3 UK Stocks That May Be Priced Below Their Intrinsic Value Estimates

As the United Kingdom's FTSE 100 index grapples with challenges stemming from weak trade data out of China and fluctuating commodity prices, investors are keenly observing market movements for potential opportunities. In such a climate, identifying stocks that may be priced below their intrinsic value can offer a strategic advantage, as these investments have the potential to provide solid returns when market conditions stabilize.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Vistry Group (LSE:VTY) | £6.038 | £11.46 | 47.3% |

| PageGroup (LSE:PAGE) | £2.304 | £4.61 | 50% |

| Mitie Group (LSE:MTO) | £1.40 | £2.64 | 47% |

| Mincon Group (AIM:MCON) | £0.41 | £0.78 | 47.3% |

| LSL Property Services (LSE:LSL) | £2.86 | £5.67 | 49.6% |

| Hollywood Bowl Group (LSE:BOWL) | £2.455 | £4.78 | 48.7% |

| Gooch & Housego (AIM:GHH) | £5.40 | £10.77 | 49.9% |

| Gateley (Holdings) (AIM:GTLY) | £1.325 | £2.58 | 48.7% |

| Begbies Traynor Group (AIM:BEG) | £1.17 | £2.22 | 47.3% |

| AstraZeneca (LSE:AZN) | £119.76 | £224.09 | 46.6% |

Let's take a closer look at a couple of our picks from the screened companies.

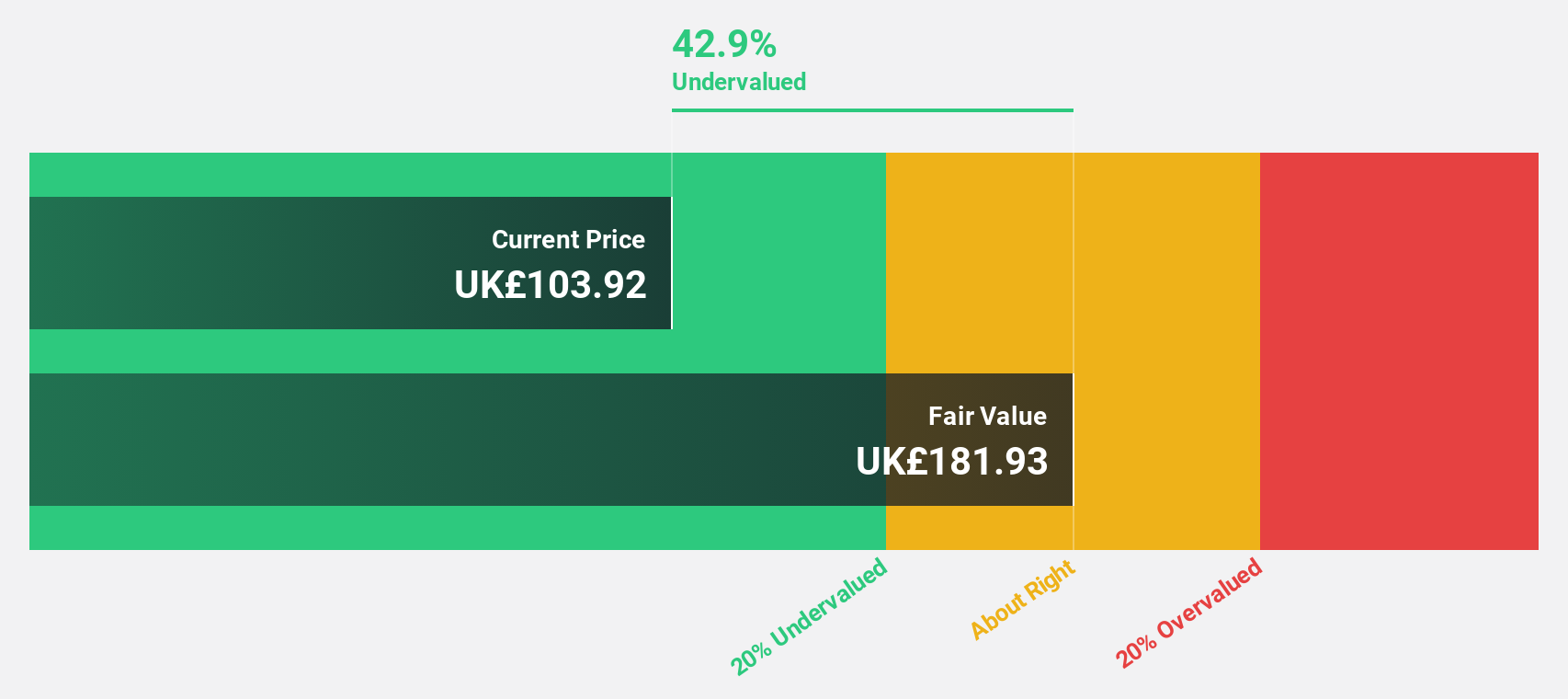

AstraZeneca (LSE:AZN)

Overview: AstraZeneca PLC is a biopharmaceutical company engaged in the discovery, development, manufacture, and commercialization of prescription medicines, with a market cap of approximately £185.71 billion.

Operations: The company generates revenue of $56.50 billion from its pharmaceuticals segment.

Estimated Discount To Fair Value: 46.6%

AstraZeneca appears undervalued based on cash flow analysis, trading at £119.76 compared to an estimated fair value of £224.09. Despite high debt levels and significant insider selling recently, the company shows strong earnings growth potential with a forecasted 14.7% annual increase, outpacing the UK market average of 13.8%. Recent positive trial results for TAGRISSO in lung cancer treatment could further enhance its financial outlook and support its valuation recovery.

- In light of our recent growth report, it seems possible that AstraZeneca's financial performance will exceed current levels.

- Get an in-depth perspective on AstraZeneca's balance sheet by reading our health report here.

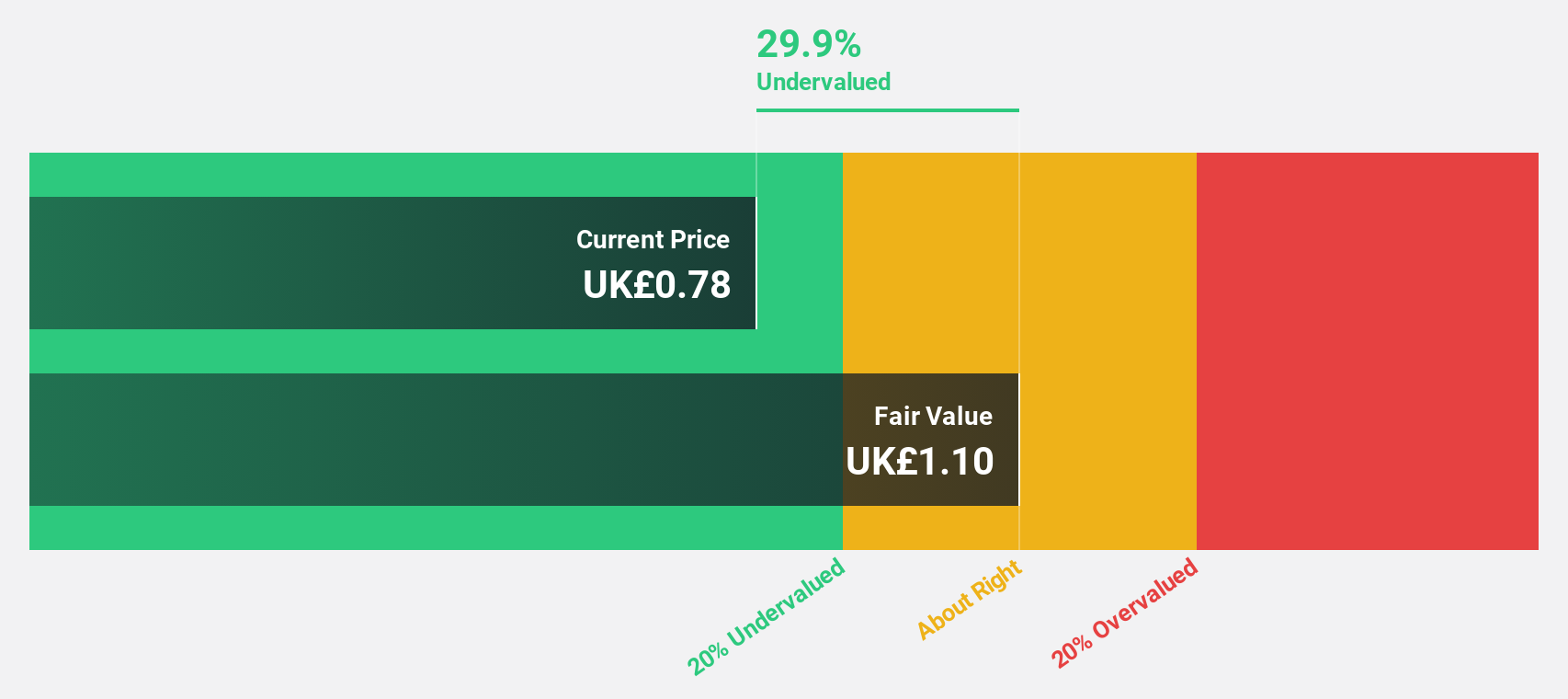

Coats Group (LSE:COA)

Overview: Coats Group plc, with a market cap of £1.54 billion, operates globally in thread manufacturing, structural components for apparel and footwear, and performance materials.

Operations: The company's revenue segments consist of $775.30 million from apparel, $405.20 million from footwear, and $321.80 million from performance materials.

Estimated Discount To Fair Value: 38.3%

Coats Group is trading at £0.8, significantly below its estimated fair value of £1.3, indicating potential undervaluation based on cash flows. Despite recent shareholder dilution through a £250.5 million follow-on equity offering, earnings are forecasted to grow substantially at 29.3% annually, outpacing the UK market's growth rate. However, the dividend yield of 2.94% is not well-covered by free cash flows and debt coverage by operating cash flow remains a concern for investors seeking stability.

- Our earnings growth report unveils the potential for significant increases in Coats Group's future results.

- Click to explore a detailed breakdown of our findings in Coats Group's balance sheet health report.

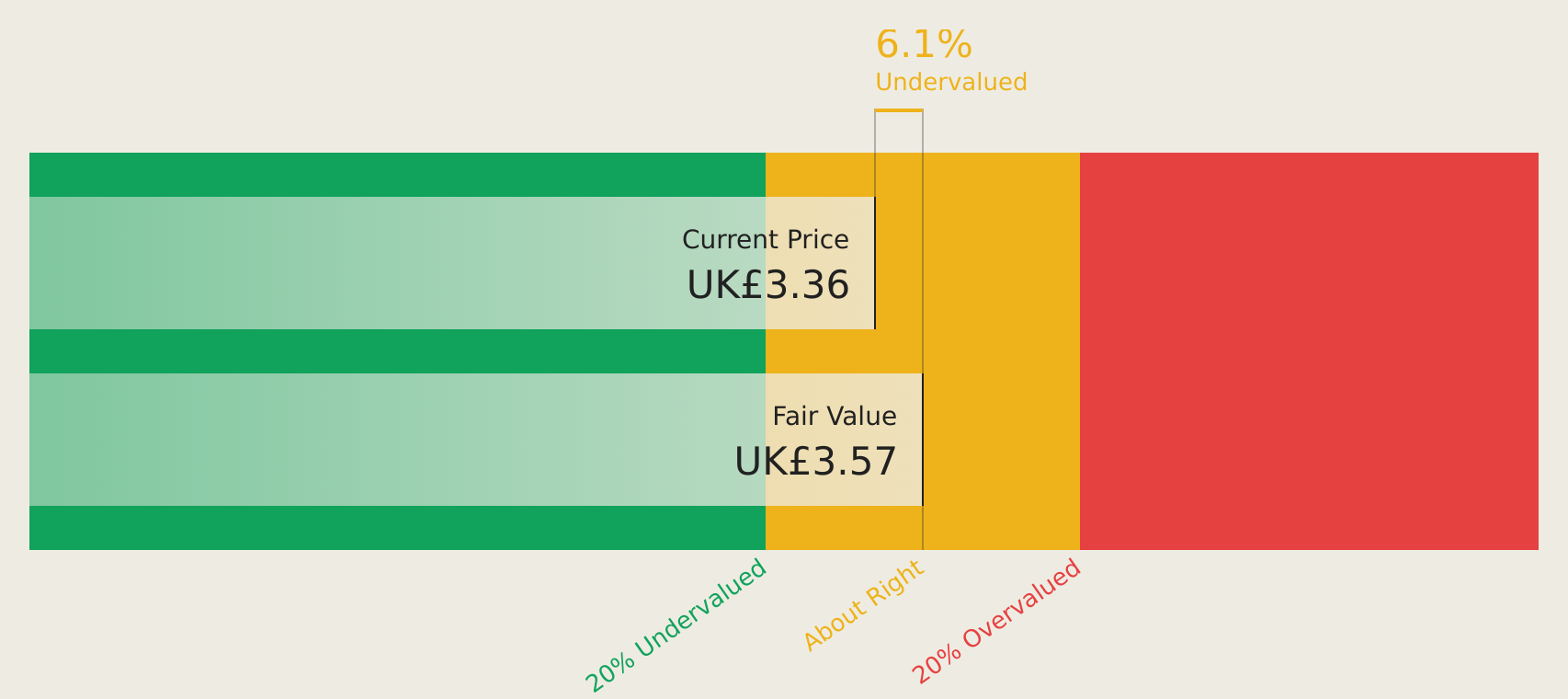

Rotork (LSE:ROR)

Overview: Rotork plc designs, manufactures, and markets industrial flow control and instrumentation solutions for various sectors including oil and gas, water and wastewater, power, chemical process, and industrial markets with a market cap of £2.89 billion.

Operations: The company generates revenue from several segments: £354.91 million from Oil & Gas, £199.89 million from Water & Power, and £205.53 million from Chemical, Process & Industrial sectors.

Estimated Discount To Fair Value: 17.8%

Rotork, trading at £3.47, is below its estimated fair value of £4.22, suggesting undervaluation based on cash flows. Despite a slight decline in net income to £47.7 million for H1 2025 compared to last year, earnings are expected to grow at 15.8% annually, outpacing the UK market's growth rate of 13.8%. The recent interim dividend increase by 7.3% reflects management's confidence despite an unstable dividend track record and slower revenue growth forecast at 5.2% per year.

- Our expertly prepared growth report on Rotork implies its future financial outlook may be stronger than recent results.

- Delve into the full analysis health report here for a deeper understanding of Rotork.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 45 Undervalued UK Stocks Based On Cash Flows now.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com