Assessing Kaken Pharmaceutical (TSE:4521) Valuation Following Subtle Share Price Moves

Taking a Closer Look at Kaken Pharmaceutical (TSE:4521) After Recent Moves

The market has seen a quiet shift in Kaken Pharmaceutical (TSE:4521) shares in recent weeks, and while no dramatic event stands out, the latest moves may still catch the attention of value-minded investors. When stocks drift upward or downward without a clear catalyst, it often raises questions, especially for those weighing whether this is simply noise or a subtle signal worth investigating. Investors are now left wondering if these price changes hint at underlying opportunity, or if they are more a function of shifting sentiment.

Over the past month, Kaken Pharmaceutical has seen its price edge up nearly 1%, with a slight gain continuing over the past 3 months. That said, the stock remains down around 15% since the start of the year, despite being up just under 4% over the past 12 months. Longer-term, the performance is mixed, marked by both growth stretches and more recent periods of decline. Against that backdrop, declining revenues and net income reported in the most recent annual results may be shaping market expectations, even while some long-term return figures remain positive.

After a year of modest gains and uninspiring financial results, is Kaken Pharmaceutical a value play right now, or is the market already bracing for weaker growth ahead?

Price-to-Earnings of 11.8x: Is it justified?

Kaken Pharmaceutical trades at a price-to-earnings (P/E) ratio of 11.8x, which is below both the Japanese market average of 14.7x and the industry average of 16.3x. This suggests that, relative to peers, the market may be assigning a lower valuation to the company's current and future earnings stream.

The price-to-earnings multiple reflects what investors are willing to pay for each unit of earnings. In the pharmaceutical sector, this ratio helps gauge if a company is priced for growth, stability, or if there is skepticism about its prospects. With Kaken Pharmaceutical’s P/E below industry and market norms, this implies that either earnings are expected to shrink or the market has overlooked some underlying value.

While the P/E ratio appears attractive, it is important to consider the company’s mixed track record of recent profit growth alongside forecasts of declining earnings. The discount to peers highlights caution in the market regarding future performance. This could also signal an opportunity if current headwinds prove temporary.

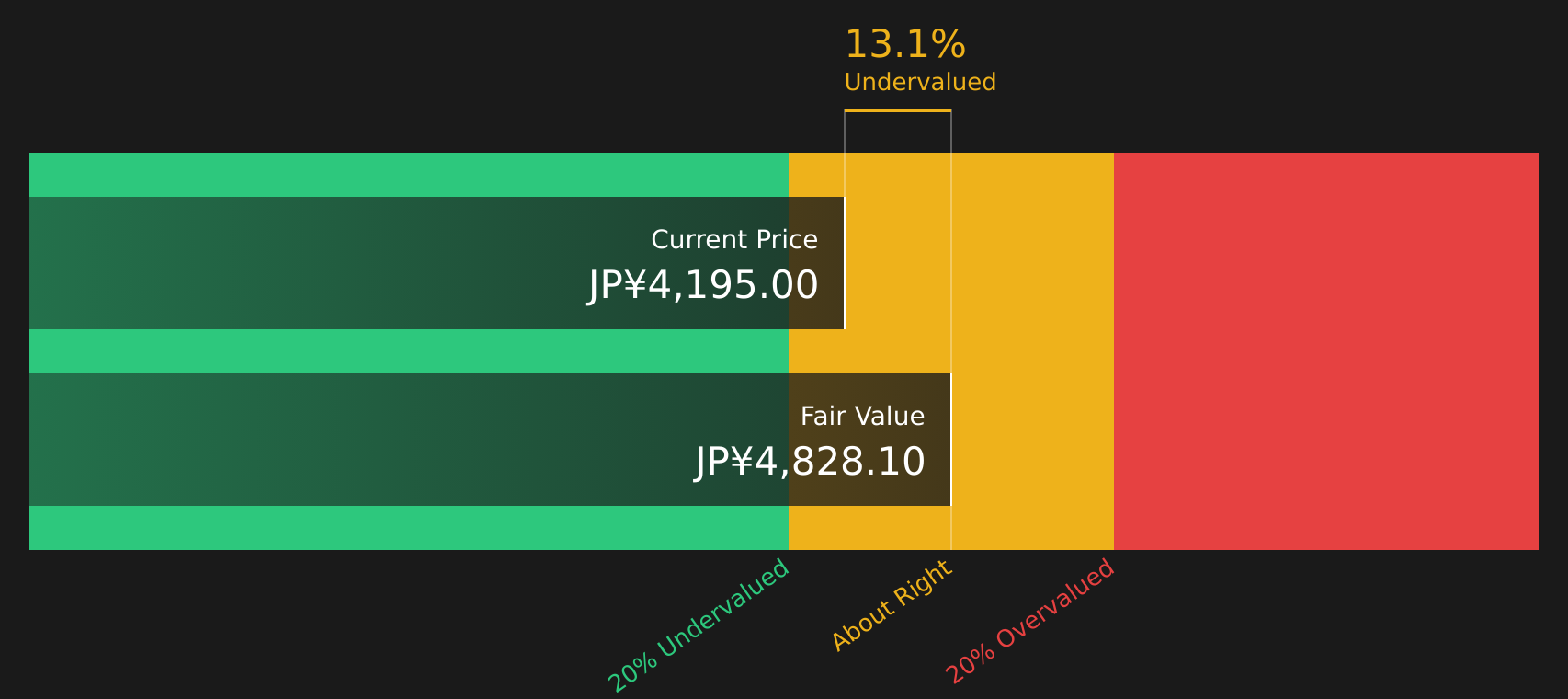

Result: Fair Value of ¥3,810.21 (ABOUT RIGHT)

See our latest analysis for Kaken Pharmaceutical.However, persistent declines in revenue and net income growth could continue dragging on sentiment, especially if industry headwinds intensify in the coming quarters.

Find out about the key risks to this Kaken Pharmaceutical narrative.Another View: Discounted Cash Flow Model

While a low earnings multiple may suggest value, the SWS DCF model paints a different story by indicating Kaken Pharmaceutical could be slightly overvalued at current prices. How much weight should investors give each approach?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Kaken Pharmaceutical Narrative

Keep in mind, if you see things differently or want to dig into the numbers yourself, you can construct your own perspective in just a few minutes. Do it your way.

A great starting point for your Kaken Pharmaceutical research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Unlock more than just market averages and give yourself an edge. Don’t let tomorrow’s best opportunities pass you by; make the most of what’s out there.

- Supercharge your search for hidden gems by using the tool for penny stocks with strong financials. See which undervalued outliers could be poised to move with penny stocks with strong financials.

- Tap into the AI boom by checking out companies driving real progress in artificial intelligence. Find your next growth star with AI penny stocks.

- Boost your portfolio income by targeting quality businesses offering healthy yields over 3%. Zero in on tomorrow’s income winners with dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com