Exploring Sinopec’s Value Following Recent Global Oil Price Fluctuations

If you have ever found yourself staring at China Petroleum & Chemical’s ticker and wondering if now is the right time to buy, hold, or move on, you are definitely not alone. This is a stock that has kept investors on their toes, juggling cycles of volatility and hints of long-term promise. Over the last year, the share price has gained 3.2%. If we stretch the timeline to five years, the stock has more than doubled, up an impressive 102.6%. That said, price swings in the shorter term can be nerve-wracking, with a 2.4% bump in the last week but a 5.6% slide over the past month. These moves reflect the market’s shifting views on energy demand and sector risk. Even year to date, the stock is still down 4.5%, hinting at ongoing caution amid global market developments rather than anything fundamentally alarming.

Valuing China Petroleum & Chemical is not as straightforward as plugging numbers into a single formula. The company currently gets a value score of 3 out of 6, indicating it passes half of the major undervaluation checks. If you are wondering how those checks stack up and whether the story told by traditional valuation models says enough, you are in the right place. Next, we will break down these methods and see how this company measures up. Stick around, because there is an even smarter way to think about valuation that could help you make more informed decisions.

Why China Petroleum & Chemical is lagging behind its peersApproach 1: China Petroleum & Chemical Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today's value. This approach relies on the idea that the company is ultimately worth the sum total of all the cash it will generate for shareholders, adjusted for the time value of money.

For China Petroleum & Chemical, the latest twelve months' Free Cash Flow (FCF) was CN¥21.9 Billion. Analysts see this figure climbing over time, with projections suggesting FCF could reach around CN¥45.5 Billion in ten years, growing at a modest annual pace through the next decade. While analyst estimates extend five years out, further growth is extrapolated for years beyond that using reasonable assumptions about the company and industry.

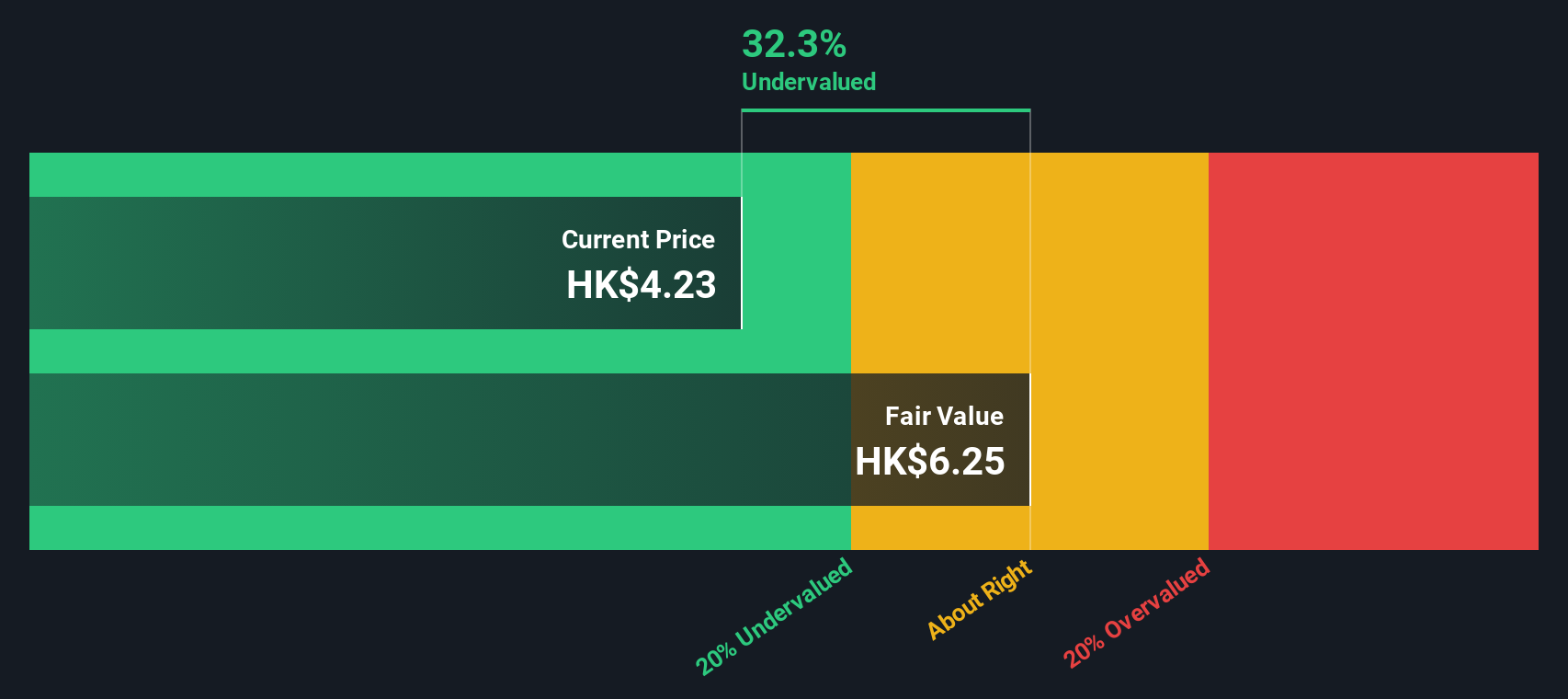

By plugging these forecasts into a two-stage DCF model, the estimated fair value of the stock is HK$5.96 per share. This is about 29.0% higher than its current trading price, which suggests the stock is meaningfully undervalued using this model.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for China Petroleum & Chemical.

Approach 2: China Petroleum & Chemical Price vs Earnings

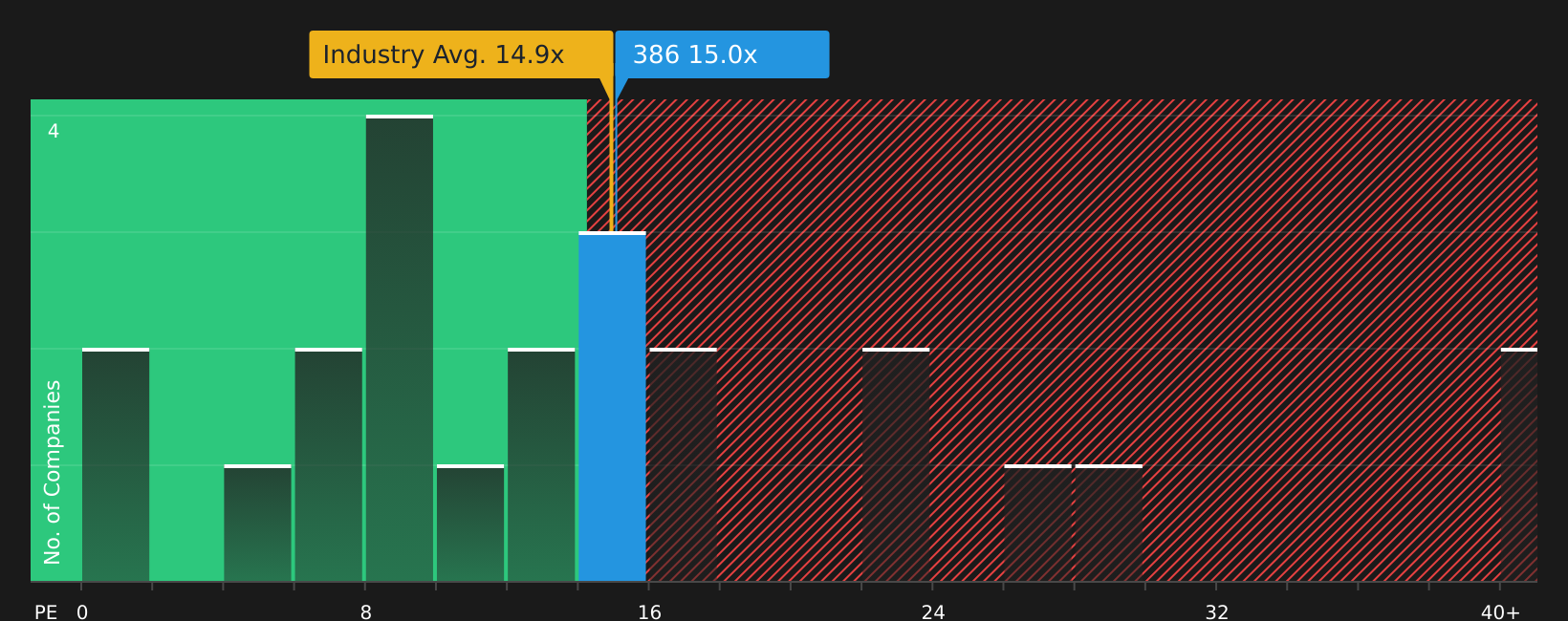

The Price-to-Earnings (PE) ratio is a widely used valuation tool for profitable companies like China Petroleum & Chemical, as it clearly connects the company’s current share price to its underlying earnings. For investors, the PE ratio provides a shorthand for how much they are paying for each dollar of profit the business generates.

What counts as a "normal" or "fair" PE ratio depends on growth outlook and risk. Higher expected earnings growth or strong competitive positioning can justify a higher PE, while increased risks or slowing growth tend to hold the multiple back. Comparing a company’s PE in context helps investors gauge whether a stock is priced optimistically or pessimistically by the market.

Currently, China Petroleum & Chemical trades at a PE ratio of 13.18x. This is just above the Oil and Gas industry average of 12.53x, and higher than its peer group’s average of 8.18x. Simply Wall St’s Fair Ratio for the company, which adjusts for earnings growth prospects, industry landscape, profit margins, market size, and risk profile, sits at 14.06x. In this context, the Fair Ratio serves as the most tailored benchmark for valuation because it captures not just what other companies are doing but also the specific qualities and future expectations for China Petroleum & Chemical itself.

Since the company's actual PE ratio and its Fair Ratio are very close, the stock appears to be trading at around fair value using this earnings-based approach.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your China Petroleum & Chemical Narrative

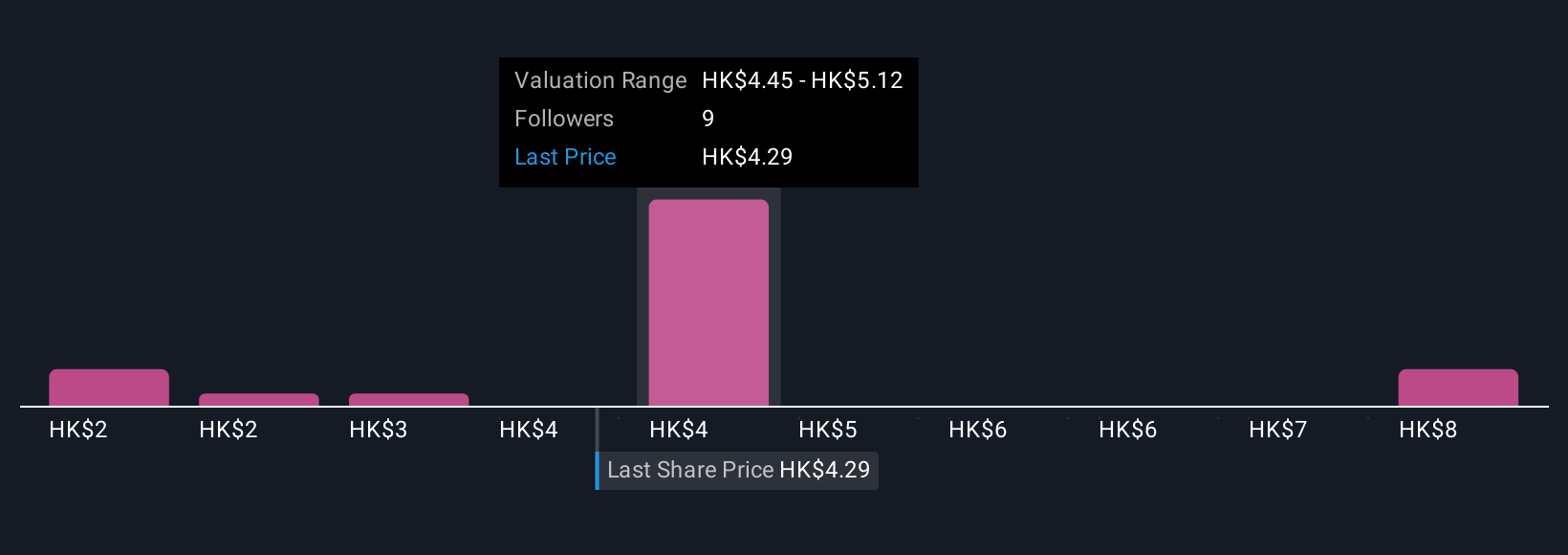

Earlier we mentioned that there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is simply your personal story or perspective about a company, connecting your assumptions about its future growth, earnings, and margins to an estimated fair value. Narratives transform raw numbers into a story, linking what you believe about China Petroleum & Chemical with a clear financial forecast and a fair value calculation.

This approach takes the guesswork out of decision making. On Simply Wall St's Community page, used by millions of investors, you can easily explore, create, or update Narratives for any company, making complex analysis much more accessible. Narratives allow you to compare your fair value estimate to the current price so you can confidently decide when the stock is a buy or a sell based on your view of its potential.

Narratives also stay up-to-date, automatically incorporating new information like earnings reports or breaking news, so your assessments are always relevant. For instance, some investors see China Petroleum & Chemical's value as high as HK$8.00, while others set it as low as HK$4.20, reflecting the power of different stories and expectations shaping each Narrative.

Do you think there's more to the story for China Petroleum & Chemical? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com