Erste Group Bank (WBAG:EBS): A Fresh Valuation Check as Momentum Slows

Most Popular Narrative: Fairly Valued

According to the most widely followed narrative, Erste Group Bank's shares are now trading at a price that closely matches the consensus fair value. The narrative suggests there is no significant discount or premium at current levels.

The analysts have a consensus price target of €81.567 for Erste Group Bank based on their expectations of its future earnings growth, profit margins, and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €97.0, and the most bearish reporting a price target of just €62.0.

Curious about the financial story behind this narrow margin between current price and target? The answer lies in the projections about revenue, earnings, and how much profit growth will be valued in a future market that may differ significantly from today. How is this fair value justified? Unlock the numbers and the full analyst view on Erste's unique position and its competitive assumptions.

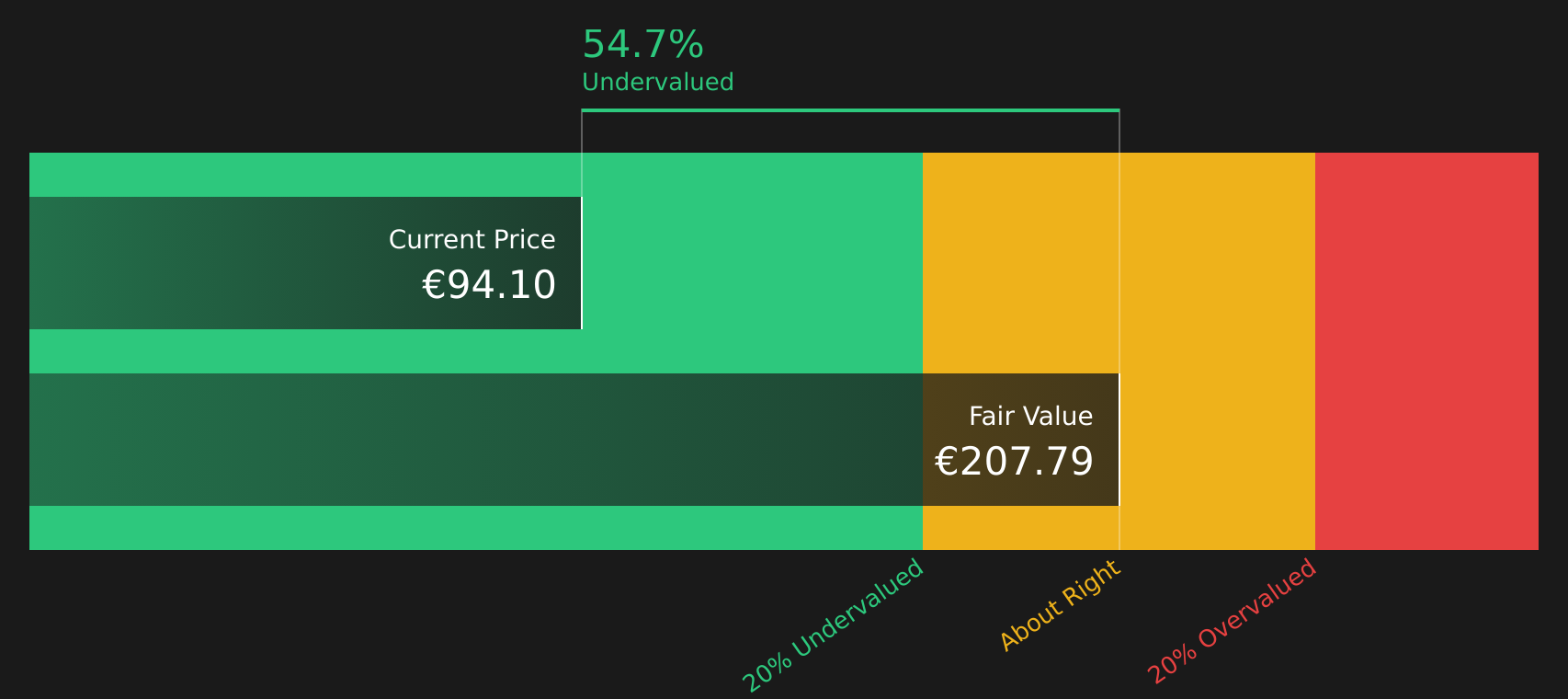

Result: Fair Value of €81.57 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent windfall taxes in key markets or integration challenges from the rapid Polish expansion could quickly change the outlook for Erste Group Bank.

Find out about the key risks to this Erste Group Bank narrative.Another View: Discounted Cash Flow Model

While analyst consensus points to a fair price, our DCF model takes a deeper look at Erste Group Bank’s long-term cash flows and reveals the potential for undervaluation. Do these two perspectives tell the same story, or is there a hidden opportunity?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Erste Group Bank Narrative

If these perspectives do not quite reflect your own, or you prefer to dig deeper and reach your own conclusions, you can easily assemble your own narrative in just a few minutes. Do it your way.

A great starting point for your Erste Group Bank research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t miss out; your next market win could be closer than you think. Use the Simply Wall Street Screener to quickly uncover investment opportunities others might overlook.

- Spot tomorrow’s standout small-caps rocking strong balance sheets with our list of penny stocks with strong financials.

- Tap into the future of medicine by checking out innovators using artificial intelligence in healthcare, all in our exclusive healthcare AI stocks roundup.

- Boost your portfolio’s income with companies offering yields above 3%. See the latest selections in our dividend stocks with yields > 3% guide.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com