Assessing the Value of Kraft Heinz After Recent Stock Slide in 2025

If you have been wrestling with whether to hang on to Kraft Heinz or add some to your portfolio, you are not alone. It is one of those names that rarely sits quietly in the pantry of the stock market. The Kraft Heinz share price has seen some bumps lately, down 4.3% over the last week and off 6.7% this past month. Stretch that further and you will see a year-to-date drop of 15.1%, and if you look over the last year, it’s a slide of 22.4%. Long-term holders have fared a bit better: up 10.4% over five years, even if the last three have been negative.

Some of this turbulence has echoed in the wider market, where defensive names like Kraft Heinz sometimes lose steam when higher-yielding assets catch investors' attention, especially in an environment shifting its perception of risk. Despite the red ink lately, there is a whisper among value investors that Kraft Heinz might be oversold right now. Why? Because when you line up conventional valuation metrics, the stock is showing flashes of opportunity. Out of six major valuation checks, Kraft Heinz passes four, giving it a value score of 4.

But what do those checks really mean? In the next section, I will break down what methods go into this kind of score and walk you through what they say about Kraft Heinz today. And just between us, there is an even more insightful way to look at valuation coming later in the article, so stay tuned.

Why Kraft Heinz is lagging behind its peersApproach 1: Kraft Heinz Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model projects a company’s future cash flows and discounts these back to a present-day value. This helps estimate what the business is intrinsically worth right now based on its ability to generate cash in the years ahead.

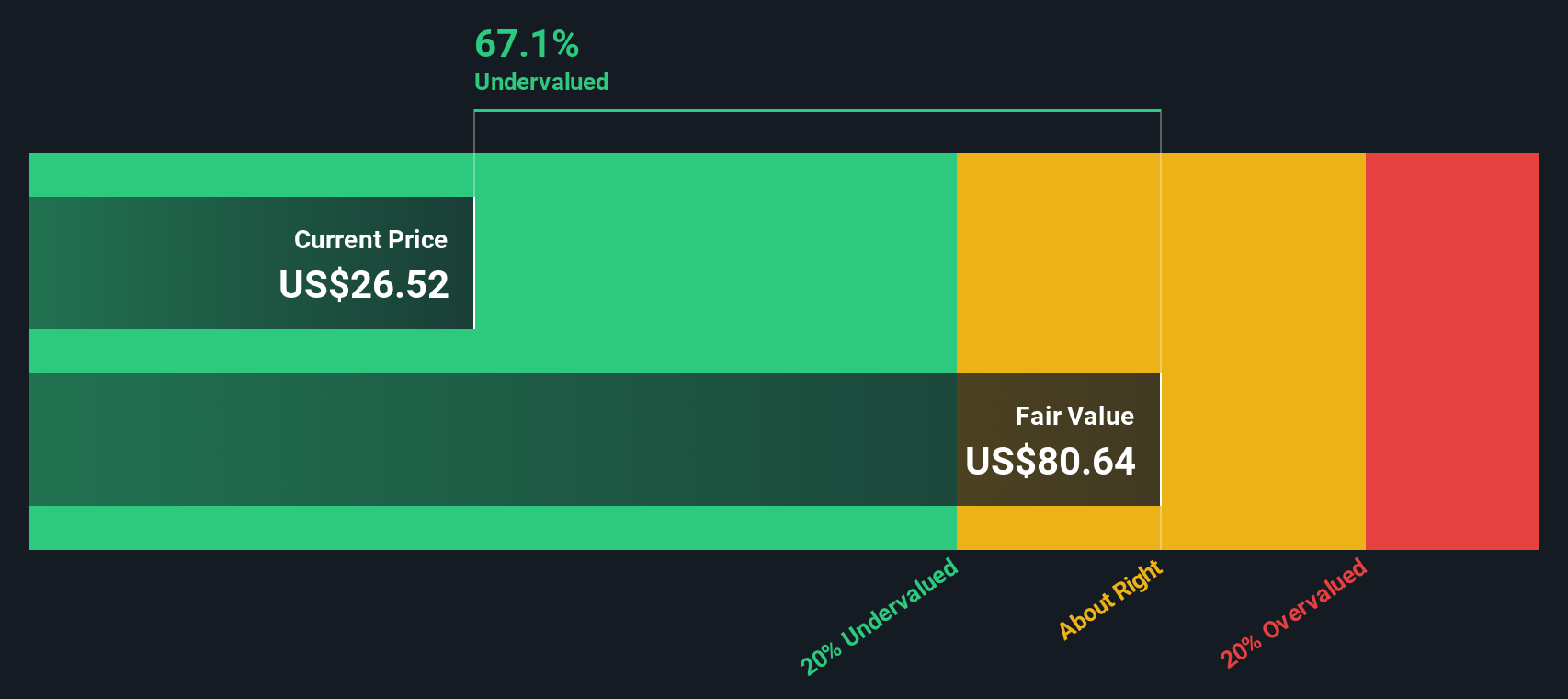

For Kraft Heinz, the latest available Free Cash Flow sits at $3.45 Billion, with forecasts showing a steady increase. Analyst consensus covers the next few years and projects a Free Cash Flow of $3.78 Billion by 2028. Projections beyond this use trend-based estimates, suggesting further modest growth through 2035. All figures are reported in US dollars.

Using the 2 Stage Free Cash Flow to Equity model, the calculated intrinsic value for Kraft Heinz is $80.64 per share. Given that the current share price is significantly lower, this suggests the stock is trading at a 67.6% discount to its DCF-implied fair value. In other words, the intrinsic value signals significant undervaluation compared to where it trades today.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Kraft Heinz.

Approach 2: Kraft Heinz Price vs Sales

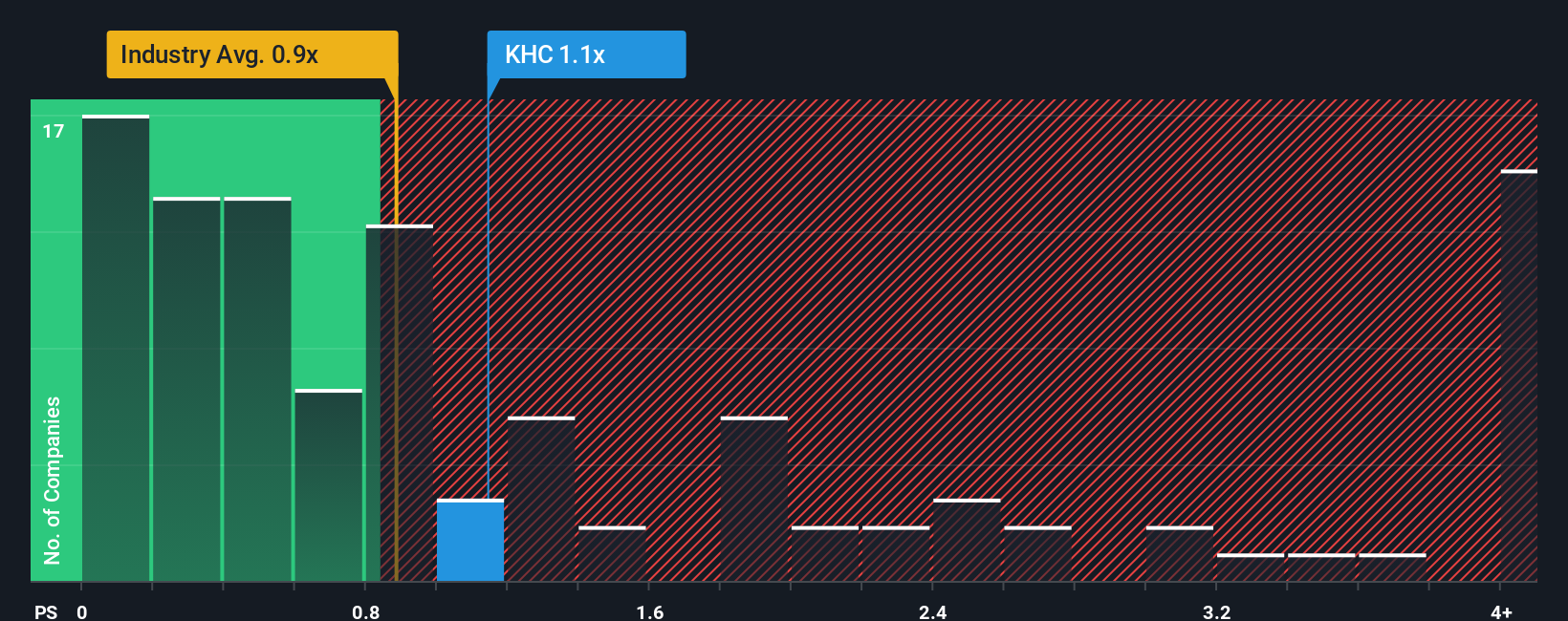

The Price-to-Sales (P/S) ratio is one of the most effective metrics for valuing established consumer staples companies like Kraft Heinz, particularly when earnings may be less reliable due to one-off charges or accounting factors. For companies with stable revenues, the P/S ratio gives investors a straightforward look at how much the market is willing to pay for each dollar of sales.

The "right" P/S multiple for a company can shift depending on expected revenue growth, the perceived stability of future sales, and how risky the business environment is for that sector. A higher growth prospect or stronger competitive advantage typically justifies a higher ratio; higher risk or sluggish sales demand a lower one instead.

Currently, Kraft Heinz trades at a P/S ratio of 1.22x. That is lower than the Food industry average of 0.86x, but also lags behind its peer group average of 1.81x. However, matching a company solely against peers or the industry can miss the mark. This is why Simply Wall St's proprietary "Fair Ratio" model steps in. This figure, 1.55x for Kraft Heinz, is custom-calculated to reflect unique factors like its market cap, profit margins, growth outlook, and risk profile rather than just broad averages.

Comparing the current P/S ratio (1.22x) to the Fair Ratio (1.55x), Kraft Heinz appears undervalued on this metric, suggesting the market may be overlooking value within its financial fundamentals.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your Kraft Heinz Narrative

Earlier, we mentioned there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is your personal story and perspective about a company, combining your assumptions and expectations about Kraft Heinz’s future, such as revenue, profit margins, and risks, into a financial forecast that leads directly to a fair value estimate.

Narratives bridge the gap between the numbers and the reasoning behind them, aligning a company’s unique story with its outlook and price. On Simply Wall St’s Community page, millions of investors use Narratives as an easy and accessible tool to build their own view of fair value, see how it compares to the current price, and decide whether the stock looks like a buy, hold, or sell.

What sets Narratives apart is how dynamic and up-to-date they are. When news breaks or earnings reports are released, assumptions and valuations update automatically, helping you quickly test your view against changing facts in real time.

For Kraft Heinz, you can see this in action. Some investors, optimistic about global expansion and innovation, forecast a future value as high as $51 per share. More cautious voices, wary of sluggish growth or execution risk, see a fair value nearer $27. Narratives let you explore exactly why investors reach these different conclusions so your investment decision is always rooted in both data and your personal conviction.

Do you think there's more to the story for Kraft Heinz? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com