Is Namura Shipbuilding (TSE:7014) Undervalued? A Fresh Look at Its Recent Valuation

If you’ve been tracking Namura Shipbuilding (TSE:7014) lately, you might have found yourself pausing at the latest movements in its share price. There hasn’t been a major news event or company announcement causing waves. Sometimes, it’s these steady periods that prompt investors to question whether the current valuation hints at something beneath the surface. Could the recent uneventful stretch be masking a new phase for the stock, or is it simply a pause before the next big move?

Over the past year, Namura Shipbuilding’s performance has been anything but quiet. The stock has delivered a gain of over 130% in that period, with momentum especially strong year-to-date at more than 65%. After some cooling in the past month, shares have held onto significant long-term growth, and recent weeks have seen only modest fluctuations. These shifts come after several years of powerful returns, paired with underlying improvements in annual revenue and net income growth.

Given all this, is Namura Shipbuilding’s current level reflecting an undervalued opportunity for investors, or is the market already factoring in the company’s future prospects?

Price-to-Earnings of 10.4x: Is it justified?

Based on the price-to-earnings (P/E) ratio of 10.4x, Namura Shipbuilding appears undervalued compared to both its industry peers and the broader sector average. The company's current P/E ratio is significantly lower than the peer average of 30.3x and also below the JP Machinery industry average of 13.4x. This could indicate potential attractive value for investors.

The P/E ratio measures how much investors are willing to pay for a yen of earnings. For a company like Namura Shipbuilding, it provides insight into market expectations about future profitability and growth. In capital goods and heavy industry, where earnings can be cyclical, a lower P/E may indicate either undervaluation or an expectation of volatile results ahead.

With Namura Shipbuilding’s strong share performance and improved profitability over recent years, the market might be underestimating the company’s earnings potential based on its modest multiple. If the business continues delivering steady revenue and profit growth, the P/E ratio could be seen as justified or even conservative.

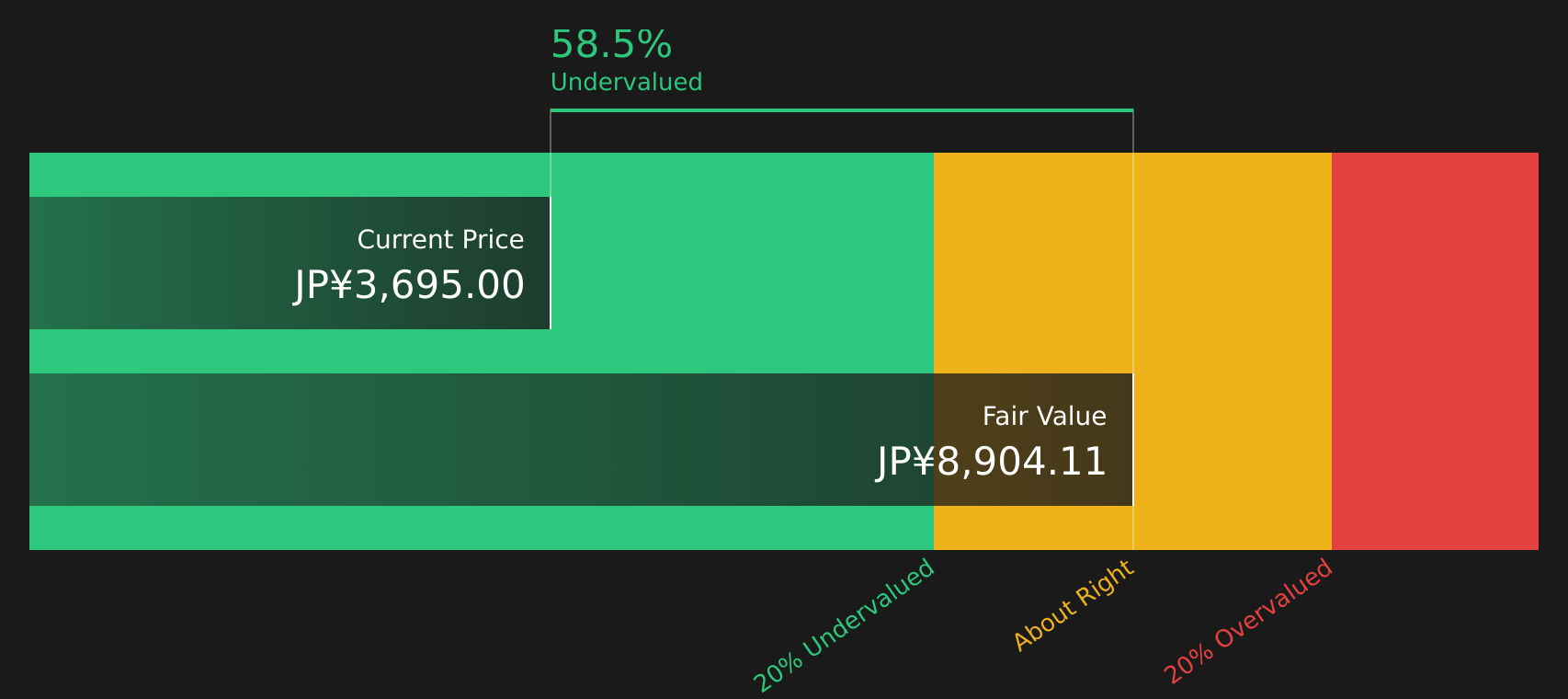

Result: Fair Value of ¥9475.16 (UNDERVALUED)

See our latest analysis for Namura Shipbuilding.However, sustained earnings growth is not guaranteed. Any downturn in global shipbuilding demand or industry price pressures could quickly alter the outlook.

Find out about the key risks to this Namura Shipbuilding narrative.Another View: What Does the SWS DCF Model Say?

To look from a different angle, our DCF model also points to Namura Shipbuilding being undervalued by the market. Both methods suggest opportunity. However, can such models fully capture the shifts in this industry?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Namura Shipbuilding Narrative

If you see things differently or like to form your own conclusions from the data, you can put together your own view in minutes. Do it your way.

A great starting point for your Namura Shipbuilding research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let great opportunities slip by. Arm yourself with smarter choices and deeper insights using Simply Wall Street’s powerful investing tools. Check out these dynamic stock themes you can act on today:

- Stay ahead of the curve and seek out market movers with AI penny stocks, blending artificial intelligence and innovation for growth-focused investors.

- Secure your portfolio’s future income by tapping into dividend stocks with yields > 3%, featuring companies offering attractive yields above 3%, helping you build steady returns.

- Unearth potential gems flying below the radar with penny stocks with strong financials, backed by solid financials and robust fundamentals rarely found in lower-priced stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com