Sable Offshore (SOC): Assessing Valuation After Lawsuits and Regulatory Setbacks Shake Investor Confidence

Sable Offshore (NYSE:SOC) investors have had plenty to process after a recent wave of class action lawsuits landed against the company. At the core of the legal storm are allegations that Sable Offshore and its leadership misled the market about restarting oil production off the California coast. Regulatory officials quickly challenged these claims, and a court stepped in with injunctions that restrict crucial pipeline activity. For investors deciding what to do with SOC shares, these events bring new risks and uncertainties to the surface.

Unsurprisingly, these developments have shaken market confidence. Over the past month, Sable Offshore’s share price has dropped more than 30%, deepening a year-to-date decline. The last year has seen modest losses, but the backdrop is more complex. Long-term shareholders are still sitting on strong gains from the stock’s three-year climb, while regulatory and legal setbacks have taken the near-term spotlight. This tension between past momentum and current headwinds is now shaping the conversation about value and risk.

So, after a difficult stretch and renewed market anxiety, is Sable Offshore presenting a rare value opportunity, or is the market correctly pricing in further fallout from these legal battles and regulatory challenges?

Price-to-Book of 4.5x: Is it justified?

Based on its price-to-book (P/B) ratio, Sable Offshore currently appears expensive relative to both its industry and peer group, signaling overvaluation through this lens.

The price-to-book ratio measures how much investors are paying for each dollar of a company’s net assets. In the oil and gas sector, this metric is widely used because asset values can be significant, and profitability may fluctuate from year to year.

Sable Offshore trades at 4.5 times its book value. This is notably higher than the US oil and gas industry average of 1.3x and the peer average of 1.5x. This premium suggests that the market is either anticipating significant asset growth or rewarding Sable Offshore for factors not yet reflected on its balance sheet. Given that the company is currently unprofitable, this high valuation multiple may raise questions about whether investor optimism is justified by fundamentals.

Result: Fair Value of $20.06 (OVERVALUED)

See our latest analysis for Sable Offshore.However, ongoing legal uncertainties and recent regulatory interventions could continue to weigh on investor sentiment, which may challenge any near-term rebound for Sable Offshore.

Find out about the key risks to this Sable Offshore narrative.Another View: Discounted Cash Flow Model

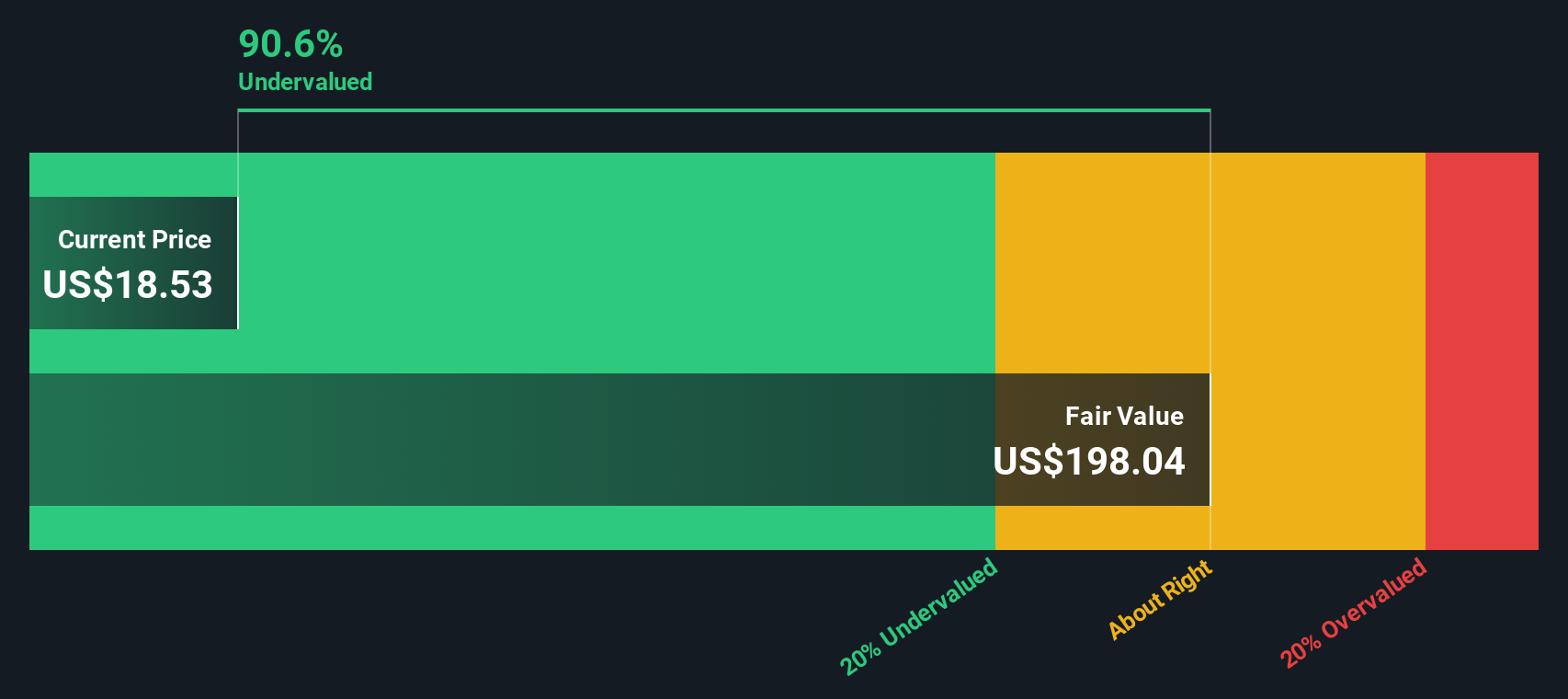

Looking at Sable Offshore from the perspective of our DCF model tells a very different story. This method suggests the shares may be deeply undervalued, which is in stark contrast to the signals from the price-to-book ratio. Which approach will prove more accurate?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Sable Offshore Narrative

If you see the situation differently or want to reach your own conclusions, you can build a personalized analysis in just a few minutes. Do it your way.

A great starting point for your Sable Offshore research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Why stop here? Give yourself an edge by checking out unique stock selections handpicked by expert filters. Don't let better opportunities slip by—your next great find could be just a click away.

- Spot emerging opportunities in technology by checking out the latest advancements through quantum computing stocks.

- Boost your long-term growth prospects with companies leading the way in game-changing artificial intelligence. Start now with AI penny stocks.

- Maximize your earning power with shares offering robust yields. Start hunting for reliable payouts at dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com