A Look at Lovesac's Valuation After Debuting Snugg Collection and Reporting Latest Earnings

Lovesac (LOVE) just made its biggest splash yet with the debut of Snugg, its first-ever couch and loveseat collection, bolstered by a head-turning marketing campaign featuring actress Brittany Snow. With this move, the company is not just upgrading its product line; it is making a bold play for a larger piece of the living room, and potentially a new tier of customers. Pair this with the latest earnings report, which showed a 2.5% uptick in net sales but a wider loss due to higher costs, and investors are taking notice as they try to determine what these changes mean for the stock’s future.

Looking at the bigger picture, Lovesac’s year has been a story of ups and downs. Shares are down nearly 33% over the past year, extending a multi-year slide despite some recent operational wins and a brand refresh with the launch of Snugg. In the past three months, there has been a modest recovery, but momentum remains mixed, shaped by new product launches, digital investments, and the ripple effects of this summer’s data breach incident. While management is sticking to its long-term growth plans, the market appears cautious, possibly waiting to see if Snugg and other innovations can reignite sales and profits over time.

After a period of declining share prices and bold company moves, is Lovesac now trading at a bargain, or is the market already factoring in most of that potential upside?

Most Popular Narrative: 41.5% Undervalued

The most widely followed narrative sees Lovesac as significantly undervalued, with its fair value estimate sitting well above the current market price. This perspective is shaped by expectations of robust future earnings and margin improvements driven by new products and operational strengths.

Lovesac's sustained innovation and frequent new product launches, such as the EverCouch and Reclining Seat, are expected to significantly expand its total addressable market and drive revenue growth. The company's strong supply chain management, including the diversification of sourcing locations and redundancy for key products, is likely to ensure stable production and potentially improve net margins by managing costs effectively.

What secrets fuel such a dramatic valuation gap? From market-shaping product launches to ambitious profit targets, the narrative is built on bold projections and aggressive financial assumptions. Curious how revenue jumps, margin shifts, and innovative strategies might push this stock higher? Uncover which factors make this valuation one of the most intriguing stories in the sector right now.

Result: Fair Value of $30.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent macro pressures and mounting competition could easily derail these bullish projections, especially if consumer demand falters or if margins contract.

Find out about the key risks to this Lovesac narrative.Another View: Not All Signs Point to a Bargain

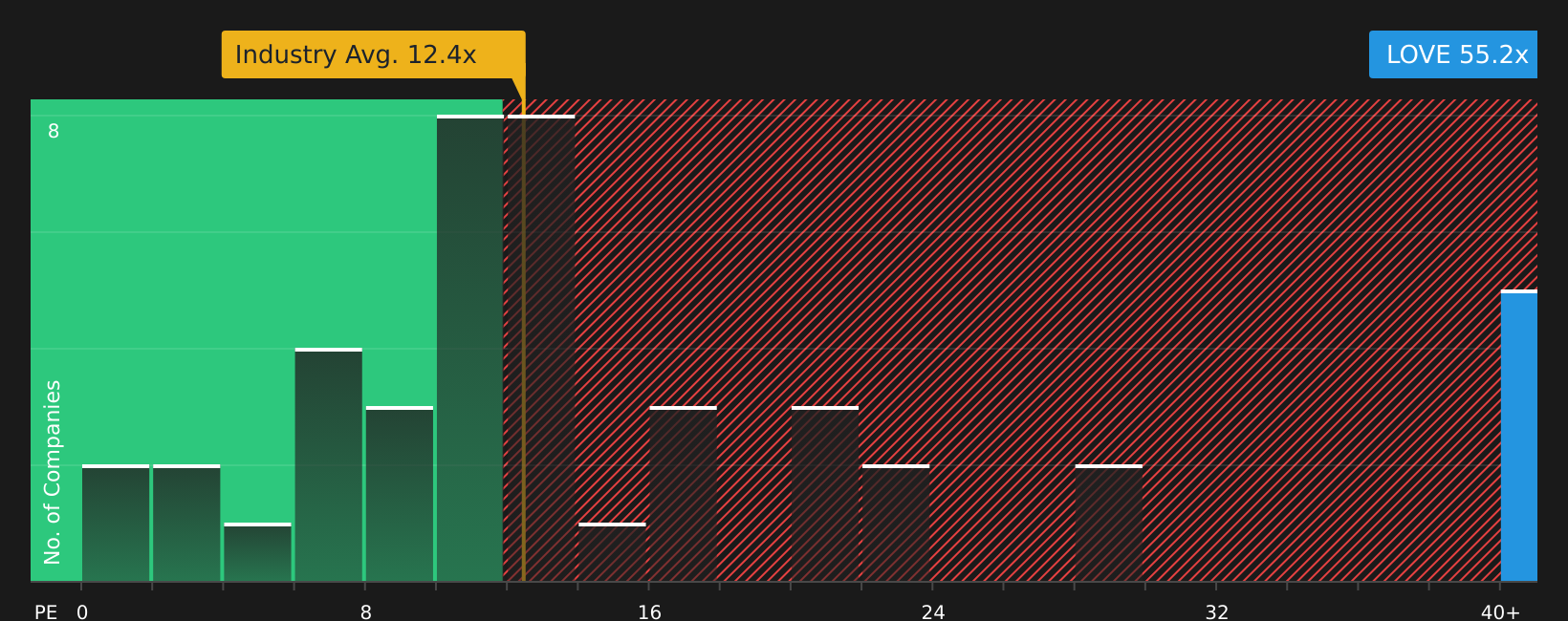

Taking a different approach, a comparison to the industry’s valuation shows that Lovesac trades at a higher price relative to its earnings than other Consumer Durables stocks. This clouds the undervalued case. Could the premium be justified?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Lovesac Narrative

If these perspectives are not quite your style or you want to dive into the data firsthand, you can easily assemble your own narrative in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Lovesac.

Looking for more investment ideas?

Don’t settle for just one opportunity. Put yourself in front of the market’s next big winners by checking out fresh stock ideas with huge potential.

- Catch high-yield opportunities and see which companies are rewarding shareholders with impressive income using the dividend stocks with yields > 3% filter.

- Spot breakthrough innovators who are poised to shape the future of healthcare by exploring companies at the forefront of medicine powered by healthcare AI stocks advancements.

- Fuel your portfolio with stocks that appear undervalued based on real cash flows by tapping into our powerful undervalued stocks based on cash flows engine.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com