Sunac (SEHK:1918): Evaluating Whether Its Recent Rebound Reflects True Value

Price-to-Sales of 0.3x: Is it justified?

Sunac China Holdings is currently trading at a price-to-sales ratio of 0.3x, which is considered good value compared to both its peer group and the wider Hong Kong Real Estate industry average of 0.7x.

The price-to-sales ratio measures how much investors are paying for each dollar of the company's revenue. This metric is especially relevant for evaluating companies where earnings may be volatile or negative, as is currently the case for Sunac.

This suggests the market is significantly discounting Sunac’s shares relative to its revenue base. This may reflect concerns over ongoing losses and future growth prospects, but it could also indicate room for a re-rating if fundamentals improve.

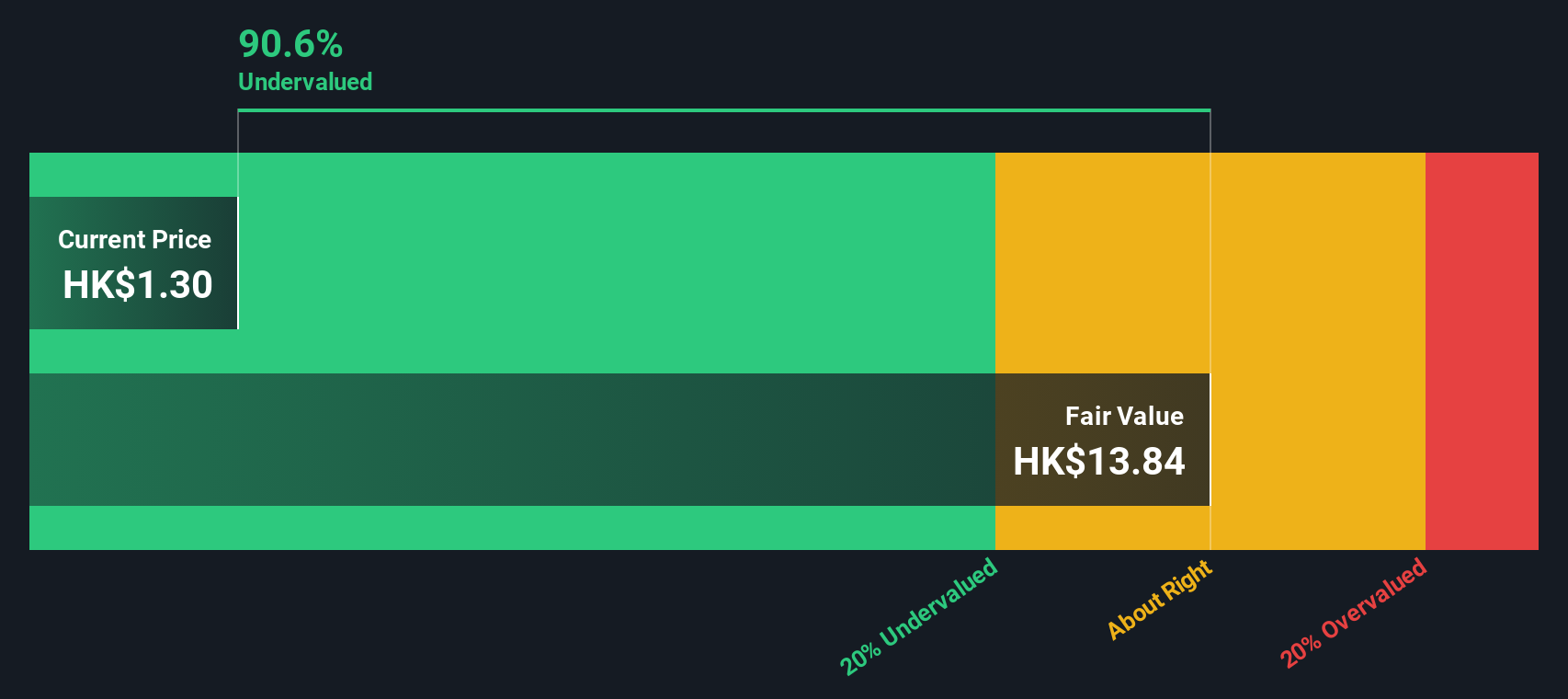

Result: Fair Value of $33.3 (UNDERVALUED)

See our latest analysis for Sunac China Holdings.However, persistent annual revenue declines and significant ongoing net losses remain risks that could counter Sunac’s recent positive momentum.

Find out about the key risks to this Sunac China Holdings narrative.Another View: Discounted Cash Flow Estimate

Switching gears from sales multiples, our SWS DCF model also points to Sunac being undervalued. Even with a different set of assumptions, this model still sees value. The question remains: can markets keep ignoring that?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Sunac China Holdings Narrative

If you see things differently or simply want to draw your own conclusions, you can quickly put together your own view on Sunac China Holdings in just a few minutes. Do it your way

A great starting point for your Sunac China Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

There are countless opportunities waiting beyond Sunac. Make smarter moves, back your research with smarter data, and get ahead of the pack with distinctive stock ideas powered by Simply Wall Street’s in-depth screener tools.

- Tap into tomorrow's growth by following healthcare AI stocks, which is powering breakthroughs in medical technology and transformative healthcare solutions.

- Spot undervalued gems trading at a discount by checking out undervalued stocks based on cash flows, identified using robust cash flow analytics and hidden value signals.

- Unlock fresh potential in emerging trends with cryptocurrency and blockchain stocks, pinpointing innovative companies making waves in digital assets and blockchain innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com