A Closer Look at MITSUI-SOKO HOLDINGS (TSE:9302) Valuation Following Recent Share Price Volatility

For investors eyeing MITSUI-SOKO HOLDINGS (TSE:9302), recent moves in the share price may have prompted some double takes. While there hasn’t been a dramatic event making headlines, this level of activity is often enough to get people wondering whether the current price signals something deeper about the company’s outlook. Anytime a stock shows meaningful movement without a big headline, smart investors naturally look for what the market might be missing or anticipating.

Looking at the bigger picture, MITSUI-SOKO HOLDINGS has experienced a striking run this year, with the stock up well over 100% on a total return basis. There have been brief setbacks, including a modest slip this month, but momentum appears very much intact overall. When you zoom out further, the three- and five-year returns stand out as significant outperformance, helped along by recent positive trends in both revenue and net income growth.

With all that in mind, investors have to ask: are we looking at an undervalued opportunity, or has the market already captured future growth in today’s price?

Price-to-Earnings of 30.7x: Is it justified?

The latest valuation draws on the price-to-earnings (P/E) ratio, which stands at 30.7x for MITSUI-SOKO HOLDINGS. This figure places the company well above both the Japan Logistics industry average of 16.3x and the peer average of 18.1x. This signals that investors are paying a steep premium for its shares.

The P/E ratio compares a company’s current share price to its per-share earnings. In the logistics sector, this multiple is often used as a yardstick for how much investors are willing to pay for each unit of profit, relative to competitors or the broader industry. A high P/E can reflect expectations of future growth, strong market positioning, or superior earnings quality. However, it can also point to overvaluation if growth does not ultimately justify the premium.

Given that MITSUI-SOKO HOLDINGS’ P/E ratio is significantly above its industry and peer averages, the market appears to be pricing in robust future performance or assigning extra value to its business model. However, with earnings growth rates that are not dramatically outpacing the sector, investors should be cautious about whether such a high multiple is warranted.

Result: Fair Value of ¥4,332.12 (ABOUT RIGHT)

See our latest analysis for MITSUI-SOKO HOLDINGS.However, slowing revenue growth or a reversal in net income trends could quickly challenge the optimism surrounding MITSUI-SOKO HOLDINGS’ recent valuation premium.

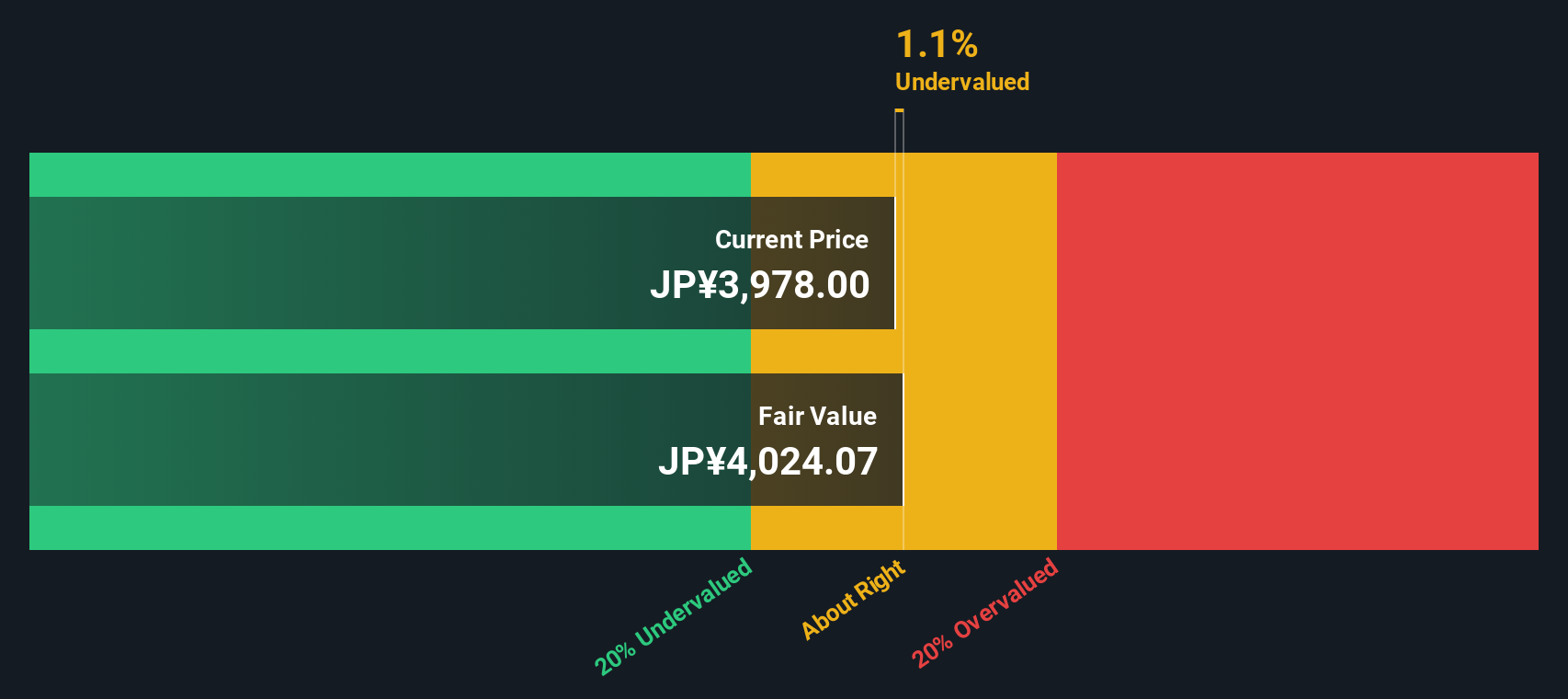

Find out about the key risks to this MITSUI-SOKO HOLDINGS narrative.Another View: What Does the DCF Say?

While the market seems to be factoring in a premium based on earnings multiples, our DCF model paints a slightly different story. This approach suggests the current share price may not fully reflect intrinsic value. Which method offers the truest signal?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own MITSUI-SOKO HOLDINGS Narrative

If you see things differently, or would rather dive into the numbers yourself, you can develop your own perspective on MITSUI-SOKO HOLDINGS in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding MITSUI-SOKO HOLDINGS.

Looking for more investment ideas?

Smart investors know that exciting opportunities don’t end with one company. The Simply Wall Street Screener can help you act fast and spot what others might miss.

- Tap into the future of finance by tracking established players making waves in digital currencies and blockchain innovation with cryptocurrency and blockchain stocks.

- Maximize your income strategy as you target stocks offering generous yields above 3 percent with dividend stocks with yields > 3%.

- Find tomorrow’s market standouts by zeroing in on shares trading below their estimated value using undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com