Jefferies Financial Group (JEF): Assessing Valuation After New Bond Issuances and Focused Balance Sheet Moves

Jefferies Financial Group raised eyebrows this week after announcing a pair of fixed-income offerings, issuing new senior unsecured notes set to mature in 2035 and 2045. This move injects over $10 million in fresh capital into its balance sheet and is aimed at boosting operational flexibility during a period when US capital markets have been anything but smooth. While some investors might view these offerings as a prudent way to shore up funding, others are watching closely to see if they signal management’s caution about the growth outlook.

The newly issued bonds come as Jefferies Financial Group continues to navigate mixed conditions in financial markets. Over the past year, the stock rewarded shareholders with a solid 17% total return, continuing a strong three-year momentum that stands well above industry averages. However, year-to-date returns tell a more muted story, down nearly 19% as markets re-evaluate earnings growth and the company’s more measured approach to risk and leverage.

After last year’s gains and this year’s shift in sentiment, is the current price undervaluing Jefferies’ ability to adapt, or is the market a step ahead, already pricing in everything?

Price-to-Earnings of 22.9x: Is it justified?

Jefferies Financial Group currently trades at a price-to-earnings (P/E) ratio of 22.9, which is below the US Capital Markets industry average of 26.7. This suggests that the stock may offer relatively better value compared to its industry peers on this metric, even though its absolute valuation remains on the higher side.

The P/E ratio is a widely followed valuation measure in capital markets. It compares a company’s share price to its earnings per share, offering insights into how much investors are willing to pay for each dollar of profit. For diversified financial firms like Jefferies, the P/E ratio can reflect not only current profitability but also expectations for future earnings growth and stability.

While Jefferies trades at a discount to the industry average, its valuation is in line with the peer group average. This indicates that the market is pricing in its earnings outlook and risk profile in a manner consistent with comparable firms. Investors appear neither overly bullish nor bearish on Jefferies’ long-term earnings capacity, but rather view it as appropriately valued given industry and peer context.

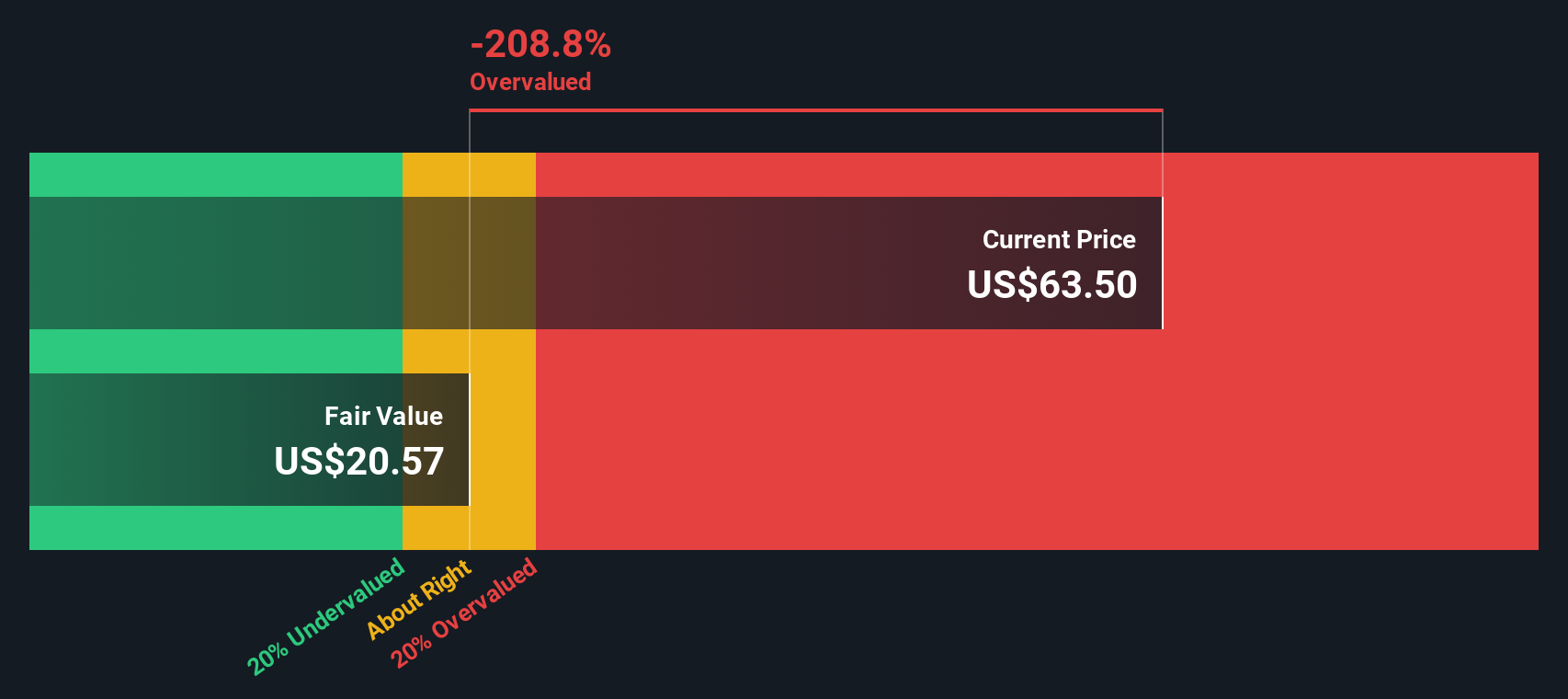

Result: Fair Value of $64.29 (ABOUT RIGHT)

See our latest analysis for Jefferies Financial Group.However, Jefferies faces risks from uneven revenue growth and recent volatility. Both of these factors could challenge its current valuation if market sentiment turns.

Find out about the key risks to this Jefferies Financial Group narrative.Another View: Our DCF Model Suggests a Different Story

While the market’s valuation looks reasonable on earnings, our DCF model points in the opposite direction and indicates that Jefferies is trading above what its future cash flows are worth. Can both perspectives be right, or is something missing from the market’s view?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Jefferies Financial Group Narrative

If you have a different perspective or want to review the numbers first-hand, you can quickly craft your own view in just a few minutes. Do it your way

A great starting point for your Jefferies Financial Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Plenty of compelling opportunities are just a click away. Put yourself ahead of the curve and spot trends before they hit the mainstream. Don’t let your next big win slip by.

- Uncover fast-moving potential by targeting penny stocks with strong fundamentals in penny stocks with strong financials and see where under-the-radar growth may be waiting.

- Gain an edge in the future of medicine by seeking out breakthroughs and promising prospects in healthcare AI stocks that are reshaping healthcare with artificial intelligence.

- Tap into attractive yield by filtering for dividend stocks with yields > 3% and highlight companies rewarding investors with robust dividend payments above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com