ZOZO (TSE:3092): Assessing Current Valuation After Recent Share Price Uptick

ZOZO (TSE:3092) has caught the attention of investors, as its shares showed slight upward movement in the past week after a period of decline. While there is no single trigger event driving the latest activity, the subtle changes in share price may raise eyebrows for those watching the online fashion retailer. This has prompted fresh questions on its future direction and current valuation.

Looking beyond the most recent uptick, ZOZO’s journey through the past year has been a mixed bag. The stock slipped almost 8% in the past twelve months and is down 9% for the year so far. This reflects some cooling from its impressive three- and five-year returns of 54% and 74%, respectively. Short-term momentum has been lackluster, with a small slide over the past month and quarter. All of this paints a picture of a company that has grown over the long haul but is currently seeing more subdued sentiment.

After last year’s dip and early signs of renewed interest, some investors may ask whether the market is underestimating ZOZO’s future growth potential or if its current price already reflects the expectations investors have for the company.

Most Popular Narrative: 3.3% Undervalued

The widely followed narrative currently sees ZOZO as undervalued, with a fair value moderately above its latest share price.

Enhanced data monetization and strong advertising demand, with ad business outperforming expectations, supports greater personalization and new revenue streams. This boosts overall margins and net earnings. Ongoing development and release of proprietary AI-powered services like ZOZOMATCH support consumer demand for personalized experiences. These efforts are likely to improve user engagement, conversion rates, and increase average order value, positively impacting net sales and margins.

Is ZOZO about to leap ahead of the competition? The most watched narrative banks on accelerated profit growth and a bold corporate transformation. What is behind this lofty valuation? You will be surprised by the revenue, margin, and earnings assumptions that anchor the calculation.

Result: Fair Value of ¥1,500 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, setbacks with the LYST integration or a spike in costly promotions could quickly challenge these positive expectations for ZOZO’s future growth.

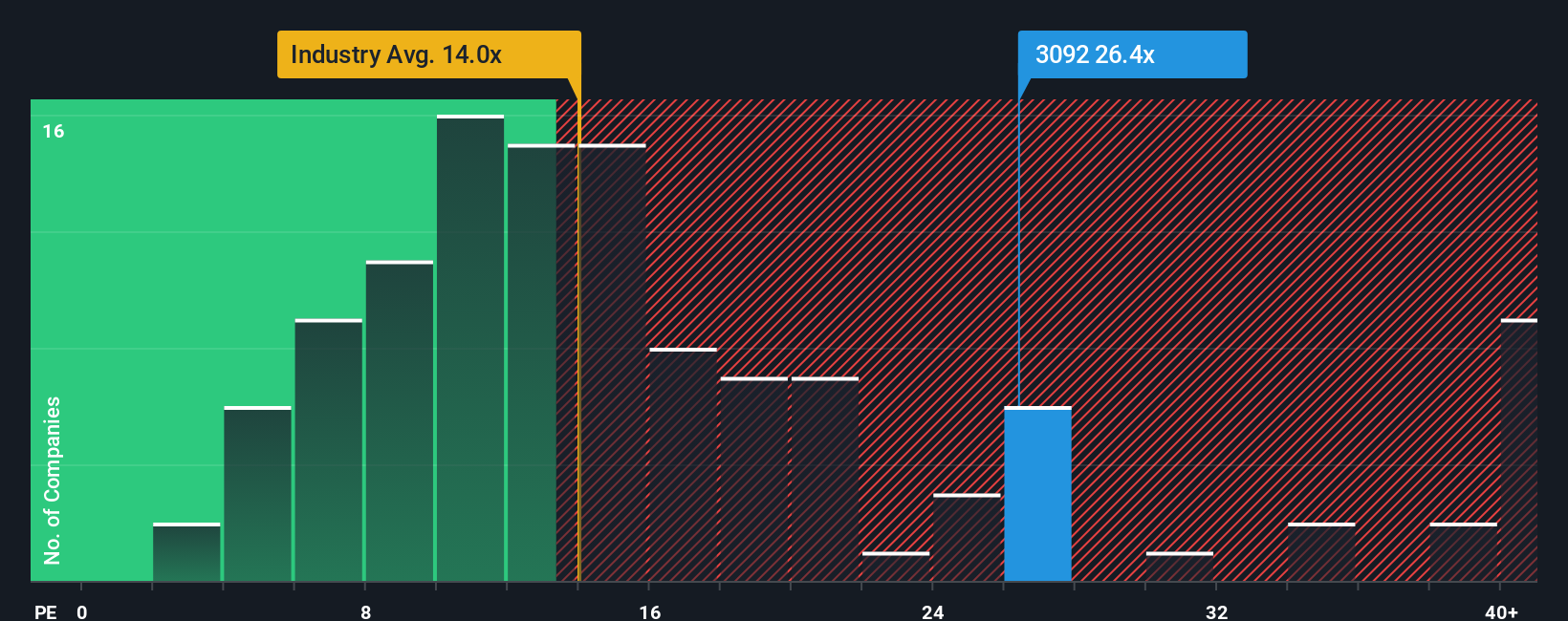

Find out about the key risks to this ZOZO narrative.Another View: Market Multiples Send a Different Signal

While the first approach sees ZOZO as undervalued, a quick look at the company’s valuation against the industry average tells a different story. Based on this measure, ZOZO actually looks expensive compared to its sector peers. Which perspective holds the key?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own ZOZO Narrative

If you want to dig deeper or reach your own conclusions, you can build your own narrative using our data in just a few minutes. Do it your way.

A great starting point for your ZOZO research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Why stop at ZOZO? There are standout companies with unique strengths waiting for you. Use these fresh ideas now, or you may miss tomorrow's movers.

- Accelerate your gains with tech innovators by tapping into AI penny stocks to spot up-and-coming leaders in artificial intelligence.

- Secure your portfolio’s income by checking out dividend stocks with yields > 3% to find stocks offering robust yields that strengthen your returns each year.

- Tap into unrealized bargains by browsing undervalued stocks based on cash flows to uncover companies trading at prices the market has not caught up to yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com