Will Leadership Changes Steer MillerKnoll (MLKN) Toward Greater Innovation and Sustainability?

- MillerKnoll announced the appointment of Jeff Stutz as Chief Operating Officer and John Hoke as incoming Board Chair following the retirement of Mike Volkema, bringing experienced leadership from within and outside the company to key oversight and operational roles.

- John Hoke's design and innovation expertise from his long tenure at Nike signals a potential greater focus on sustainability and creative growth initiatives within MillerKnoll's leadership team.

- We'll explore how the addition of John Hoke as Board Chair could influence MillerKnoll's focus on innovation and future strategic direction.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

MillerKnoll Investment Narrative Recap

To believe in MillerKnoll as a shareholder, one must have confidence in the company's ability to drive innovation and operational efficiency amid macroeconomic pressure and sector-wide trade policy risks. While the recent board and executive appointments bring strong experience to the table, the most important short-term catalyst, turnaround in key business segments, remains only modestly affected by leadership changes at this stage. The biggest ongoing risk continues to stem from deteriorating retail margins and persistent asset impairments, with the latest news making limited direct impact on this immediate concern.

The appointment of John Hoke as Board Chair stands out among recent announcements by strengthening the company’s future focus on design innovation and potentially renewed creative direction. While this aligns with MillerKnoll’s longer-term growth ambitions, the near-term business catalysts such as segment restructuring and global expansion remain driven primarily by broader market developments and existing operational efforts.

However, investors should not overlook the potential for further asset impairments and special charges if profitability challenges in the retail segment persist...

Read the full narrative on MillerKnoll (it's free!)

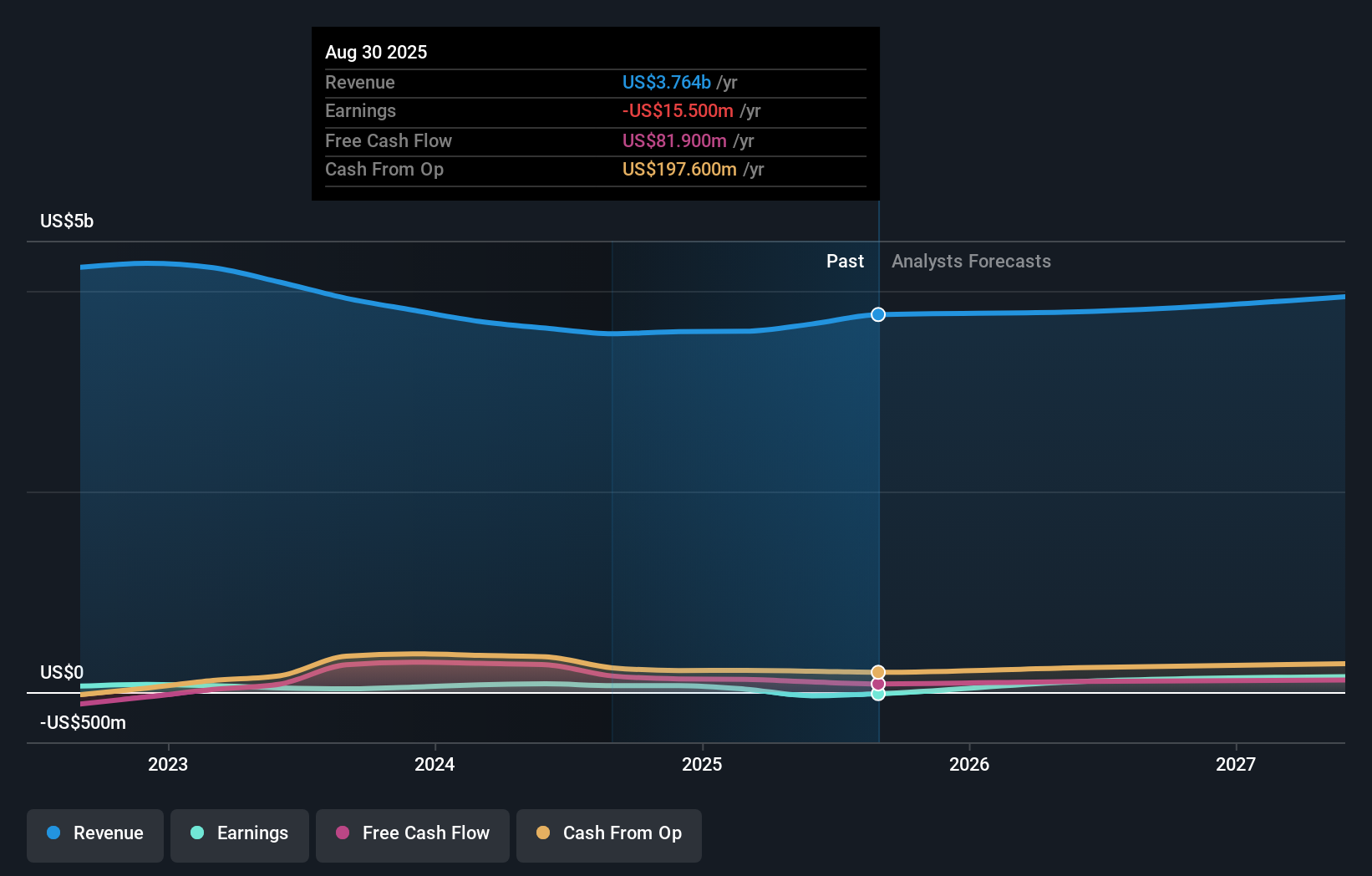

MillerKnoll's outlook anticipates $4.0 billion in revenue and $293.0 million in earnings by 2028. This scenario is based on annual revenue growth of 3.2% and an earnings increase of $329.9 million from current earnings of -$36.9 million.

Uncover how MillerKnoll's forecasts yield a $38.00 fair value, a 81% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community produced a single fair value estimate of US$38.00, showing no range among their views. Despite this, ongoing profit challenges and retail margin pressures highlight why market participants may hold diverse opinions about the company’s outlook, reviewing more perspectives may reveal alternatives you have not considered.

Explore another fair value estimate on MillerKnoll - why the stock might be worth just $38.00!

Build Your Own MillerKnoll Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your MillerKnoll research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MillerKnoll research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MillerKnoll's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com