Heiwa Real Estate (TSE:8803): Evaluating Valuation After a Period of Steady Share Price Gains

If you’ve been keeping an eye on Heiwa Real Estate (TSE:8803), you might be wondering what’s been fueling the recent action in its share price. While there hasn’t been a headline-grabbing event this week, the stock’s steady upward movement could be sparking fresh debates among investors about whether the market is signaling optimism or simply reacting to broader sector trends. For those weighing their next move, even modest shifts can sometimes point to evolving expectations about a company’s future.

Drilling into the numbers, Heiwa Real Estate shares have climbed 25% in the past twelve months, adding to the momentum that’s been building over the past three years. Shorter-term, performance has remained positive, with gains across various timeframes. This pattern suggests that market sentiment is not only recovering but could also be shifting toward growth, especially in the context of changing risk perceptions within the real estate sector.

So with this year’s consistent gains, is Heiwa Real Estate now trading at an attractive valuation, or is the market already factoring in all the upside potential?

Price-to-Earnings of 16.4x: Is it justified?

Heiwa Real Estate is currently trading at a price-to-earnings (P/E) ratio of 16.4x, which is considered expensive compared to both the Japanese real estate industry average of 11.5x and the peer average of 12.6x. This signals that investors are paying a higher price for each unit of company earnings than they would for many industry peers.

The P/E ratio is a commonly used metric for evaluating how the market values a company's growth potential and profitability against its reported earnings. In real estate, where steady income and asset values are key, a higher P/E can indicate expectations for stronger growth or superior profitability. In this case, it suggests that current market optimism may already be reflected in the price, potentially outpacing actual financial performance and projections.

Given that earnings are forecast to decline over the next few years and the current premium to industry averages, the high P/E multiple raises questions about whether investors are being overly optimistic about future returns.

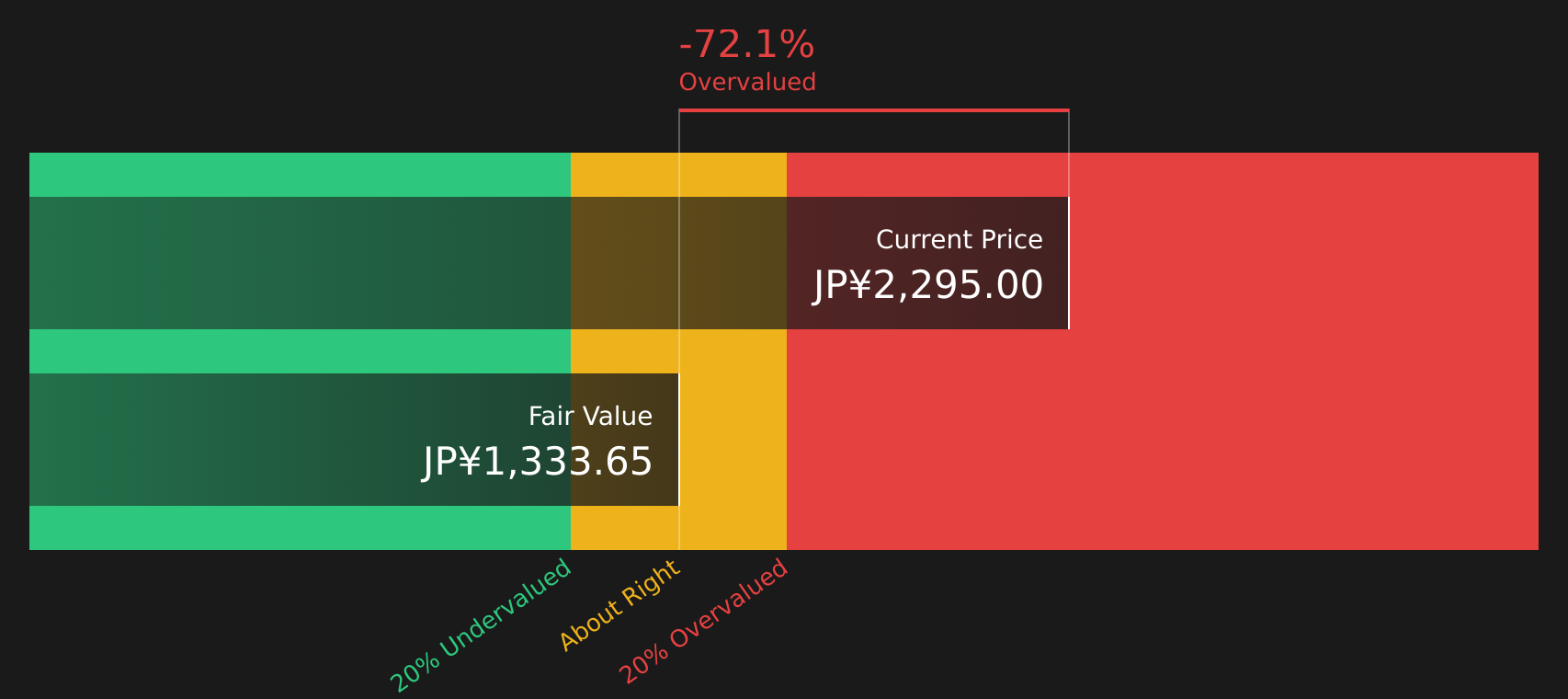

Result: Fair Value of ¥1,173.61 (OVERVALUED)

See our latest analysis for Heiwa Real Estate.However, slowing net income growth and Heiwa Real Estate’s premium valuation could trigger future volatility if investor expectations are not met.

Find out about the key risks to this Heiwa Real Estate narrative.Another View: Discounted Cash Flow Model

While multiples suggest Heiwa Real Estate is trading at a premium, our DCF model offers a different perspective. It calculates value based on expected future cash flows, and in this case, it points to the shares also being overvalued. But which approach best captures the real story—market sentiment or cash flow fundamentals?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Heiwa Real Estate Narrative

If you have a different view or prefer charting your own path, you’re free to dig into the data and assemble your perspective, all in just a few minutes. Do it your way

A great starting point for your Heiwa Real Estate research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Every moment you hesitate is a chance missed. Make smarter moves by searching for outstanding companies beyond Heiwa Real Estate using the Simply Wall Street Screener.

- Capture opportunities with unbeatable value by checking out stocks that are currently priced well below their true worth through our undervalued stocks based on cash flows.

- Accelerate your portfolio growth by finding companies driving breakthroughs in healthcare with our exclusive focus on healthcare AI stocks.

- Maximize income potential by targeting businesses offering strong yields and reliable payments via our selection of dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com