Evaluating Fujikura After Record Run and AI Infrastructure News in 2025

If you have been watching Fujikura’s stock lately, you are not alone. Investors are debating whether to ride the next wave or lock in profits as the share price continues its seemingly relentless climb. The numbers speak for themselves: in just the last week, Fujikura’s stock jumped 5.7%, it is up 14.9% over the past month, and the year-to-date return stands at an eye-popping 113.4%. Longer-term holders have seen truly phenomenal gains, with the stock up 247.7% over the past year, 1,525.5% in three years, and an astounding 4,997.6% over five years.

Much of this surge has been driven by renewed optimism in market sectors relevant to Fujikura, as well as increased investor interest in companies benefiting from technology infrastructure upgrades. As perceptions of risk and reward shift, the story behind these big price moves becomes even more compelling.

You are probably wondering if, after such a run, Fujikura is still undervalued or if all the good news is priced in. Here is a reality check: based on six standard valuation checks, Fujikura does not appear undervalued on any of them, giving it a valuation score of 0 out of 6. But as any savvy investor knows, traditional valuation metrics are just the starting point. Next, let us dig into those approaches and explore how to make sense of Fujikura’s rapid ascent before circling back with a smarter way to understand what the stock is really worth.

Fujikura scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.Approach 1: Fujikura Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future free cash flows and discounting them back to today's value. This provides an indication of the business’s intrinsic worth based only on its cash generation potential.

For Fujikura, the latest reported Free Cash Flow stands at approximately ¥91.96 billion. Analyst estimates extend for the next five years, with projections showing steady growth in cash flows. By 2030, Fujikura’s Free Cash Flow is forecasted to reach ¥175.20 billion. Later years are extrapolated by Simply Wall St based on observed trends. These projections use the 2 Stage Free Cash Flow to Equity approach, which considers near-term analyst forecasts and then applies longer-term growth assumptions.

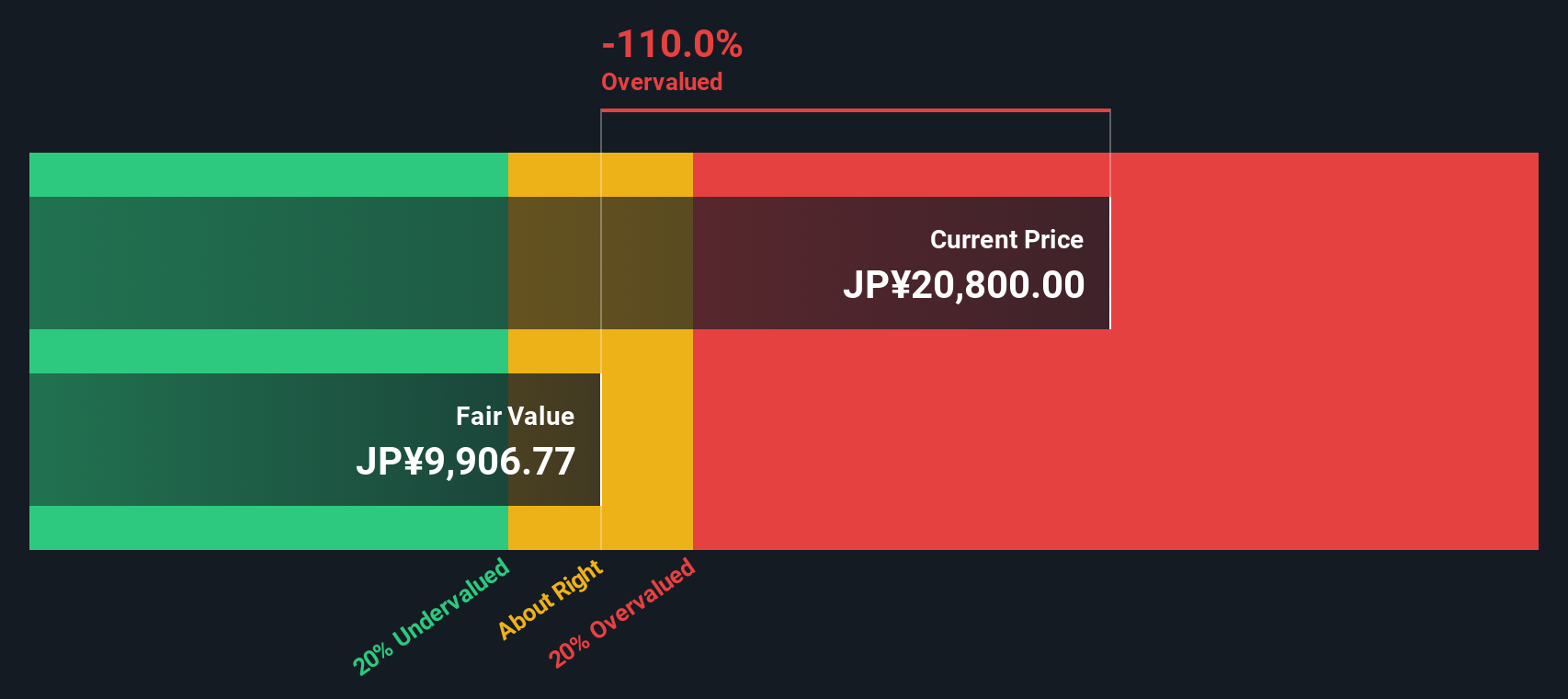

Based on this DCF model, the intrinsic value per share is calculated at ¥10,575. Compared to the current market price, this valuation suggests that Fujikura’s stock is approximately 33.3% overvalued according to today’s discounted cash flow outlook.

Result: OVERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Fujikura.

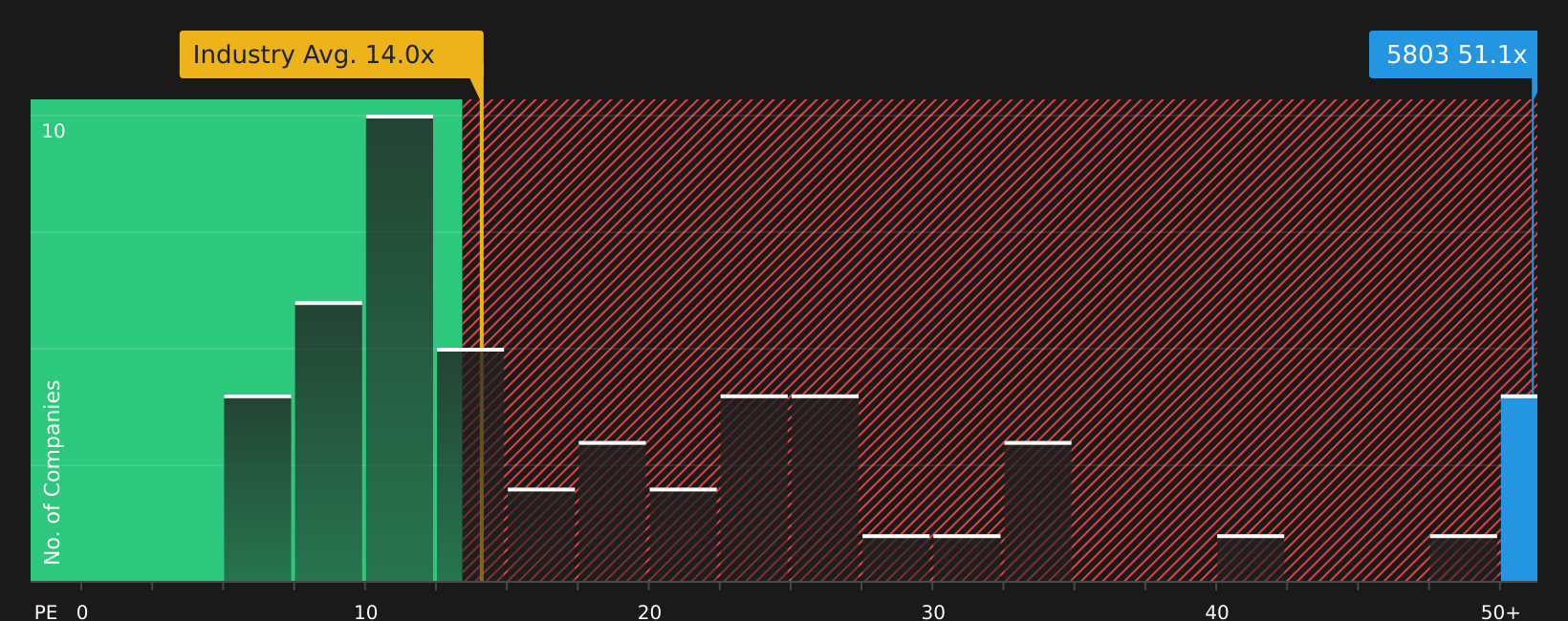

Approach 2: Fujikura Price vs Earnings (PE Ratio)

For profitable companies like Fujikura, the Price-to-Earnings (PE) ratio is a widely used way to judge value. It connects a company’s current share price to its per-share earnings, making it a direct indicator of how much investors are willing to pay for every yen of profit.

Assessing what counts as a “normal” or “fair” PE depends on a couple of things. Higher future growth expectations can justify a higher PE, as can lower risk. On the other hand, slower-growing or riskier businesses typically see their PE ratios settle lower, in line with measured expectations.

Right now, Fujikura’s PE ratio stands at 37.7x. To put that in perspective, this is well above the Electrical industry average of 13.0x, and higher than both the peer average of 21.9x. Clearly, Fujikura is priced at a premium relative to its direct competitors and the broader sector.

This is where Simply Wall St’s “Fair Ratio” comes in. Unlike simple industry or peer multiples, the Fair Ratio (36.8x for Fujikura) is calculated by factoring in expected growth, profit margins, market cap, and company-specific risks. It is designed to show what would be a reasonable PE given Fujikura’s unique situation, not just broad averages.

The difference between Fujikura’s current PE (37.7x) and its Fair Ratio (36.8x) is very slight, less than 0.10, suggesting the stock’s valuation is in line with its fundamentals and prospects.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your Fujikura Narrative

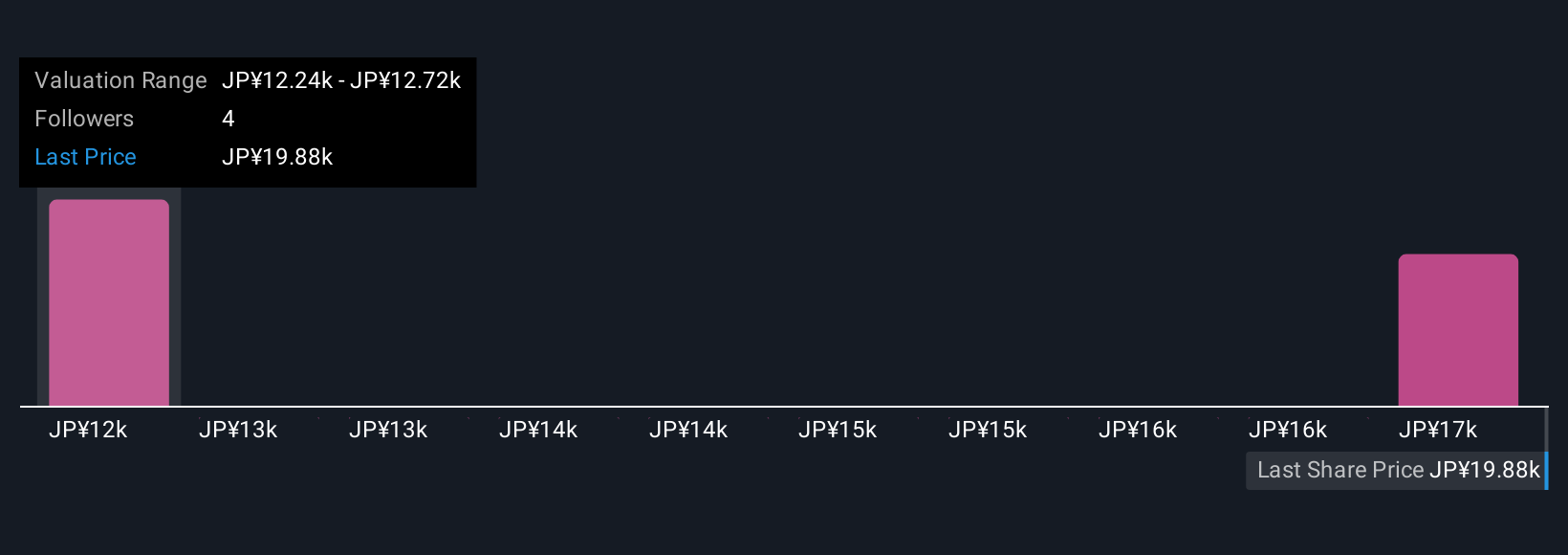

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is simply your story or perspective on a company, where you bring together your view of its potential with your own forecasts for future revenue, profit margins, and fair value. Rather than just relying on numbers, Narratives allow you to link Fujikura’s story to a detailed financial forecast and an up-to-date estimate of what the business is really worth.

Narratives are built for simplicity and are available to everyone on Simply Wall St’s Community page, where millions of investors share their views and analyses. They empower you to easily compare your Fair Value with the current Price to see if it could be the right time to buy or sell. The best part: Narratives update automatically when new information, like company news or earnings, comes in. This ensures your outlook always remains relevant and fresh.

For example, one Fujikura investor may create a Narrative with a very bullish fair value projection, while another is more cautious and calculates a much lower estimate. This makes it easy to see the range of investor sentiment and base your decisions on real stories connected to real numbers.

Do you think there's more to the story for Fujikura? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com