Should Investors Reconsider Millennium bcp as Shares Surge 82% Ahead of 2025?

Thinking about what to do with Banco Comercial Português shares? You are not alone. After a wild few years, this stock has grabbed more attention from investors looking for growth and value. Let us face it, numbers rarely lie, and Banco Comercial Português has put together a pretty eye-catching performance lately. Over the past year alone, the stock is up an incredible 81.7%, with a mind-blowing 776.0% rally over five years. Even after some recent turbulence, including a 7.2% dip over the last month, the year-to-date return stands tall at 56.2%.

This surge has not happened in a vacuum. Like many European banks, Banco Comercial Português has benefited from changing economic winds and shifting investor appetite for financial stocks. There is a buzz around Portuguese equities, fueled by broader market stability and renewed optimism around domestic banking. That said, big runs like this can leave investors asking whether there is still value left or if the stock is starting to look expensive.

With a value score of just 2 out of 6, Banco Comercial Português only ticks the undervalued box on a couple of valuation checks. This might raise some eyebrows if you are hunting for bargains. In the next section, we will break down how different valuation methods stack up for this bank, and later on, we will tackle what really matters when figuring out if Banco Comercial Português is still a buy.

Banco Comercial Português scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.Approach 1: Banco Comercial Português Excess Returns Analysis

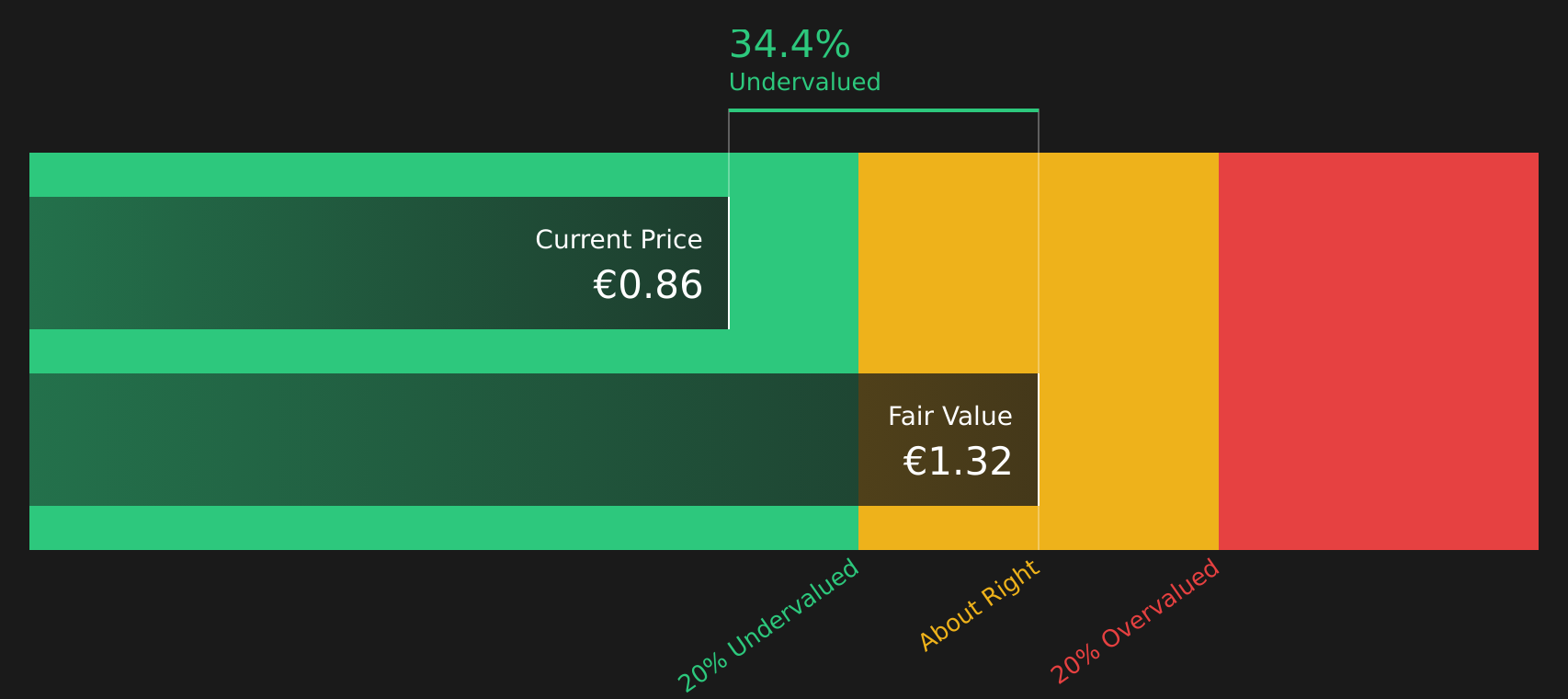

The Excess Returns valuation model focuses on how much profit a business generates above its cost of equity. For banks like Banco Comercial Português, this means looking at the return on invested capital to see if the bank makes more than what shareholders expect as compensation for their risk.

Banco Comercial Português stands out with a Book Value of €0.46 per share and a Stable EPS of €0.08 per share, based on weighted future Return on Equity estimates from 12 analysts. The Cost of Equity is €0.05 per share, resulting in an Excess Return of €0.03 per share. Over the long run, the bank’s Average Return on Equity sits at an impressive 14.61%. Meanwhile, the Stable Book Value is projected to rise to €0.52 per share, reflecting analysts’ expectations for steady growth.

This model estimates Banco Comercial Português is currently trading at a 25.8% discount to its intrinsic value, which suggests the stock is significantly undervalued based on its ability to generate excess returns for shareholders.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Banco Comercial Português.

Approach 2: Banco Comercial Português Price vs Earnings

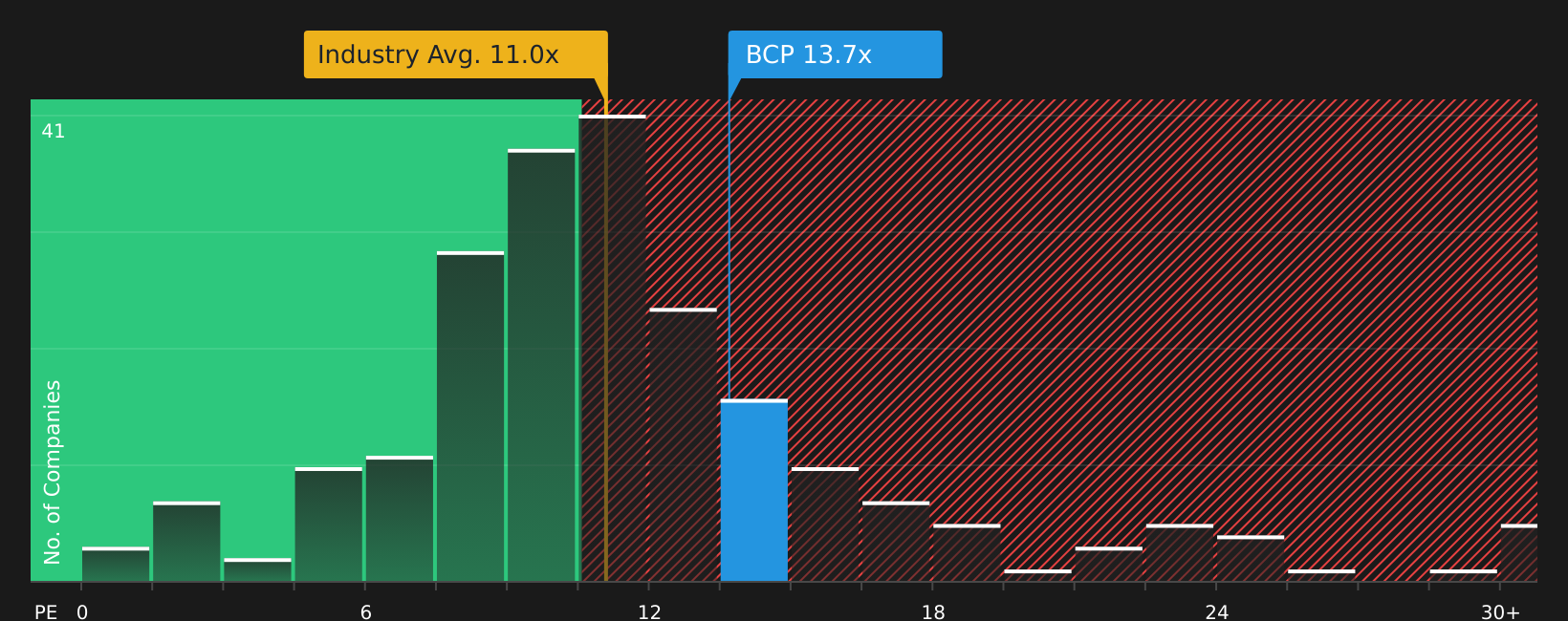

The Price-to-Earnings (PE) ratio is a popular and reliable way to value profitable companies like Banco Comercial Português. This metric lets investors quickly see how much they are paying for each euro of earnings, making it especially useful when profits are stable and growing. Generally, higher growth expectations or lower risk justify higher PE ratios, while slower growth or more risk would drag that number lower.

Banco Comercial Português currently trades at a PE of 12x. For context, this is above the average PE for European banks, which stands at 10.4x, and also ahead of the 8.4x average for its direct peers. On the surface, this suggests the market is placing a premium on Banco Comercial Português, likely due to its impressive rally and outlook. However, simply comparing to peer or industry averages can be misleading, since these numbers do not account for company-specific strengths or unique risks.

This is where Simply Wall St's proprietary "Fair Ratio" offers a sharper lens. Unlike generic averages, the Fair Ratio blends growth prospects, risk profile, profit margins, market cap, and industry dynamics to estimate what a truly reasonable PE should be for this specific business. Judging by this holistic benchmark, Banco Comercial Português's 12x PE lines up nearly exactly with its Fair Ratio, signaling that the shares are trading at a price that matches their underlying fundamentals.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your Banco Comercial Português Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is your unique, story-driven perspective on a company. It links what you believe about Banco Comercial Português’s future, such as growth in revenue or profit margins, directly to a financial forecast and then to a fair value estimate. This approach takes investing beyond static numbers, letting you quickly see how your view compares with others. Narratives are available to everyone on Simply Wall St’s Community page, where millions of investors share their outlooks. This makes it an easy and accessible tool to compare, discuss, and refine your investment thesis.

With Narratives, you can see how your scenario for Banco Comercial Português responds to changes. For example, you might expect the bank’s fair value to be at the high end, or you may see more risk and lower potential, just as other investors do. As new information becomes available, Narratives update in real time, helping you decide if the current price still matches your view to buy, sell, or hold.

Do you think there's more to the story for Banco Comercial Português? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com