RWE (XTRA:RWE) Valuation in Focus as New France Projects and Apollo Grid Deal Drive Energy Transition Momentum

RWE (XTRA:RWE) has been in the news lately, and for good reason. Over the past few weeks, the company has kicked off four new wind farms and a solar power plant in France, boosting its renewable energy footprint. It also struck a long-term partnership with Apollo Global Management to secure funding for grid expansion via its stake in Amprion. These moves signal real momentum in RWE’s strategy to cement itself at the forefront of Europe’s energy transition.

Unsurprisingly, recent headlines have caught the attention of investors, with the stock gaining 2.6% over the past week and more than 21% year-to-date. While momentum earlier in the summer was more subdued, this fresh batch of projects and strategic collaborations underlines RWE’s ongoing push for growth. Coupled with steady revenue trends and a track record of turning renewable investments into higher capacity, it is no wonder the market is paying attention.

With the shares up solidly this year, do these infrastructure investments leave room for further upside, or has the market already priced in RWE’s future growth?

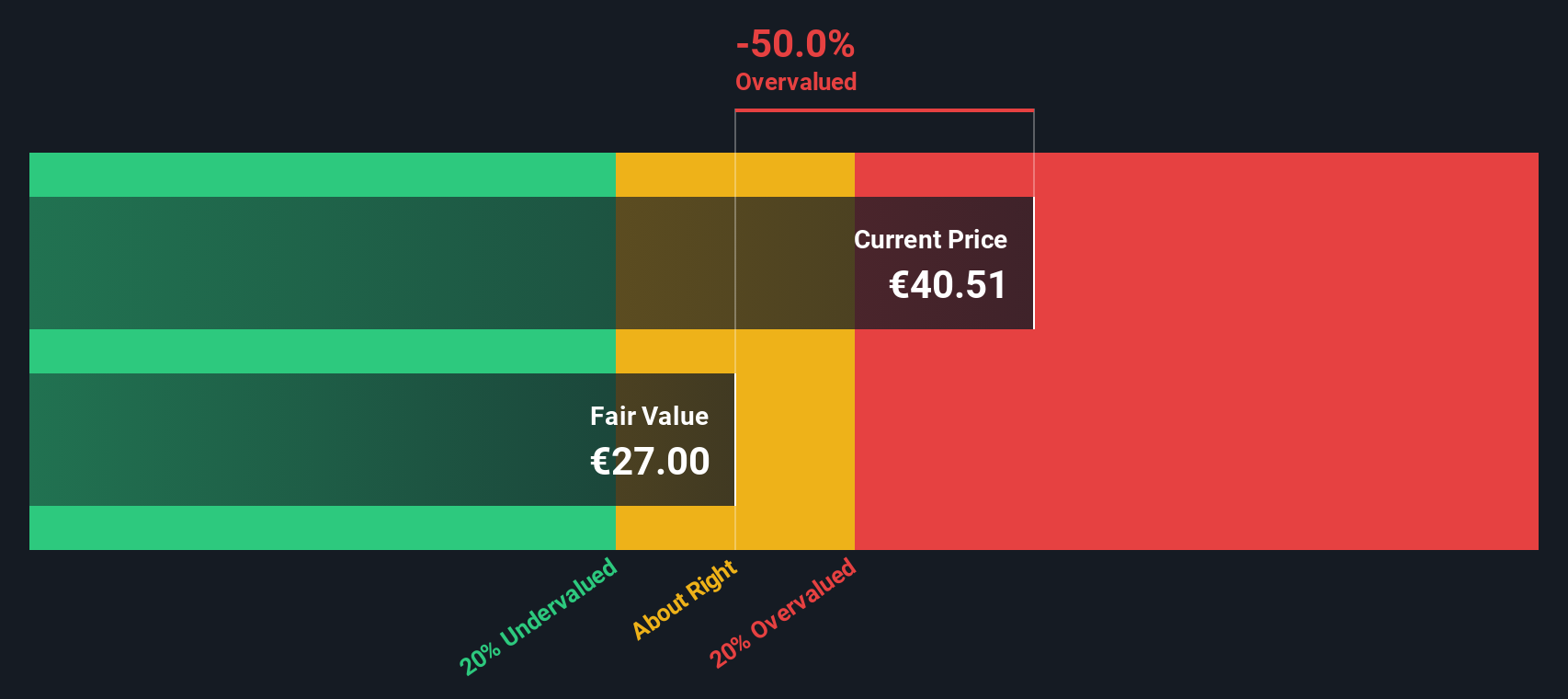

Most Popular Narrative: 16.8% Undervalued

The current market narrative considers RWE to be significantly undervalued compared to analyst expectations, with robust underlying assumptions supporting this perspective.

Major policy tailwinds in core markets, the U.K. retention of a single price zone, extension of CfD periods to 20 years, higher auction price caps, and the new U.S. "Big Beautiful Bill" with tax incentives, are expected to provide greater revenue visibility and de-risk project cash flows. These factors are likely to support higher recurring revenues and improved earnings quality over time.

Want to know why analysts believe RWE could surge higher? This fair value estimate incorporates bold revenue gains and ambitious profit assumptions, hinting at a future financial profile that rivals some of Europe’s fastest-growing energy companies. Curious what’s fueling such optimism and what numbers are setting this target? Uncover the full story to see which key assumptions might surprise you.

Result: Fair Value of €43.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent weak wind conditions and global supply chain pressures could undermine RWE’s growth outlook if these factors weigh on renewable output and project profitability.

Find out about the key risks to this RWE narrative.Another View: Our DCF Model

Taking a different approach, the SWS DCF model suggests that RWE’s current share price actually sits above its estimate of fair value. This challenges assumptions from the analyst consensus. Could the market be missing something, or are future growth projections too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own RWE Narrative

If you see things differently or want to dig into the numbers yourself, you can build your own scenario in just a few minutes. Do it your way.

A great starting point for your RWE research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t sit on the sidelines while incredible opportunities are waiting. Use the Simply Wall Street Screener to pinpoint picks tailored to your strategy and interests.

- Uncover hidden gems among small companies making big moves with penny stocks with strong financials. This screener highlights ambitious businesses with financial muscle.

- Capitalize on the AI revolution by checking out AI penny stocks. Find exciting tech disruptors shaping our digital future with smart innovation.

- Tap into potential bargains others might overlook by browsing undervalued stocks based on cash flows and focus on companies where cash flows point to strong value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com