How Prisma SASE 4.0’s AI Security Launch at Palo Alto Networks (PANW) Has Changed Its Investment Story

- Earlier this month, Palo Alto Networks introduced Prisma SASE 4.0, an AI-driven secure access service edge platform with innovations such as real-time browser-based threat neutralization and adaptive private application security.

- This launch highlights the company's rapid response to the growing importance of enterprise browser security as critical data and applications increasingly shift online, setting them apart in the competitive cybersecurity landscape.

- We’ll explore how these new AI security advancements shape Palo Alto Networks’ investment narrative and growth prospects in the evolving cloud security market.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Palo Alto Networks Investment Narrative Recap

For shareholders in Palo Alto Networks, the core investment belief centers on the accelerating adoption of AI-powered and cloud-based security solutions by enterprises, supporting recurring revenue and margin potential. The launch of Prisma SASE 4.0 reinforces the company’s ability to keep pace with evolving threats, though the most immediate catalyst, expansion of Secure Access Service Edge (SASE) ARR, may see incremental rather than material impact from this release. Ongoing integration risks, including those from acquisitions, remain a watchpoint for short-term earnings stability.

A recent announcement that resonates with this development is the April update of Prisma Access Browser 2.0, which targeted AI security features and operational resilience in browser-based environments. This sequence of launches illustrates Palo Alto Networks' focus on building out their SASE portfolio, a category that continues to drive growth in annual recurring revenue and frames the company’s near-term catalysts around SASE platform adoption.

By contrast, investors should also weigh the risk that growing regulatory requirements and global data sovereignty laws could...

Read the full narrative on Palo Alto Networks (it's free!)

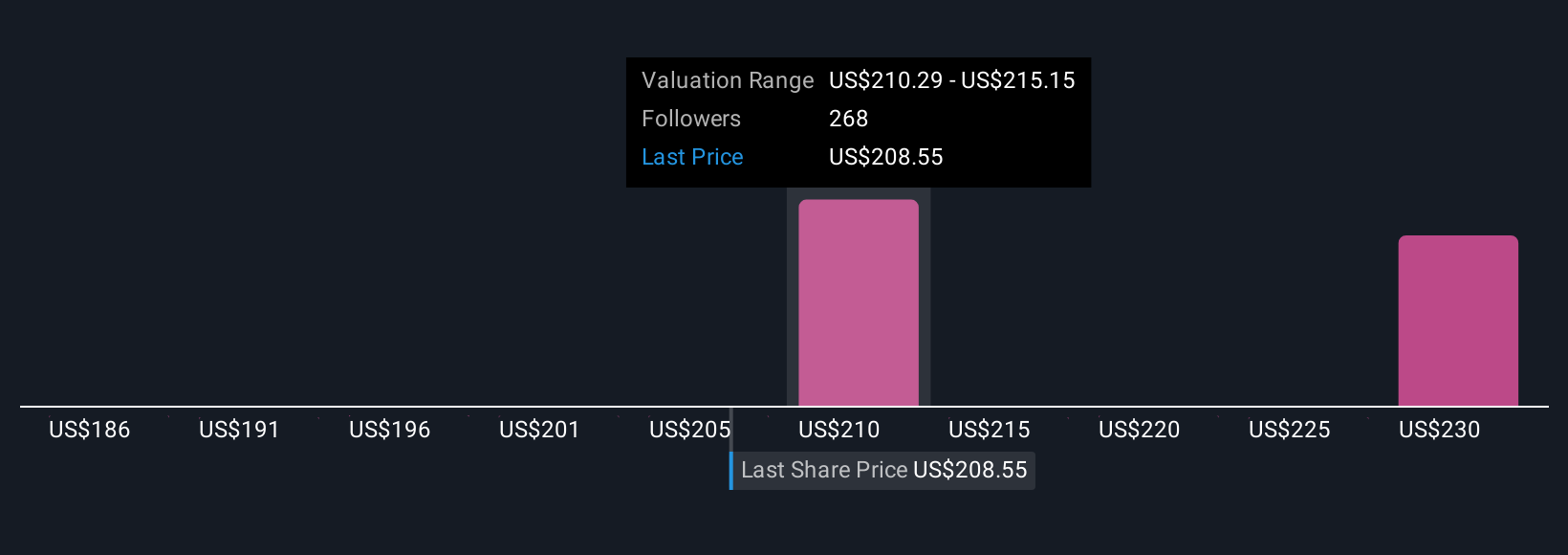

Palo Alto Networks is projected to reach $13.3 billion in revenue and $2.0 billion in earnings by 2028. This outlook requires annual revenue growth of 13.1% and a $0.9 billion increase in earnings from the current $1.1 billion.

Uncover how Palo Alto Networks' forecasts yield a $214.21 fair value, a 9% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community contributed 18 different fair value estimates for Palo Alto Networks ranging from US$181 to US$237.49 per share. While many highlight the company’s growth in SASE and recurring revenue, perspectives vary widely on the influence of integration risks and competitive pressures, showing just how much investor viewpoints can differ.

Explore 18 other fair value estimates on Palo Alto Networks - why the stock might be worth as much as 21% more than the current price!

Build Your Own Palo Alto Networks Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Palo Alto Networks research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Palo Alto Networks research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Palo Alto Networks' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 28 stocks are leading the charge.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com