A Fresh Look at Marvell Technology (MRVL) Valuation Following AI Growth, New Products, and Return to Profitability

If you have been watching Marvell Technology (MRVL), the company’s latest quarterly results might just change how you see its future. Marvell posted impressive year-over-year revenue growth and swung back to profitability, largely on the strength of rising demand in its data center business and newer AI-focused custom silicon products. In addition to these financials, Marvell has been rolling out new technology, from memory expansion controllers to state-of-the-art die-to-die interconnects, that underline its position at the forefront of data-centric infrastructure. News of ongoing buybacks, supported by proceeds from key business divestitures, helps tell a story of a company actively shaping its future and returning capital to shareholders.

All of this comes at a time when Marvell’s share price performance has been a bit of a roller coaster. Despite the recent bounce in demand and technological innovation, MRVL shares are down almost 4% over the past year and sit lower still from highs at the start of 2025. Momentum has cooled compared to the last few years, even with new product wins and high-profile partnerships with major cloud providers. The recent rebound in profitability and expansion into new data center markets may signal a turn, but investors have seen both volatility and lingering skepticism reflected in the stock’s price.

With Marvell’s story evolving and shares lagging broader tech moves, the question for investors is whether this presents a window for long-term growth or if the market has already accounted for what comes next.

Most Popular Narrative: 23.3% Undervalued

The prevailing narrative suggests Marvell Technology is notably undervalued, with analysts projecting significant upside based on future earnings growth, margin expansion, and market share gains.

“The company's success in securing multigenerational design wins with hyperscalers and ramping up a robust pipeline (over 50 new custom silicon opportunities representing $75 billion in lifetime value) positions Marvell to grow its data center market share from 13% to 20% of a fast-expanding $94B TAM by 2028. This is expected to drive recurring and expanding revenue.”

Want to know what’s fueling this bold target? The secret lies in a set of rapid-fire growth forecasts and profit milestones that shape Marvell’s valuation in a way not seen before. Curious which financial leaps are assumed in this calculation? There is much more happening behind the headline than meets the eye.

Result: Fair Value of $86.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, heavy reliance on major data center customers and unpredictable custom project cycles may challenge Marvell’s future growth trajectory if market trends shift.

Find out about the key risks to this Marvell Technology narrative.Another View: Valued Against Industry Standards

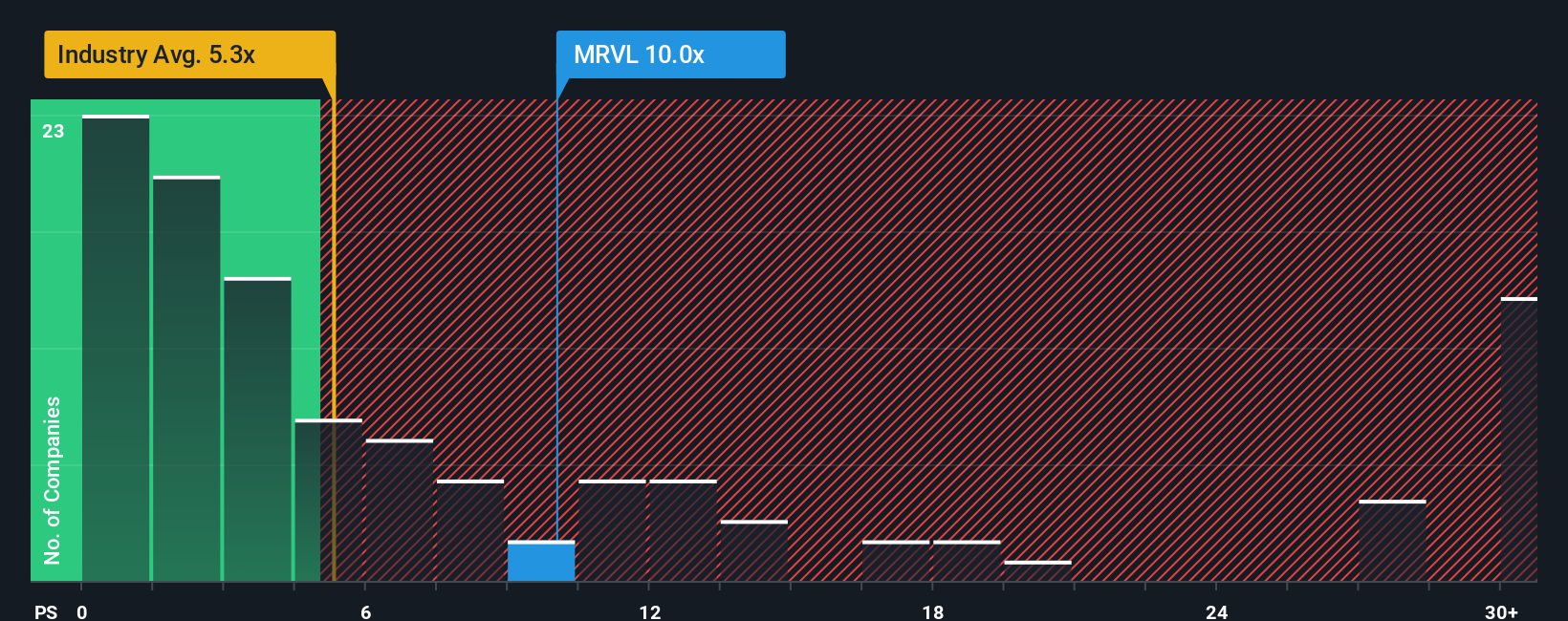

Looking at Marvell next to others in its industry, shares actually appear quite expensive compared to the typical price-to-sales metric seen among U.S. semiconductor companies. Does this indicate higher expectations or simply more risk?

See what the numbers say about this price — find out in our valuation breakdown.While multiples offer one perspective, different approaches can tell a different story. The valuation picture for Marvell may depend on which lens you use.

Build Your Own Marvell Technology Narrative

If you see things differently or want to dig deeper into the numbers yourself, you can craft your own Marvell story in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Marvell Technology.

Looking for More Ways to Invest with Confidence?

Stock markets never stop moving, and opportunity is everywhere. Take your investing up a notch by tapping into fresh stock ideas and hidden gems with tools built for smart investors.

- Unlock income potential from stable companies and access reliable cash flows by checking out dividend stocks with yields > 3%.

- Jump ahead of the crowd with innovators at the intersection of healthcare and intelligence by using healthcare AI stocks.

- Catch tomorrow’s breakthroughs early and amplify your portfolio’s upside by uncovering the next wave of quantum computing stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com