsLtd is ¥2,194 per share. With the current share price sitting roughly 41% above that level, the market price implies the stock is significantly overvalued using this cash flow-based approach.

Result: OVERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Kintetsu Group HoldingsLtd.

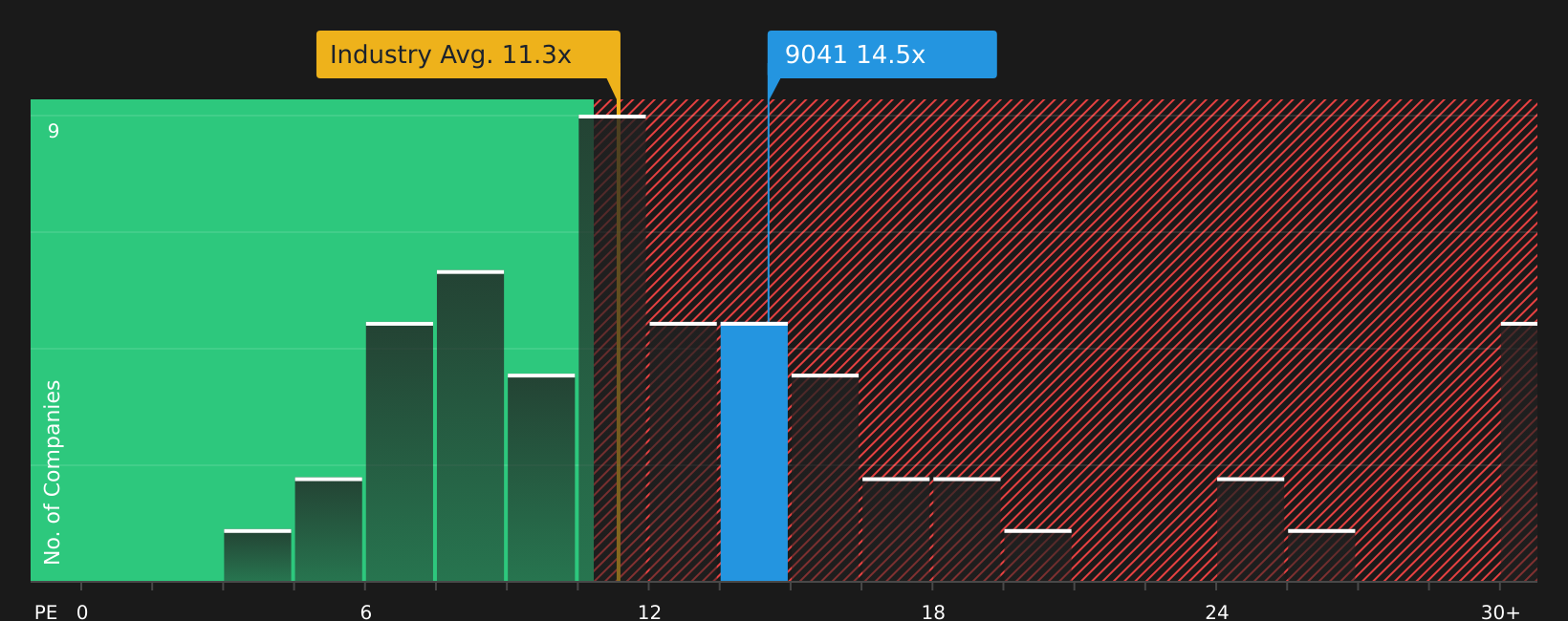

Approach 2: Kintetsu Group HoldingsLtd Price vs Earnings

When a company is consistently profitable, the Price-to-Earnings (PE) ratio is a tried-and-true way to gauge whether its shares are reasonably valued. The PE ratio measures how much investors are willing to pay for each yen of current earnings, and normal or fair PE levels can swing higher or lower depending on expectations for future growth, underlying risks, and broader market sentiment.

For Kintetsu Group HoldingsLtd, the current PE ratio stands at 13.1x. This is just above both the Transportation industry average of 13.1x and the average of its direct peers at 12.2x, suggesting the stock is priced in line with its competition. At first glance, that could indicate a fairly valued business, but there is a more nuanced way to look at it.

The “Fair Ratio,” calculated by Simply Wall St, sets a tailored benchmark by considering not just peer and industry figures but also Kintetsu Group HoldingsLtd’s earnings growth, risk profile, profit margins, and market cap. This is a more holistic approach compared to simply averaging across companies, as it accounts for variables that directly impact what investors should reasonably pay. For Kintetsu Group HoldingsLtd, the Fair PE Ratio is 15.2x, which is just modestly above its actual multiple.

Because the difference between the Fair Ratio and the company’s current PE is small, these shares look fairly priced relative to the company’s unique profile and prospects.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your Kintetsu Group HoldingsLtd Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is a simple yet powerful approach that helps you connect your perspective and research about a company to future expectations for its revenue, earnings, and margins. This creates your own story behind the numbers. With Narratives, you link a company’s story and outlook to a data-driven financial forecast, which produces your own estimate of fair value.

Narratives are available right on Simply Wall St’s Community page, making this advanced process easy and accessible for everyone. They help you compare your Fair Value with the current market price so you can quickly see if Kintetsu Group HoldingsLtd is a buy, sell, or hold for you. Narratives always stay up to date as new information, such as earnings announcements or news, becomes available.

For example, two investors might have very different Narratives for Kintetsu Group HoldingsLtd. Their estimates for Fair Value might range from as low as ¥1,900 per share to as high as ¥2,700 per share, depending on their outlook for the company’s future. With Narratives, your decisions are grounded in your own understanding, giving you a dynamic and personalized edge in the market.

Do you think there's more to the story for Kintetsu Group HoldingsLtd? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com