Peyto Exploration & Development (TSX:PEY): Valuation Insight as Dividend Strength and Stability Drive Renewed Interest

Peyto Exploration & Development (TSX:PEY) has been catching more attention lately, and it is not just about its share price. Recent news has put the spotlight on Peyto as a standout dividend stock within the natural gas sector, highlighting its solid balance sheet, low debt levels, and steady production. The company's reputation for financial strength and consistent cash flow is taking center stage, appealing to investors searching for long-term, dependable payouts.

So how has that buzz translated to stock performance? Over the past year, Peyto’s shares have surged 36%, handily outpacing many peers and building on significant long-term momentum. While there have been dips lately, including a 5% slide over the past month, the bigger picture shows Peyto remains on a strong upward track, supported by ongoing revenue and earnings growth, both comfortably positive this year. Investors seem to be weighing long-term reliability against short-term volatility.

After such a run, the natural question is whether Peyto is now undervalued given its dividend appeal, or if recent price gains already capture most of the upside. Is there more room for growth, or is the market now fully pricing in Peyto’s future?

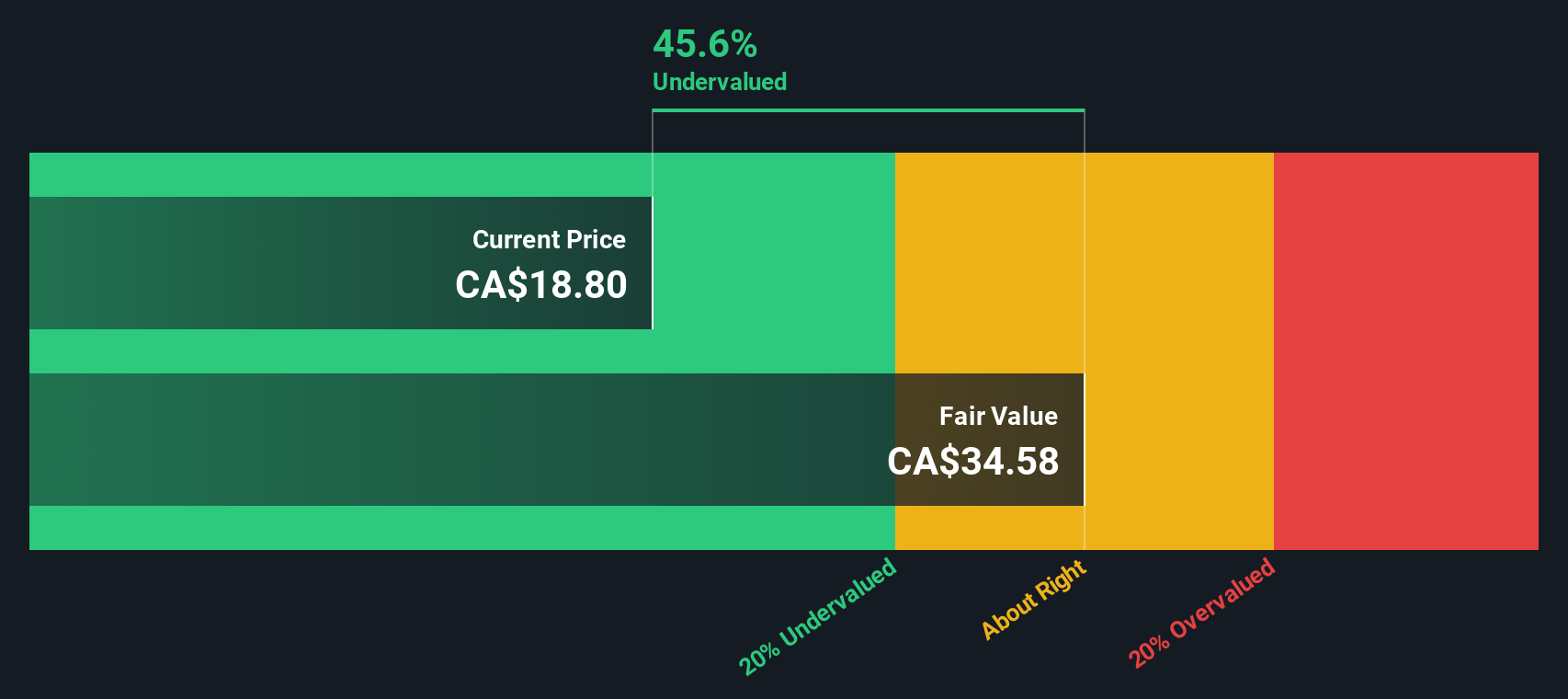

Most Popular Narrative: 15% Undervalued

The most widely followed valuation narrative suggests that Peyto Exploration & Development is trading at a substantial discount to its fair value. Current pricing reflects a notable gap versus analysts’ consensus target, rooted in forward-looking profit and revenue expectations.

“Ramp-up of LNG export facilities (notably LNG Canada's commencement of exports) is set to increase long-term demand and support higher benchmark prices for Canadian natural gas. This is expected to enhance Peyto's sales volumes and revenue prospects. Peyto's consistently low-cost structure, driven by efficient Deep Basin development, cost reductions in drilling and completions, and focus on high-margin inventory, positions the company to maintain resilient net margins even during commodity price volatility.”

Curious what could be pushing Peyto’s shares so much higher than the market? The key narrative here centers on aggressive revenue growth, solid profitability, and a future multiple typically seen in faster-growing sectors. Want to know what bold financial forecasts and assumptions make analysts so bullish on this energy stock? Dive in for the data that’s fueling this surprising value call.

Result: Fair Value of $21.52 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent infrastructure bottlenecks and slow LNG export ramp-up could limit Peyto’s growth potential. This may challenge the bullish valuation narrative.

Find out about the key risks to this Peyto Exploration & Development narrative.Another View: DCF Model Adds Perspective

While analysts emphasize future earnings and industry targets, our DCF model also indicates the stock is undervalued. This suggests that there may be upside from a cash flow perspective. But which approach offers the more accurate picture?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Peyto Exploration & Development Narrative

If you'd like to dig deeper and craft your own perspective, you're welcome to put the numbers to the test and share your outlook. Do it your way.

A great starting point for your Peyto Exploration & Development research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Set your portfolio apart by targeting opportunities others overlook. Access handpicked screeners that highlight breakthrough sectors and strong financial profiles, so you never miss the next big move.

- Uncover unique value plays and track stocks trading below their true worth with our undervalued stocks based on cash flows.

- Capture income streams that stand out, using our tool to spotlight dividend stocks with yields > 3% currently offering impressive yields and financial strength.

- Get ahead as artificial intelligence reshapes industries and pinpoint rising stars with our AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com