Is Santander Still Attractive After Shares Soar Nearly 100% in the Past Year?

If you are weighing your options on Banco Santander stock, you are definitely not alone. Plenty of investors are keeping an eye on this European banking giant, especially given how it has performed lately. Over just the last week, the stock crept up 1.1%, while in the past month, it gained 4.2%. Zoom out a bit, and the story gets even more compelling, with the stock rising 88.3% so far this year. Over the longer haul, the 1-year return stands at an impressive 97.1%. Those who stuck around for three or five years have seen gains of 247.0% and 445.6%, respectively.

This strong performance has not gone unnoticed, especially as global financial markets remain sensitive to ongoing changes in monetary policy and economic sentiment across Europe and Latin America. These are two regions central to Banco Santander’s business. Many investors are beginning to ask whether recent momentum is a signal of more growth to come or if it simply reflects a shift in how the market perceives risk in the banking sector.

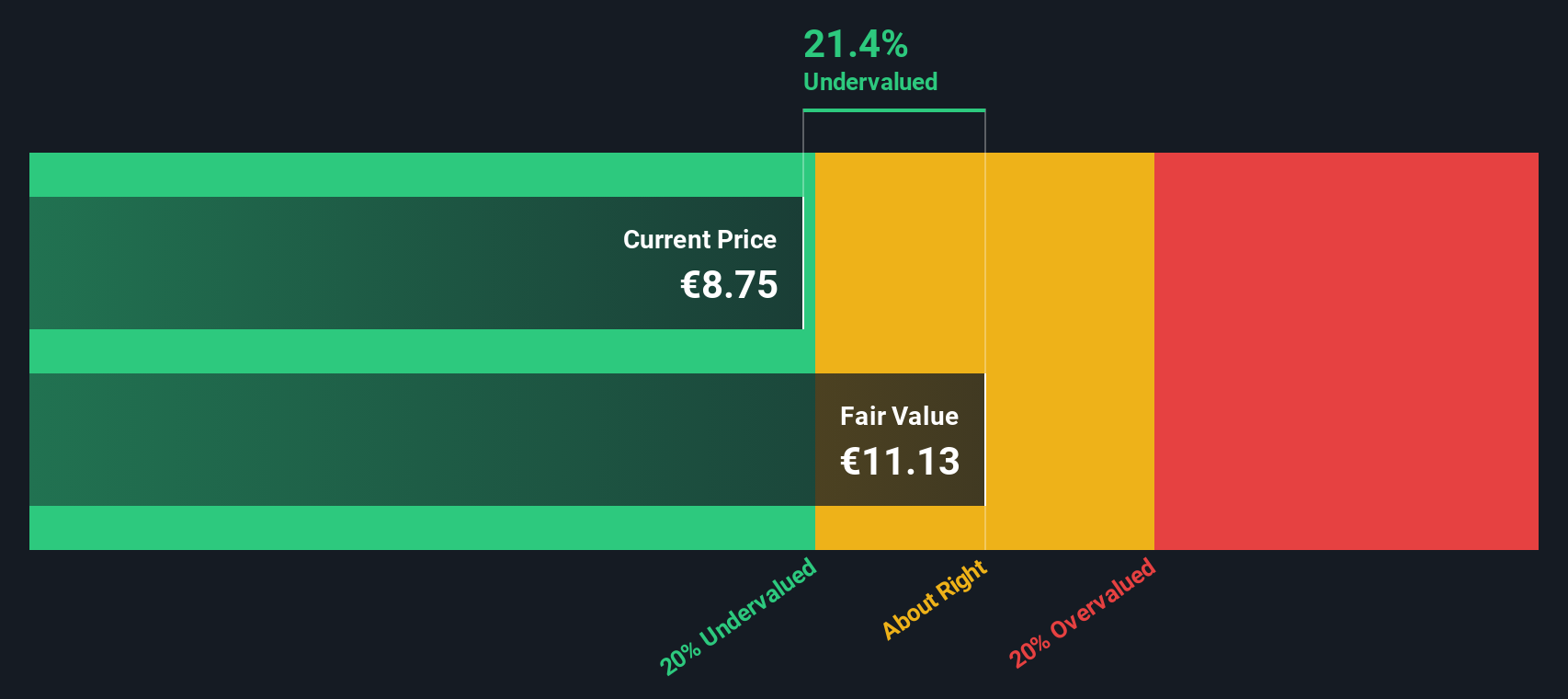

Of course, past gains are only one piece of the puzzle. For those who want to know if Banco Santander is still a smart buy right now, valuation becomes critical. By the numbers, Banco Santander scores a 4 out of 6 on our undervaluation check, passing two-thirds of the tests that point to a stock being undervalued. Next, we will break down those valuation approaches. At the end, we will dive into an even more insightful way to look at what Banco Santander may truly be worth.

Banco Santander delivered 97.1% returns over the last year. See how this stacks up to the rest of the Banks industry.Approach 1: Banco Santander Excess Returns Analysis

The Excess Returns model evaluates a company by looking at how much profit it generates above the cost of equity capital. In other words, it measures how efficiently Banco Santander turns each euro of shareholder investment into returns that surpass what investors could expect elsewhere.

For Banco Santander, the model shows a Book Value of €6.63 per share and a Stable EPS of €1.00 per share, sourced from a consensus of 13 analyst estimates. The company's Cost of Equity is calculated at €0.75 per share, meaning every euro invested by shareholders is expected to return €1.00, outpacing basic equity costs. This delivers an Excess Return of €0.25 per share, with an average Return on Equity at a solid 12.74%. Looking ahead, the Stable Book Value is estimated to rise to €7.84 per share, according to projections from nine analysts.

Based on these numbers, the Excess Returns model suggests Banco Santander is intrinsically valued at a level reflecting a 26% discount to its current market price. This means the stock is currently considered undervalued through this lens.

Result: UNDERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Banco Santander.

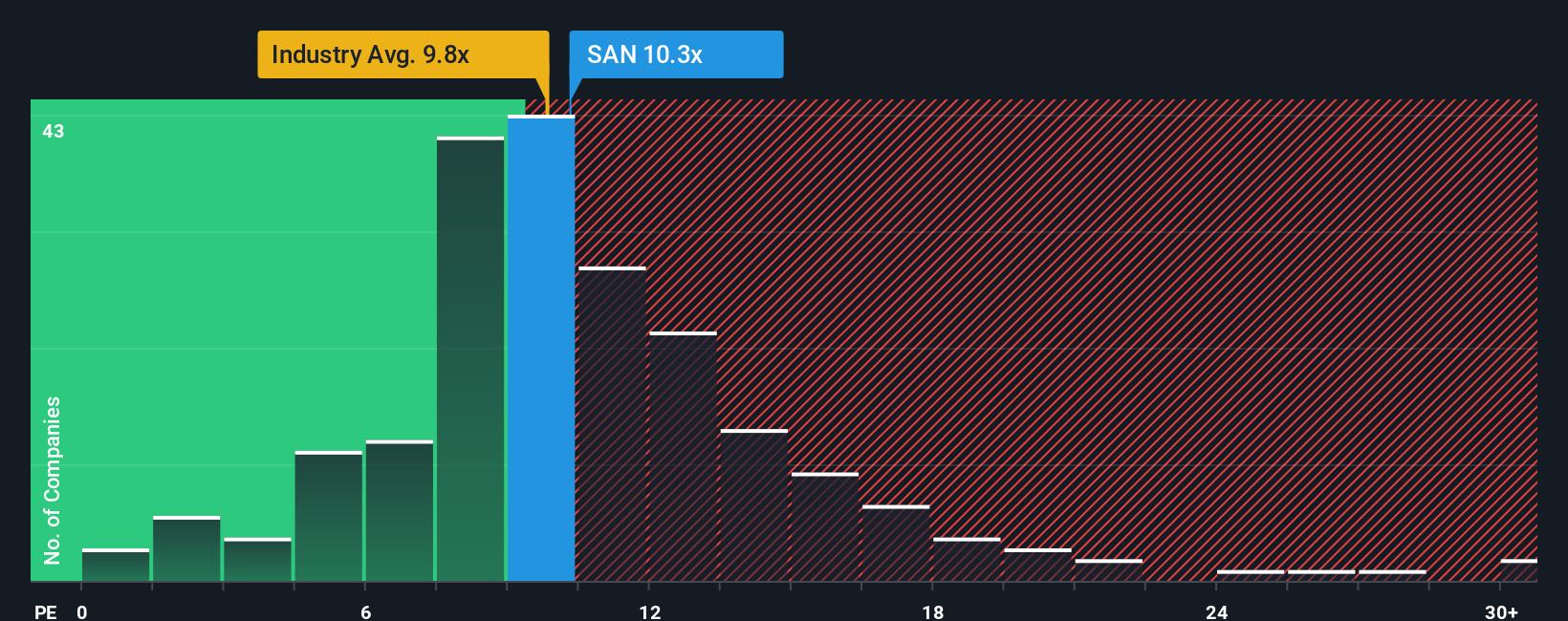

Approach 2: Banco Santander Price vs Earnings (P/E)

The Price-to-Earnings (P/E) ratio is often used for valuing consistently profitable companies like Banco Santander, because it connects a company's share price to the earnings it produces for shareholders. This multiple helps investors quickly gauge whether a stock might be cheap or expensive relative to its current profits.

When considering whether a P/E ratio is reasonable, it is important to factor in how fast a company is expected to grow and what risks it faces. Generally, higher growth potential or lower risks justify a higher "normal" P/E. In contrast, slower growth or higher risk should result in a lower P/E.

Banco Santander currently trades on a P/E ratio of 9.78x, which is slightly below the industry average of 10.39x and just under its peer average of 9.90x. This suggests the market is pricing the stock conservatively compared to typical banks in the region. Notably, Simply Wall St’s Fair Ratio for Banco Santander is 10.99x. This is a proprietary calculation that takes into account the company’s unique growth outlook, risk profile, profit margins, industry, and market capitalization. Unlike a simple comparison with peers or the broader industry, this Fair Ratio provides additional context and a tailored benchmark for what the P/E should be given all relevant factors.

With Banco Santander’s current P/E very close to its Fair Ratio, the stock appears to be trading about where it should be based on its fundamentals and outlook.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your Banco Santander Narrative

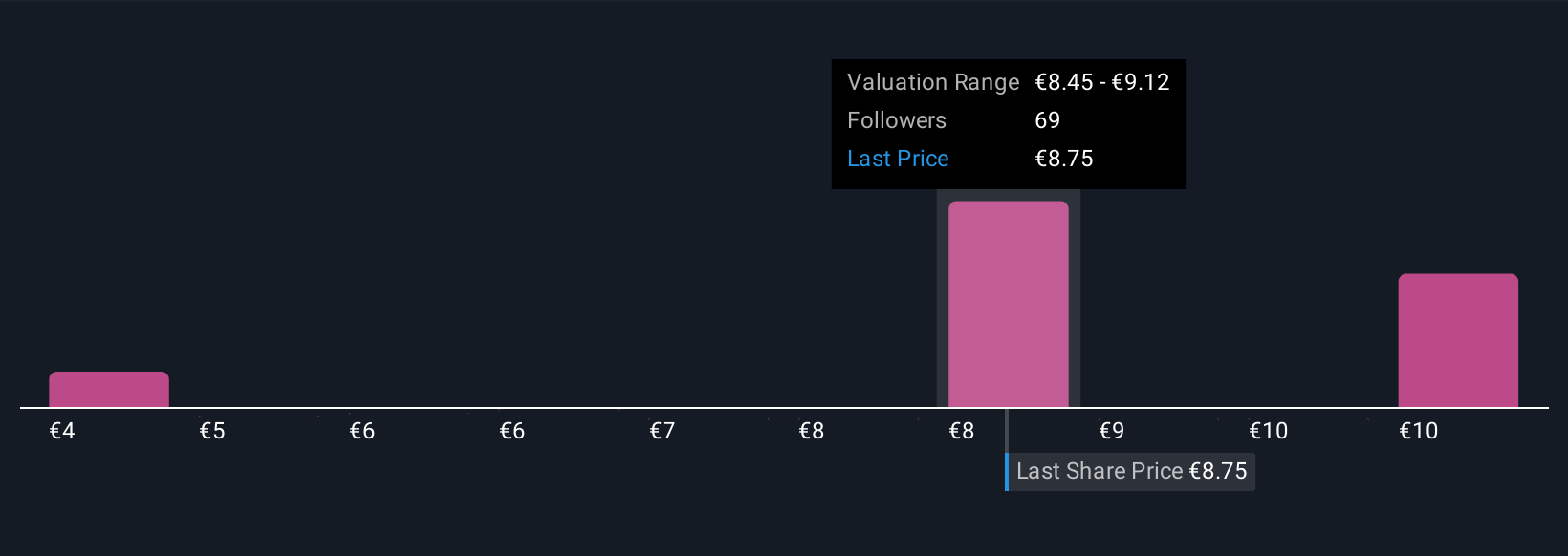

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. On Simply Wall St, a Narrative is a simple, dynamic way to express your view of a company by connecting its story to a financial forecast. This then leads to a personal estimate of fair value.

Rather than just focusing on traditional metrics, Narratives empower you to combine your perspective on Banco Santander’s strategy, risks, and growth drivers with your assumptions for future revenues, earnings, and profit margins. This approach helps frame a company’s numbers within the bigger picture of where you think the business is heading, making your valuation more meaningful and relevant to your outlook.

The Narratives feature, available on the Community page and used by millions of investors, lets you easily set or update your forecast and see your Fair Value compared directly to the current market price. This helps to clarify when to buy or sell based on your own reasoning, not just analyst estimates or market sentiment.

Best of all, Narratives are updated automatically as new data and news arrives, so your analysis is always current. For example, one investor might believe Santander deserves a much lower fair value of €4.43 due to digital banking execution challenges, while another sees €7.99 as fair, based on digital growth and Latin American expansion. This highlights how Narratives reflect differing, data-backed opinions.

Do you think there's more to the story for Banco Santander? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com