Is Grenergy Renovables (BME:GRE) Overvalued After Its Strong Share Price Rally?

Grenergy Renovables (BME:GRE) has been catching some attention lately, even without a specific news event setting things in motion. Sometimes, a stock makes a move that sparks fresh debate among investors who are wondering whether the gains signal real momentum or simply market noise. It is this kind of shift, without a clear external trigger, that often pushes valuation into the spotlight and has market watchers double-checking whether an opportunity is taking shape right under their noses.

Despite a lack of headline-grabbing news, Grenergy Renovables’ shares have gained a strong 15% over the past month and are up more than 100% for the year. Shorter-term momentum has picked up substantially, although the three-year and five-year returns show even more dramatic growth. Underneath these numbers, the company’s annual revenue and net income have also kept advancing, adding another layer for those weighing its valuation story.

The real question now, after this year’s extraordinary run, is whether Grenergy Renovables is in bargain territory, or if the market has already baked in its future growth prospects?

Price-to-Earnings of 23.6x: Is it justified?

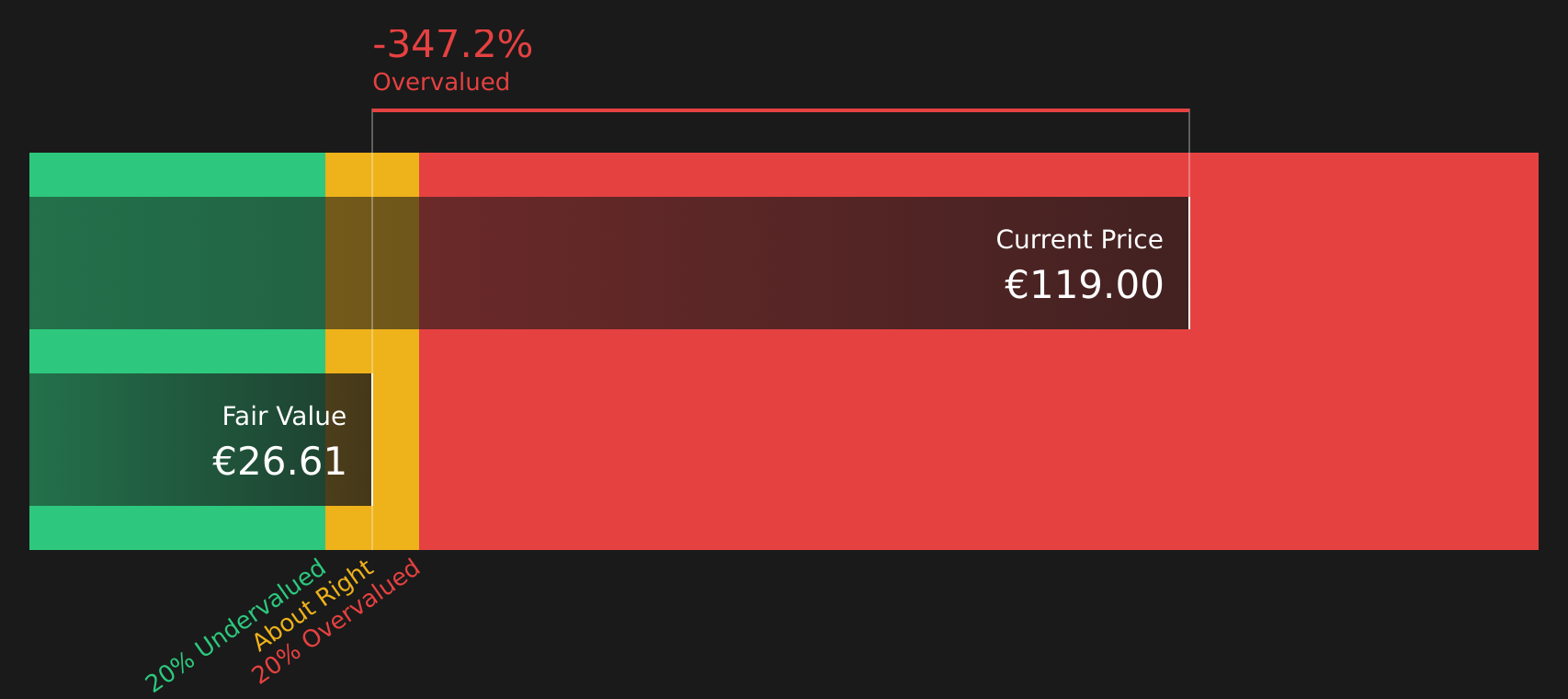

Based on the price-to-earnings (P/E) ratio, Grenergy Renovables appears overvalued compared to both its industry peers and the broader European renewable energy sector. The company trades at a P/E of 23.6x, which is notably higher than the European industry average of 15.9x.

The P/E ratio measures a company's current share price relative to its earnings per share. For renewable energy firms, this multiple is particularly important because it helps investors gauge whether optimism about future growth is causing the stock to trade at a premium to recent earnings power.

Although Grenergy's historical and forecasted earnings growth is robust, the current P/E suggests the market is pricing in extremely strong ongoing performance. Investors should weigh whether this premium is supported by future growth prospects or if the stock is now running ahead of fundamentals.

Result: Fair Value of €71.1 (OVERVALUED)

See our latest analysis for Grenergy Renovables.However, a slowdown in revenue growth or changing sentiment around renewables could quickly challenge the current valuation narrative for Grenergy Renovables.

Find out about the key risks to this Grenergy Renovables narrative.Another View: Our DCF Model Says Overvalued Too

Taking a step back from earnings multiples, our SWS DCF model also indicates that Grenergy Renovables is trading well above its fair value. Could both methods be missing something? Or is this a clear warning sign?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Grenergy Renovables Narrative

If you feel that this view does not align with your own analysis or you enjoy diving into the data independently, you can quickly develop your own narrative in just a few minutes. Do it your way

A great starting point for your Grenergy Renovables research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t miss your chance to spot tomorrow’s opportunities. Expand your portfolio horizon now with fresh stock ideas tailored to your strategy on Simply Wall Street.

- Boost your portfolio’s earning potential by uncovering reliable companies packed with dividend stocks with yields > 3% for consistent income streams.

- Tap into futuristic breakthroughs by screening quantum computing stocks and stay ahead in the race for technological edge.

- Seize hidden gems the market has overlooked by filtering for undervalued stocks based on cash flows and get a head start on tomorrow’s value plays.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com