Assessing Catena’s (OM:CATE) Valuation as Recent Share Price Weakness Draws Investor Attention

There’s no headline-grabbing news out of Catena (OM:CATE) this week. That in itself might catch the attention of investors wondering whether the stock’s recent slide signals something deeper or simply reflects shifting sentiment. Without a major trigger to explain the movement, some shareholders may find themselves asking whether this is an early warning or an overlooked opportunity to dig into the numbers and revisit the company’s long-term value proposition.

Catena’s share price has certainly had a tough run this year, extending a streak of declines both in the short and longer term. The stock is down roughly 22% over the past year and has lost ground in the last month as well as over the past quarter, reversing a strong return over five years. Revenue and earnings growth have been muted recently, and momentum seems to be fading for now, making valuation a more pressing question.

Does the current weakness represent a discounted entry point into Catena, or is the market simply pricing in muted growth ahead?

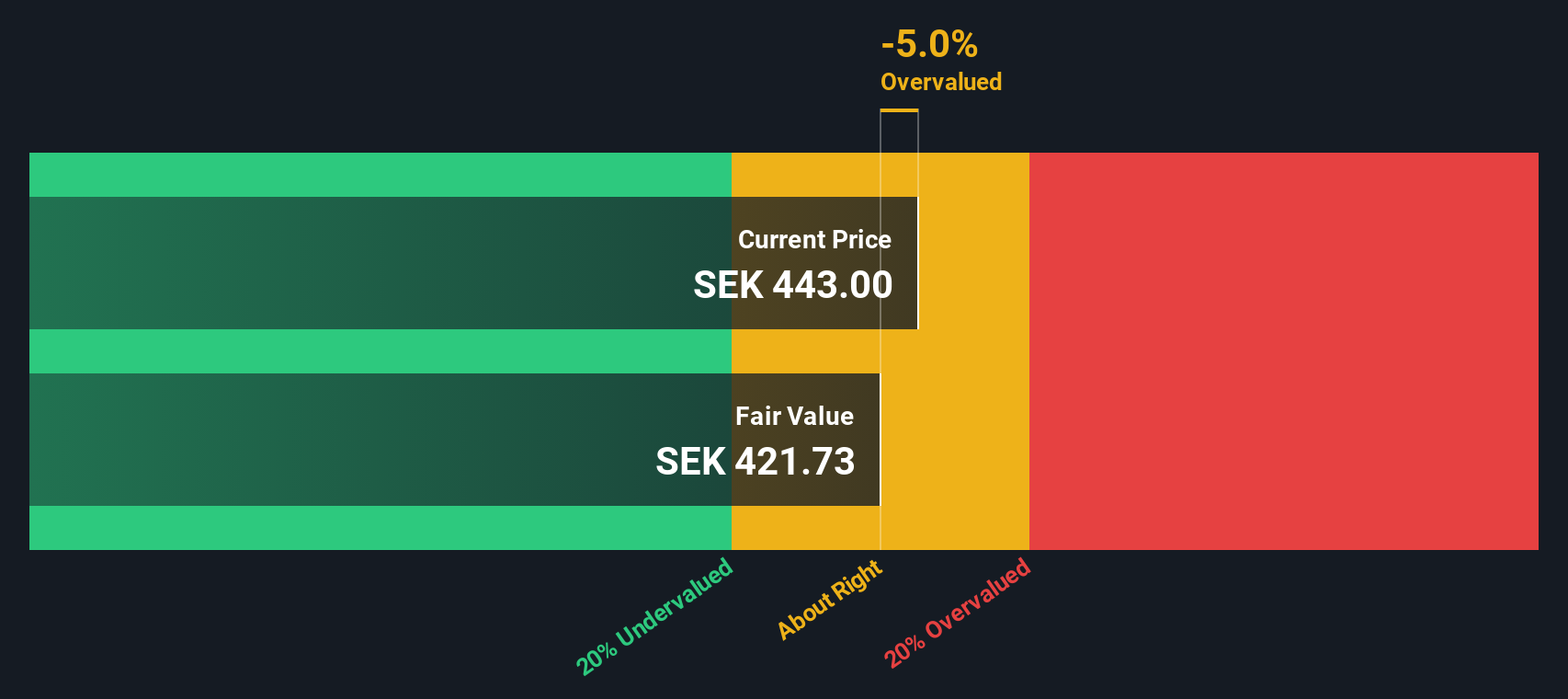

Most Popular Narrative: 85% Overvalued

According to Unike, the prevailing view is that Catena currently trades at a substantial premium to its estimated fair value, based on the narrative's discounted cash flow approach and fundamental forecasting.

Catena is expected to remain a leading logistics real estate player, benefiting from e-commerce growth, urbanization, and supply chain changes. If well executed, portfolio expansion and higher-quality assets should enhance profitability.

Think Catena’s premium is all about market hype? There is a detailed model behind this verdict, hinging on revenue expansion, bold margin stability, and a multiple that might surprise you. Want to discover what assumptions Unike made to justify this aggressive fair value and just how long-term growth drivers are factored in? Dig in and see the full picture to understand what is powering this striking valuation gap.

Result: Fair Value of $229.2 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, a prolonged period of high interest rates or an economic slowdown could quickly challenge the optimistic outlook that currently underpins Catena’s valuation.

Find out about the key risks to this Catena narrative.Another View: What Does Our DCF Model Say?

Looking at Catena through the lens of our DCF model offers a different perspective. This approach suggests the shares are priced above their estimated intrinsic value, which raises another set of questions about long-term growth versus market optimism. Which view gets it right?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Catena Narrative

If you see things differently or want to dive deeper into the numbers yourself, it’s quick and easy to craft your own perspective. Do it your way.

A great starting point for your Catena research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Great Investment Ideas?

Smart investors constantly expand their horizons. Make sure you’re not missing tomorrow’s winners by searching for companies with high growth potential, reliable income, and disruptive influence using these powerful tools:

- Capture reliable income streams and boost your yield by checking out companies offering impressive payouts through dividend stocks with yields > 3%.

- Tap into the next wave of tech innovation by hunting for bold pioneers shaping the future of medicine with healthcare AI stocks.

- Seize overlooked bargains and find stocks trading below their true value using our essential guide to undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com