Is Dai Nippon Printing (TSE:7912) Undervalued? Taking a Fresh Look at Recent Valuation Signals

Price-to-Earnings of 12.3x: Is it justified?

Dai Nippon Printing is currently trading at a price-to-earnings (P/E) ratio of 12.3, positioning it well below both its peer average (18.6) and the broader industry average (13.3). This suggests that, on an earnings basis, the market views the stock as undervalued relative to comparable companies in Japan's Commercial Services sector.

The price-to-earnings ratio is a fundamental measure used to gauge how much investors are willing to pay for each yen of earnings. For a company like Dai Nippon Printing, which has a long operating history and generates steady profits, a lower P/E can signal either skepticism about its growth prospects or a potential buying opportunity if fundamentals remain solid.

Given that the P/E ratio is significantly below both peer and industry averages, the data suggests that the company is trading at a discount. This could indicate that the market is underpricing Dai Nippon Printing's ability to generate future earnings, especially when compared to other companies in its sector.

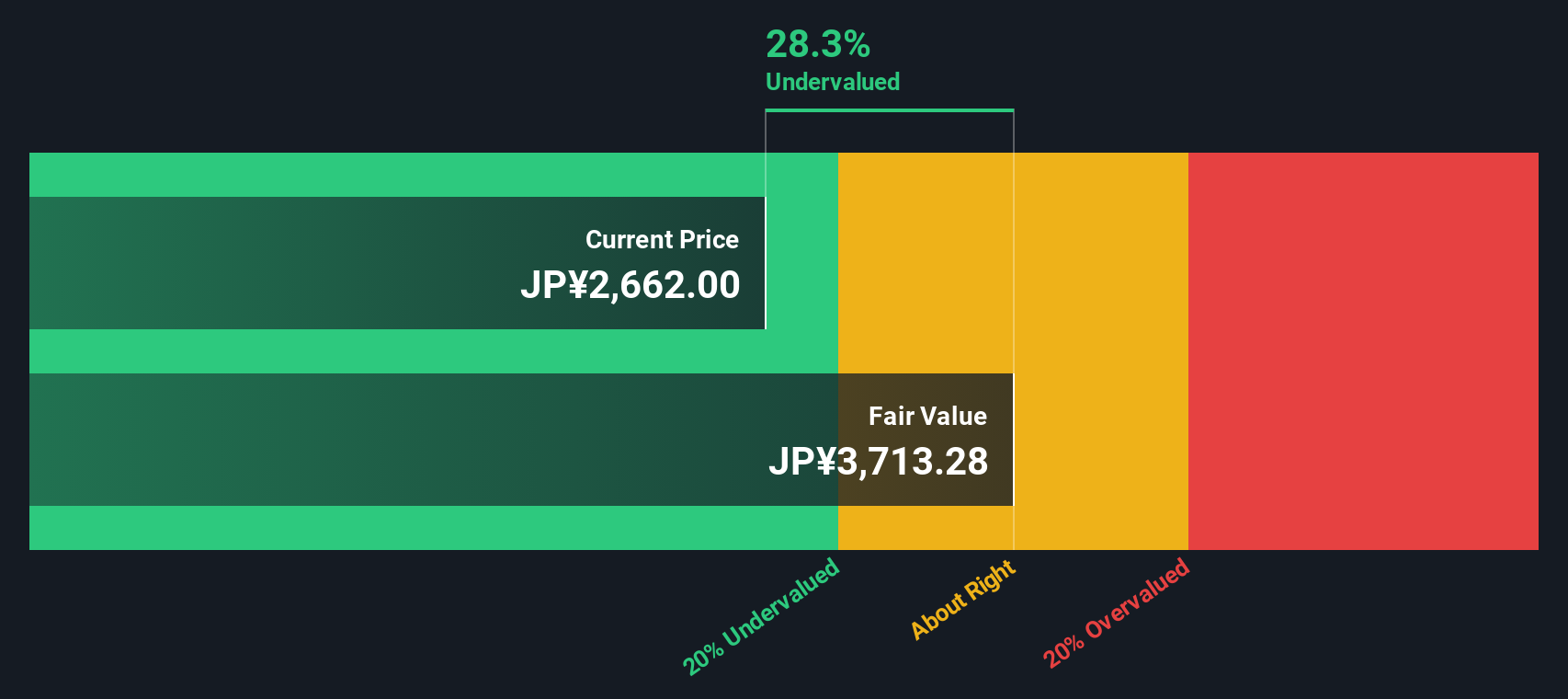

Result: Fair Value of ¥3,619.35 (UNDERVALUED)

See our latest analysis for Dai Nippon Printing.However, ongoing pressure on net income growth and modest revenue growth could challenge the undervalued thesis if these trends persist in coming quarters.

Find out about the key risks to this Dai Nippon Printing narrative.Another View: What Does the DCF Say?

Taking things a step further, our DCF model offers a different perspective on Dai Nippon Printing’s valuation. Interestingly, it also points toward the shares being undervalued at current prices. Could both methods be missing something? Does this consensus signal a rare opportunity?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Dai Nippon Printing Narrative

If you have a different perspective or prefer to dig into the numbers yourself, you can shape your own take in just a few minutes with our tools: Do it your way.

A great starting point for your Dai Nippon Printing research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Opportunities?

Missing out on other promising ideas could mean leaving gains on the table. Use these curated shortcuts to spot your next potential winner before the market catches on.

- Accelerate your strategy with low-priced stocks showing robust financial health by jumping straight to penny stocks with strong financials.

- Fuel your portfolio with high-yield options by tracking companies offering dividend stocks with yields > 3% to lock in superior income streams.

- Stay ahead of the curve in digital finance by finding movers in cryptocurrency and blockchain stocks, where innovation is reshaping the future of investing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com