Evaluating Fuji (TSE:6134): Is the Stock’s Premium Valuation Warranted After Recent Gains?

Price-to-Earnings of 17.6x: Is it justified?

Based on its price-to-earnings ratio of 17.6x, Fuji is currently trading at a premium compared to the broader Japanese machinery industry. This suggests that the market is placing higher expectations on Fuji’s future earnings compared to its peers.

The price-to-earnings ratio compares a company’s current share price to its per-share earnings and offers a snapshot of how much investors are willing to pay for each unit of profit. In capital goods and machinery sectors, this multiple can reflect both growth expectations and perceived stability.

Currently, Fuji’s multiple exceeds both the industry average and the estimated fair value multiple. This raises questions about whether the market is overvaluing Fuji’s future profitability or pricing in positive developments that are not fully evident from current results.

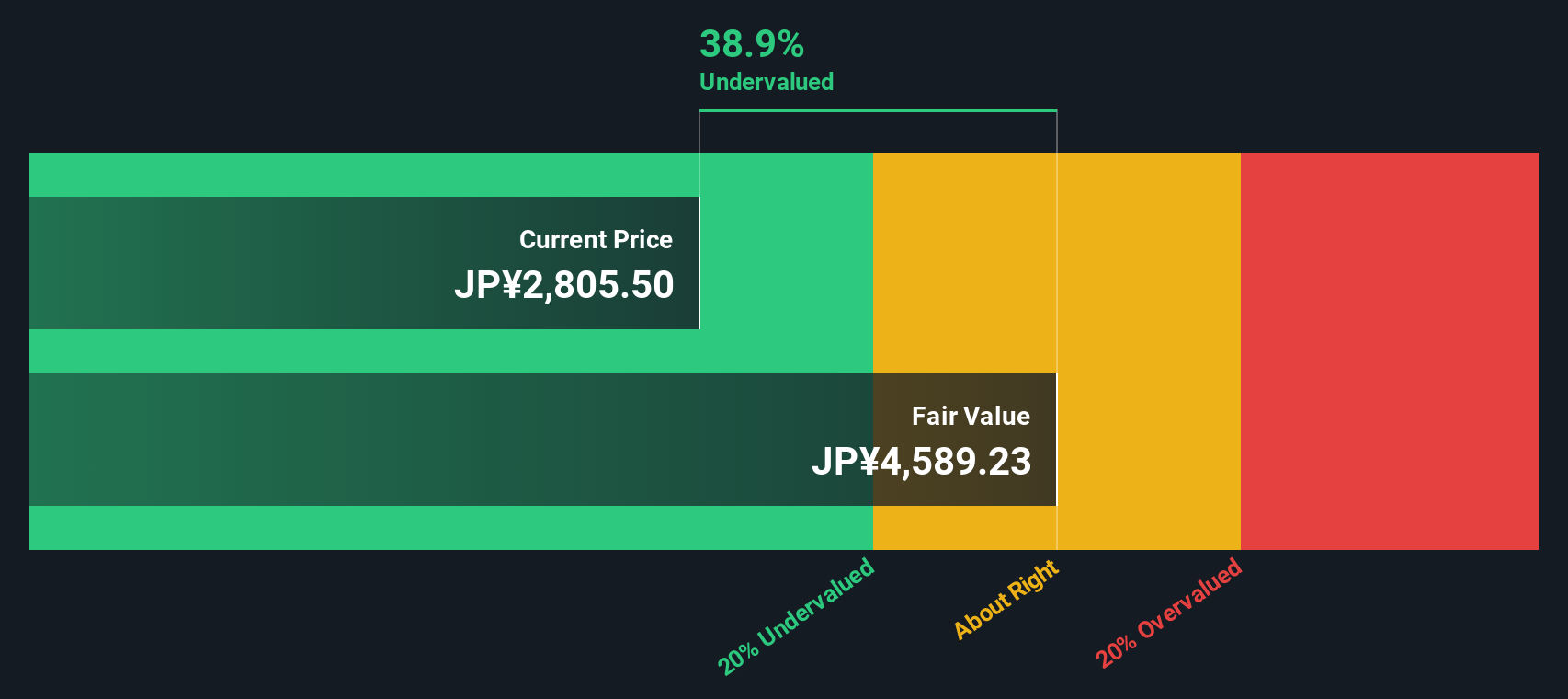

Result: Fair Value of ¥2,796.5 (OVERVALUED)

See our latest analysis for Fuji.However, weaker revenue growth or unexpected earnings shortfalls could quickly challenge the current optimism and put pressure on Fuji's stock valuation.

Find out about the key risks to this Fuji narrative.Another View

Switching to our DCF model, the perspective looks very different. This method points to Fuji being undervalued, which raises doubts about whether the market's current premium is really justified. Which picture reflects reality?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Fuji Narrative

If you see things differently or prefer diving into the numbers yourself, building your own take is just a quick process. Do it your way

A great starting point for your Fuji research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don't miss out on the next wave of market opportunities. Let Simply Wall Street’s powerful Screener lead you to stocks with standout potential and distinct advantages.

- Unlock high-yield potential and secure your portfolio with dividend stocks with yields > 3%. This screener features returns above 3% for those seeking steady income growth.

- Supercharge your watchlist with AI penny stocks. This tool highlights companies pioneering innovations in artificial intelligence and transforming entire industries.

- Seize undervalued opportunities by analyzing undervalued stocks based on cash flows. This option identifies stocks poised for resilience and upside based on strong underlying cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com