Solaria (BME:SLR): Analyzing Valuation as Investor Sentiment Shifts This Month

If you have been eyeing Solaria Energía y Medio Ambiente (BME:SLR) recently, the subtle shifts in its share price might have caught your attention. There has not been a major event driving today’s move, but slight declines over the past month and week have left some shareholders wondering if the market is reacting to something beneath the surface or simply drifting with broader trends. For anyone weighing what to do next, the current climate prompts questions about the company’s true value and growth story.

Looking back, the past year for Solaria Energía y Medio Ambiente has been a mixed bag. The stock’s total return is roughly flat over the year but shows a strong upward momentum over the past three months, with a 32% gain suggesting some revived interest or shifting sentiment among investors. However, the share price has edged lower day-to-day and week-to-week, reflecting a touch of caution or pause compared to earlier in the year. Meanwhile, the company has continued to grow both revenue and net income on an annual basis, even if that progress has not always translated to share price stability for long-term holders.

With the stock still well off its highs from recent years but showing pockets of renewed momentum, investors may be questioning whether this is a chance to pick up Solaria at a compelling valuation or if the market is already factoring in everything it knows about the business's prospects.

Most Popular Narrative: 5% Overvalued

According to the most followed narrative, Solaria Energía y Medio Ambiente is slightly overvalued relative to its calculated fair value using consensus analyst projections and a discount rate of 9.8%.

Solaria's diversification into real estate associated with renewables, Generia, and the data center business is expected to be a significant catalyst for future growth. This should support increased revenue and expanding margins over time. The company is constructing more than 1.5 GW of solar capacity in Spain, with the goal of significantly increasing its operational capacity in the short term. This increased capacity is likely to boost revenue and improve earnings through economies of scale.

Curious about what’s powering this premium? The narrative hinges on aggressive expansion plans, bold operational targets, and elevated future profit multiples. Want to see which long-range financial assumptions support that price but could shift everything if conditions change? The full narrative reveals the forecasts that set this valuation on edge.

Result: Fair Value of €11.42 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, a sharper government tax on revenue and continued reliance on project financing could quickly challenge these optimistic growth expectations for Solaria.

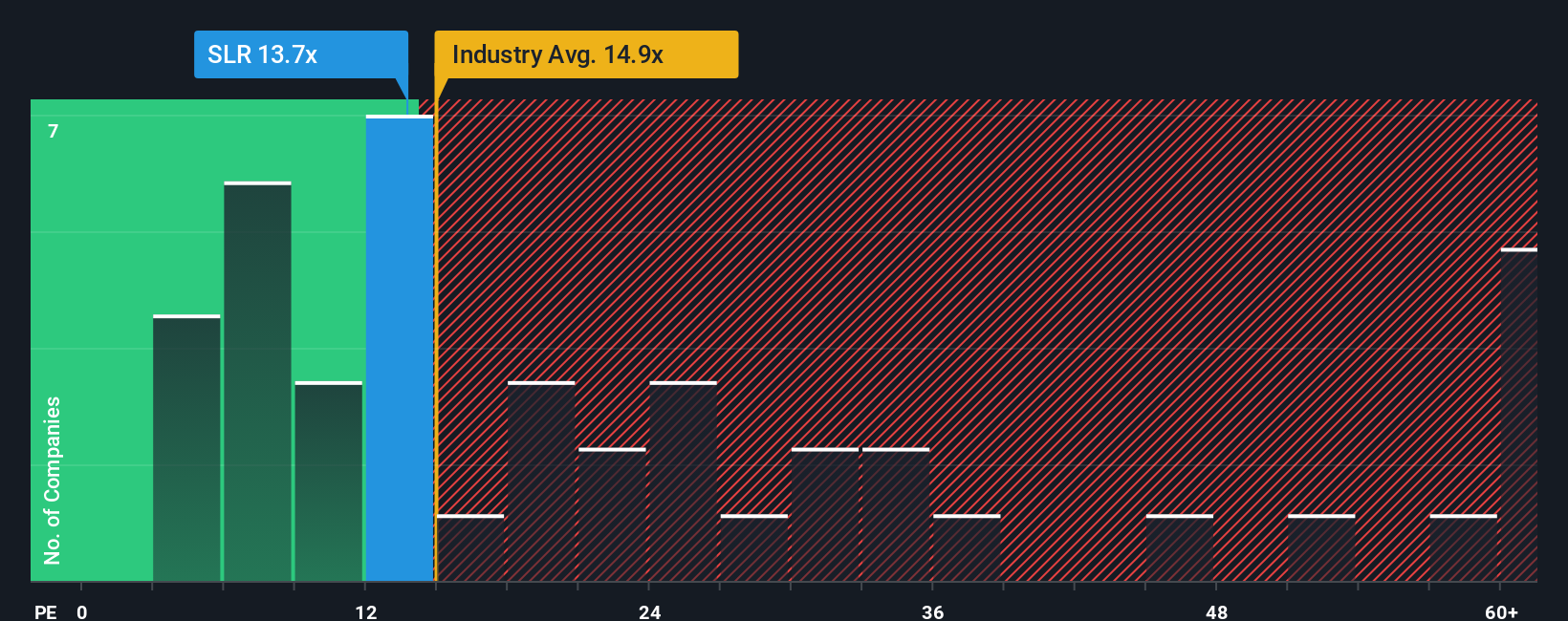

Find out about the key risks to this Solaria Energía y Medio Ambiente narrative.Another Perspective: Relative Value Looks Compelling

Taking a different angle, the company appears attractively priced compared to the broader European sector when we look at one widely-followed metric. Its shares are trading below the industry average, which challenges the prior overvaluation claim. However, will the market continue to agree?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Solaria Energía y Medio Ambiente Narrative

If you see the story differently or want to form your own view from the numbers, you can quickly shape your own perspective in just a few minutes. Do it your way.

A great starting point for your Solaria Energía y Medio Ambiente research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Expand your investment toolkit and spot tomorrow’s standout opportunities. There is a world of innovative companies waiting for your attention—don't let these pass you by.

- Supercharge your growth potential with stocks making waves in artificial intelligence. Harness AI penny stocks to uncover future tech leaders.

- Unlock market-beating opportunities by zeroing in on undervalued companies. Let undervalued stocks based on cash flows help you pinpoint hidden gems before others do.

- Turbocharge your income strategy with reliable picks that consistently pay out. Use dividend stocks with yields > 3% to strengthen your portfolio’s earning power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com